Australia Deregulation

Australia Deregulation

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Menta Bangun Made Anta Ridzky Arya Sudono: March, 2010Document18 pagesMenta Bangun Made Anta Ridzky Arya Sudono: March, 2010arya_85No ratings yet

- Letter To BirDocument2 pagesLetter To BirlhemnavalNo ratings yet

- Project Report On Online Class SystemDocument91 pagesProject Report On Online Class Systemapurva singh100% (1)

- Motion For Summary JudgmentDocument27 pagesMotion For Summary JudgmentKING 5 News100% (1)

- EC744 Lecture Note 1: Prof. Jianjun MiaoDocument18 pagesEC744 Lecture Note 1: Prof. Jianjun MiaobinicleNo ratings yet

- Iso Ts 16949 Semiconductor CommodityDocument24 pagesIso Ts 16949 Semiconductor Commoditydyogasara2No ratings yet

- Employment Contract Gomez FinalDocument15 pagesEmployment Contract Gomez Finalartemio villasNo ratings yet

- Accounting Standards: Sub: Financial Reporting & AnalysisDocument13 pagesAccounting Standards: Sub: Financial Reporting & AnalysisDevasaya MitraNo ratings yet

- ABM 002 Teacher Day 17Document9 pagesABM 002 Teacher Day 17Darelle Hannah MarquezNo ratings yet

- QAD Procedure - Control of Non-Conforming Products P1Document1 pageQAD Procedure - Control of Non-Conforming Products P1sumanNo ratings yet

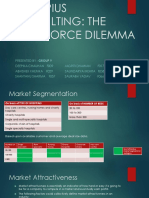

- Asclepius Consulting - Group 9Document14 pagesAsclepius Consulting - Group 9TryNo ratings yet

- Value World Fall 2013Document49 pagesValue World Fall 2013bimoNo ratings yet

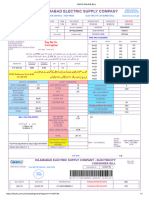

- Iesco Online Bill23Document1 pageIesco Online Bill23aamir ShahzadNo ratings yet

- Business Ethics, Corporate Social Responsibility and Importance of Implementation of CSR at CorporationsDocument40 pagesBusiness Ethics, Corporate Social Responsibility and Importance of Implementation of CSR at CorporationsPika ChuNo ratings yet

- Project Report ON: Financial Analysis of DLF, Unitech & Ansal ApiDocument61 pagesProject Report ON: Financial Analysis of DLF, Unitech & Ansal Apiprachi158No ratings yet

- Complete Income Generating Project in SchoolDocument78 pagesComplete Income Generating Project in SchoolEcila DigoNo ratings yet

- List of DVMFXDKBFG Program 02132024Document300 pagesList of DVMFXDKBFG Program 02132024Rhoanne SisonNo ratings yet

- ChoiceListReport - TT - PDF of ShifaDocument1 pageChoiceListReport - TT - PDF of ShifaAbdur Rahman AbdullahNo ratings yet

- The Women 2012Document5 pagesThe Women 2012Christopher MartinNo ratings yet

- CH 12Document30 pagesCH 12ReneeNo ratings yet

- Insider TradingDocument4 pagesInsider TradingAnusha SimhaNo ratings yet

- Digests, R62 R66Document27 pagesDigests, R62 R66lonitsuafNo ratings yet

- Admission Capital AdjustmentsDocument6 pagesAdmission Capital AdjustmentsHamza MudassirNo ratings yet

- Answers With Explanation Indian Economy BasicsDocument5 pagesAnswers With Explanation Indian Economy BasicsrahulNo ratings yet

- Operations Management - Capacity Planning and Control Sample PDFDocument3 pagesOperations Management - Capacity Planning and Control Sample PDFQuincy RileyNo ratings yet

- Knowledge Management As A DoughnutDocument7 pagesKnowledge Management As A DoughnutNigel Psalm YapNo ratings yet

- Theories of Interest RateDocument10 pagesTheories of Interest RateAshutoshNo ratings yet

- Total Gadha NumbersDocument11 pagesTotal Gadha NumbersSaket Shahi0% (1)

- GSIS Annual Report For 2009Document64 pagesGSIS Annual Report For 2009vlamuning06No ratings yet

- Cbse Class 11 Business Studies Sample Paper Set 1 QuestionsDocument2 pagesCbse Class 11 Business Studies Sample Paper Set 1 QuestionsNandini AgarwalNo ratings yet

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Menta Bangun Made Anta Ridzky Arya Sudono: March, 2010Document18 pagesMenta Bangun Made Anta Ridzky Arya Sudono: March, 2010arya_85No ratings yet

- Letter To BirDocument2 pagesLetter To BirlhemnavalNo ratings yet

- Project Report On Online Class SystemDocument91 pagesProject Report On Online Class Systemapurva singh100% (1)

- Motion For Summary JudgmentDocument27 pagesMotion For Summary JudgmentKING 5 News100% (1)

- EC744 Lecture Note 1: Prof. Jianjun MiaoDocument18 pagesEC744 Lecture Note 1: Prof. Jianjun MiaobinicleNo ratings yet

- Iso Ts 16949 Semiconductor CommodityDocument24 pagesIso Ts 16949 Semiconductor Commoditydyogasara2No ratings yet

- Employment Contract Gomez FinalDocument15 pagesEmployment Contract Gomez Finalartemio villasNo ratings yet

- Accounting Standards: Sub: Financial Reporting & AnalysisDocument13 pagesAccounting Standards: Sub: Financial Reporting & AnalysisDevasaya MitraNo ratings yet

- ABM 002 Teacher Day 17Document9 pagesABM 002 Teacher Day 17Darelle Hannah MarquezNo ratings yet

- QAD Procedure - Control of Non-Conforming Products P1Document1 pageQAD Procedure - Control of Non-Conforming Products P1sumanNo ratings yet

- Asclepius Consulting - Group 9Document14 pagesAsclepius Consulting - Group 9TryNo ratings yet

- Value World Fall 2013Document49 pagesValue World Fall 2013bimoNo ratings yet

- Iesco Online Bill23Document1 pageIesco Online Bill23aamir ShahzadNo ratings yet

- Business Ethics, Corporate Social Responsibility and Importance of Implementation of CSR at CorporationsDocument40 pagesBusiness Ethics, Corporate Social Responsibility and Importance of Implementation of CSR at CorporationsPika ChuNo ratings yet

- Project Report ON: Financial Analysis of DLF, Unitech & Ansal ApiDocument61 pagesProject Report ON: Financial Analysis of DLF, Unitech & Ansal Apiprachi158No ratings yet

- Complete Income Generating Project in SchoolDocument78 pagesComplete Income Generating Project in SchoolEcila DigoNo ratings yet

- List of DVMFXDKBFG Program 02132024Document300 pagesList of DVMFXDKBFG Program 02132024Rhoanne SisonNo ratings yet

- ChoiceListReport - TT - PDF of ShifaDocument1 pageChoiceListReport - TT - PDF of ShifaAbdur Rahman AbdullahNo ratings yet

- The Women 2012Document5 pagesThe Women 2012Christopher MartinNo ratings yet

- CH 12Document30 pagesCH 12ReneeNo ratings yet

- Insider TradingDocument4 pagesInsider TradingAnusha SimhaNo ratings yet

- Digests, R62 R66Document27 pagesDigests, R62 R66lonitsuafNo ratings yet

- Admission Capital AdjustmentsDocument6 pagesAdmission Capital AdjustmentsHamza MudassirNo ratings yet

- Answers With Explanation Indian Economy BasicsDocument5 pagesAnswers With Explanation Indian Economy BasicsrahulNo ratings yet

- Operations Management - Capacity Planning and Control Sample PDFDocument3 pagesOperations Management - Capacity Planning and Control Sample PDFQuincy RileyNo ratings yet

- Knowledge Management As A DoughnutDocument7 pagesKnowledge Management As A DoughnutNigel Psalm YapNo ratings yet

- Theories of Interest RateDocument10 pagesTheories of Interest RateAshutoshNo ratings yet

- Total Gadha NumbersDocument11 pagesTotal Gadha NumbersSaket Shahi0% (1)

- GSIS Annual Report For 2009Document64 pagesGSIS Annual Report For 2009vlamuning06No ratings yet

- Cbse Class 11 Business Studies Sample Paper Set 1 QuestionsDocument2 pagesCbse Class 11 Business Studies Sample Paper Set 1 QuestionsNandini AgarwalNo ratings yet