You might also like

- Notes To Financial Statements TemplateDocument2 pagesNotes To Financial Statements TemplateFlorendo Dauz Jr.100% (1)

- BookkeepingRegulationsRRV 1Document80 pagesBookkeepingRegulationsRRV 1Jeremy Kuizon Pacuan100% (1)

- Quality Assurance Process Manual FOR Sole Proprietor CpaDocument21 pagesQuality Assurance Process Manual FOR Sole Proprietor CpaAnasor GoNo ratings yet

- Letter Response - Request For ELOA Revalidation V2Document2 pagesLetter Response - Request For ELOA Revalidation V2Jazz TraceyNo ratings yet

- BIR Releases Rules On Appealing Disputed Tax AssessmentsDocument13 pagesBIR Releases Rules On Appealing Disputed Tax AssessmentsDana100% (1)

- Raymart - Notes To FS 2018Document7 pagesRaymart - Notes To FS 2018gerald padua100% (3)

- Special Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument47 pagesSpecial Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityLady Paul SyNo ratings yet

- 39621RMC 30-2008Document11 pages39621RMC 30-2008remingiiiNo ratings yet

- RGM3 - Assessment 11.26.2018Document73 pagesRGM3 - Assessment 11.26.2018Rufino Gerard Moreno IIINo ratings yet

- RMC 30-2008.PDF - Life and Non-Life InsuranceDocument5 pagesRMC 30-2008.PDF - Life and Non-Life InsuranceAbaNo ratings yet

- Bookkeeping RegulationsDocument23 pagesBookkeeping RegulationsJewellrie Dela Cruz100% (2)

- Notes To Financial StatementsDocument9 pagesNotes To Financial StatementsCheryl FuentesNo ratings yet

- Train LawDocument108 pagesTrain LawKenneth Cyrus Olivar100% (1)

- Managing Birs Tax Assessment FreeebookDocument88 pagesManaging Birs Tax Assessment FreeebookJohn Patrick Guillen100% (1)

- TRAIN Law - Diaz Murillo Dalupan and CompanyDocument215 pagesTRAIN Law - Diaz Murillo Dalupan and CompanyBien Bowie A. Cortez100% (1)

- XXXXXXXXXXXXXXX, Inc.: Notes To Financial Statements DECEMBER 31, 2018 1.) Corporate InformationDocument7 pagesXXXXXXXXXXXXXXX, Inc.: Notes To Financial Statements DECEMBER 31, 2018 1.) Corporate InformationJmei AfflieriNo ratings yet

- Other MatterDocument4 pagesOther MatterBrex Lloyd MalaluanNo ratings yet

- RMC 72-04Document9 pagesRMC 72-04ai0412No ratings yet

- Bir Ruling 044-10Document4 pagesBir Ruling 044-10Jason CertezaNo ratings yet

- Statement of MGT Responsibility ITRDocument1 pageStatement of MGT Responsibility ITRJasper Andrew AdjaraniNo ratings yet

- Rmo 19-2007Document14 pagesRmo 19-2007Em CaparrosNo ratings yet

- Mastering BIR Year-End Compliance Requirements.: AIT Webinar, January 22, 2022 By: Dante R. TorresDocument66 pagesMastering BIR Year-End Compliance Requirements.: AIT Webinar, January 22, 2022 By: Dante R. TorresClarine Kyla Bautista100% (1)

- SRC Rule 68 As AmendedDocument51 pagesSRC Rule 68 As AmendedGilYah MoralesNo ratings yet

- TAX PAYER GUIDE MannualDocument7 pagesTAX PAYER GUIDE MannualLevi Lazareno EugenioNo ratings yet

- Illustrative FS - PFRS For Small EntitiesDocument28 pagesIllustrative FS - PFRS For Small EntitiesJessa EspinozaNo ratings yet

- VAT LetterDocument2 pagesVAT Letterrhea CabillanNo ratings yet

- Full PFRS Illustrative Financial Statements 2018Document126 pagesFull PFRS Illustrative Financial Statements 2018Jake Aseo BertulfoNo ratings yet

- Tax Filing Reminders: OutlineDocument30 pagesTax Filing Reminders: OutlineMarc Nathaniel RanayNo ratings yet

- Offer LetterDocument3 pagesOffer LetterpartionNo ratings yet

- Issues, Problems and Solutions in Tax Audit and Investigation (1-10-13)Document184 pagesIssues, Problems and Solutions in Tax Audit and Investigation (1-10-13)marygrace_apaitan100% (2)

- RMC 35-2006 Taxation For Freight ForwardersDocument23 pagesRMC 35-2006 Taxation For Freight ForwardersremoveignoranceNo ratings yet

- General Audit Procedures and Documentation-BirDocument3 pagesGeneral Audit Procedures and Documentation-BirAnalyn BanzuelaNo ratings yet

- Group 6Document27 pagesGroup 6Joyce Kay AzucenaNo ratings yet

- Revised Statement of Management Responsibility 2017Document1 pageRevised Statement of Management Responsibility 2017MackyNo ratings yet

- Certification Statement of Management's Responsibility (Itr)Document1 pageCertification Statement of Management's Responsibility (Itr)Earl Jhune Amoranto100% (1)

- RR 2-98 - Withholding TaxesDocument99 pagesRR 2-98 - Withholding TaxesbiklatNo ratings yet

- Ms. Luisa M. LabadDocument14 pagesMs. Luisa M. LabadLaarnie ManalastasNo ratings yet

- Mary Joy L. Amigos Rice Store Notes To The Financial StatementsDocument5 pagesMary Joy L. Amigos Rice Store Notes To The Financial StatementsLizanne GauranaNo ratings yet

- How To Use BIR FormsDocument52 pagesHow To Use BIR Formsbalinghoy#hotmail_com2147No ratings yet

- Annex C-1 - Summary of System DescriptionDocument4 pagesAnnex C-1 - Summary of System DescriptionChristian Albert HerreraNo ratings yet

- Notes To FS EncodingDocument11 pagesNotes To FS EncodingPappi JANo ratings yet

- RMC 72-2004 PDFDocument9 pagesRMC 72-2004 PDFBobby LockNo ratings yet

- Accounting ManualDocument2 pagesAccounting ManualAshok Raaj100% (1)

- 1701 GuidelinesDocument4 pages1701 GuidelinesJazz techNo ratings yet

- TaxDocument6 pagesTaxChristian GonzalesNo ratings yet

- Secrets To Prevent BIR Audit and Eliminate Tax Assessments - R1 - v2Document50 pagesSecrets To Prevent BIR Audit and Eliminate Tax Assessments - R1 - v2Peter John M. Lainez100% (2)

- CAR 2D Expanded Engagement Ltr-Compilation (5-17)Document8 pagesCAR 2D Expanded Engagement Ltr-Compilation (5-17)Andy RossNo ratings yet

- Pbcom V CirDocument9 pagesPbcom V CirAbby ParwaniNo ratings yet

- Pagong BagalDocument1 pagePagong Bagaljuliet_emelinotmaestroNo ratings yet

- Sample Audit Engagement Letter June 2015 PDFDocument9 pagesSample Audit Engagement Letter June 2015 PDFfasdsadsaNo ratings yet

- Refund of CWT and VAT Upon Dissolution of Company - ICN 9.11.14Document3 pagesRefund of CWT and VAT Upon Dissolution of Company - ICN 9.11.14JianSadakoNo ratings yet

- Process For Application To Use LooseleafDocument1 pageProcess For Application To Use LooseleafFrancis MartinNo ratings yet

- Preparation of Financial Statements 081112 RevisedDocument89 pagesPreparation of Financial Statements 081112 RevisedNorhian AlmeronNo ratings yet

- QB 2015 CH 4 LectureDocument99 pagesQB 2015 CH 4 LectureFadi Alshiyab100% (1)

- What Is Separation PayDocument2 pagesWhat Is Separation PayMartin SandersonNo ratings yet

- Statement of ManagementDocument31 pagesStatement of ManagementSharmz SalazarNo ratings yet

- The Philippine Accountancy Act of 2004Document74 pagesThe Philippine Accountancy Act of 2004YamateNo ratings yet

- RR 12-2007Document6 pagesRR 12-2007Irish BalabaNo ratings yet

- RR No. 12-2007 PDFDocument7 pagesRR No. 12-2007 PDFAbbey LiNo ratings yet

- REVENUE REGULATIONS NO. 12-2007 Issued On October 17, 2007 Amends CertainDocument2 pagesREVENUE REGULATIONS NO. 12-2007 Issued On October 17, 2007 Amends CertainJolinaBanawaNo ratings yet

- Crisostomo Vs NazarenoDocument4 pagesCrisostomo Vs NazarenonaldsdomingoNo ratings yet

- Caladiao V de BlasDocument3 pagesCaladiao V de BlasnaldsdomingoNo ratings yet

- J. Tiosejo Investment Corp. Vs AngDocument15 pagesJ. Tiosejo Investment Corp. Vs AngnaldsdomingoNo ratings yet

- Araullo V AquinoDocument14 pagesAraullo V AquinonaldsdomingoNo ratings yet

- Martinez V Ong Po - Full TextDocument3 pagesMartinez V Ong Po - Full TextnaldsdomingoNo ratings yet

- Domondon V NLRC GR 154376Document9 pagesDomondon V NLRC GR 154376naldsdomingoNo ratings yet

- Heirs of Tan Uy V International Exchange BankDocument6 pagesHeirs of Tan Uy V International Exchange BanknaldsdomingoNo ratings yet

- Dioquino V Cruz - Full CaseDocument5 pagesDioquino V Cruz - Full CasenaldsdomingoNo ratings yet

- Ker & Co. V LingadDocument4 pagesKer & Co. V LingadnaldsdomingoNo ratings yet

- Amigo V Teves - Full TextDocument5 pagesAmigo V Teves - Full TextnaldsdomingoNo ratings yet

- Zaragoza V CADocument6 pagesZaragoza V CAnaldsdomingoNo ratings yet

- Eviota V CA GR 152121Document13 pagesEviota V CA GR 152121naldsdomingoNo ratings yet

- Obana Vs CA DigestDocument1 pageObana Vs CA DigestnaldsdomingoNo ratings yet

- Serra Vs CA DigestDocument2 pagesSerra Vs CA DigestnaldsdomingoNo ratings yet

- Sulo Sa Nayon V Nayong FilipinoDocument12 pagesSulo Sa Nayon V Nayong Filipinonaldsdomingo0% (1)

- Reodica V CADocument10 pagesReodica V CAnaldsdomingoNo ratings yet

- RR 8-2007Document2 pagesRR 8-2007naldsdomingoNo ratings yet

- Ocampo V CA - DigestDocument3 pagesOcampo V CA - Digestnaldsdomingo33% (3)

- Areola V CA - DigestDocument2 pagesAreola V CA - DigestnaldsdomingoNo ratings yet

- Amendment Vat 2Document22 pagesAmendment Vat 2jonefjonepNo ratings yet

- "Section 3. - COVERAGE.-xxx XXX XXXDocument2 pages"Section 3. - COVERAGE.-xxx XXX XXXnaldsdomingoNo ratings yet

- RR 9-2007Document3 pagesRR 9-2007naldsdomingoNo ratings yet

- Aulia Safa Fariski - 19080304049 - Pak 2019-I Journal Worksheet Kasus-2aDocument12 pagesAulia Safa Fariski - 19080304049 - Pak 2019-I Journal Worksheet Kasus-2aaulia safafNo ratings yet

- Chapter 4 - Forms of Business OrganizationDocument24 pagesChapter 4 - Forms of Business Organizationairam cabadduNo ratings yet

- Burj Malabar Auto Maint.: Tax InvoiceDocument1 pageBurj Malabar Auto Maint.: Tax InvoiceburjmalabarautoNo ratings yet

- ECS Mandate FormDocument2 pagesECS Mandate FormManoj PatiyalNo ratings yet

- CH 4 Income From House PropertyDocument89 pagesCH 4 Income From House PropertyPratyashNo ratings yet

- Aadhar Pay Reports Govt's (USRPAY) 12.3.19Document5 pagesAadhar Pay Reports Govt's (USRPAY) 12.3.19charsaubees420No ratings yet

- Bir Ruling 128-99Document2 pagesBir Ruling 128-99001nooneNo ratings yet

- First Data Annual Report 2011Document178 pagesFirst Data Annual Report 2011SteveMastersNo ratings yet

- Auditing The Expenditure Cycle: Kelompok 5Document18 pagesAuditing The Expenditure Cycle: Kelompok 5mrevitasariNo ratings yet

- Cfap 5 2020 PKDocument192 pagesCfap 5 2020 PKShafeyAliKhanNo ratings yet

- SunitaDocument4 pagesSunitaNikhil OjhaNo ratings yet

- SalaryDocument80 pagesSalarykalyanikamineniNo ratings yet

- Online Training Calendar July - September 2021: Sitrain - Digital Industry AcademyDocument3 pagesOnline Training Calendar July - September 2021: Sitrain - Digital Industry AcademyM MaheshNo ratings yet

- US Internal Revenue Service: f8835 - 2000Document3 pagesUS Internal Revenue Service: f8835 - 2000IRSNo ratings yet

- Module 16 17Document5 pagesModule 16 17Znyx Aleli Jazmin-MarianoNo ratings yet

- 2022 142 Taxmann Com 414 Mumbai Trib 20 09 2022Document2 pages2022 142 Taxmann Com 414 Mumbai Trib 20 09 2022ABCNo ratings yet

- Elephant Design Proforma InvoiceDocument1 pageElephant Design Proforma InvoiceRamdas NagareNo ratings yet

- General Principles: Estate Tax Vs Donor's Tax Estate Tax Donor'S TaxDocument3 pagesGeneral Principles: Estate Tax Vs Donor's Tax Estate Tax Donor'S TaxKenneth Mataban100% (1)

- Grade 12 (Business Math)Document2 pagesGrade 12 (Business Math)Luz Gracia OyaoNo ratings yet

- Pci Vs CADocument1 pagePci Vs CASheilah Mae PadallaNo ratings yet

- Tax Assignment 1Document8 pagesTax Assignment 1Jiaxi WNo ratings yet

- Tax - Notes - Inclusions and ExclusionsDocument11 pagesTax - Notes - Inclusions and ExclusionsCamille Danielle BarbadoNo ratings yet

- Annualization For Alphalist 2017-2020Document18 pagesAnnualization For Alphalist 2017-2020AEC IncorpNo ratings yet

- PFMS Generated Print Payment Advice: To, The Branch HeadDocument1 pagePFMS Generated Print Payment Advice: To, The Branch HeadHarsh VarshneyNo ratings yet

- Hatta Land Border 05/06/2022 DECIDF0506227306706: Oman Dry Dock Company LLCDocument2 pagesHatta Land Border 05/06/2022 DECIDF0506227306706: Oman Dry Dock Company LLCMaan JuttNo ratings yet

- Ketanna HasLab Star Wars PDFDocument1 pageKetanna HasLab Star Wars PDFSantiago Cabarcas L. de UrquizoNo ratings yet

- Colorado Feedlot Horses Fein PapersDocument3 pagesColorado Feedlot Horses Fein Papersapi-270147093No ratings yet

- TTD Accommodation ReceiptDocument2 pagesTTD Accommodation ReceiptDharani KumarNo ratings yet

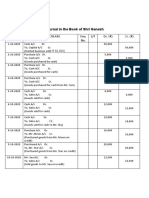

- Journal in The Book of Shri Ganesh: Date Particulars Vou. No. L/F Dr. Cr.Document4 pagesJournal in The Book of Shri Ganesh: Date Particulars Vou. No. L/F Dr. Cr.Anuj GohainNo ratings yet

- Exide Life Smart Term Plan-Fri Dec 15 12-24-27 IST 2017Document6 pagesExide Life Smart Term Plan-Fri Dec 15 12-24-27 IST 2017abc defNo ratings yet