You might also like

- Airbus B-E Analysis ModelDocument5 pagesAirbus B-E Analysis ModelTran Tuan Linh100% (3)

- Airbus Calulation TemplateDocument4 pagesAirbus Calulation TemplateKumar VikasNo ratings yet

- Boeing 7E7 Case Study SolutionDocument18 pagesBoeing 7E7 Case Study Solutionaqueel7389% (28)

- Boeing 777 CaseStudy SolutionDocument3 pagesBoeing 777 CaseStudy SolutionRohit Parnerkar80% (5)

- DuPont Corporation Sale of Performance CoatingsDocument1 pageDuPont Corporation Sale of Performance Coatingsj2203950% (2)

- TN16 The Boeing 7E7Document27 pagesTN16 The Boeing 7E7Stanleylan100% (5)

- FINAN 6220 - Target Case Study AnswersDocument2 pagesFINAN 6220 - Target Case Study AnswerschandanaNo ratings yet

- Estimation of Cost of Capital: Case: The Boeing 7E7Document125 pagesEstimation of Cost of Capital: Case: The Boeing 7E7jk kumarNo ratings yet

- Boeing 7E7 Case StudyDocument5 pagesBoeing 7E7 Case Studymrc2000100% (1)

- Seminar Questions For The Boeing 7E7 CaseDocument2 pagesSeminar Questions For The Boeing 7E7 CaseLucasNo ratings yet

- Pressco Case MemoDocument7 pagesPressco Case Memotodenheim0% (3)

- Pressco Inc. Case StudyDocument19 pagesPressco Inc. Case StudyIrakli SaliaNo ratings yet

- Diageo Case Write UpDocument10 pagesDiageo Case Write UpAmandeep AroraNo ratings yet

- Case Analysis Embraer FinalDocument17 pagesCase Analysis Embraer Finalfossaceca67% (3)

- Data Import Template BLDocument94 pagesData Import Template BLdavender kumarNo ratings yet

- Boeing 7E7Document3 pagesBoeing 7E7Justin Zak100% (9)

- 1 Heinz Case StudyDocument8 pages1 Heinz Case Studysachin2727100% (2)

- Nike Cost of CapitalDocument2 pagesNike Cost of CapitalYou VeeNo ratings yet

- Nike Inc. Cost of Capital Case AnalysisDocument7 pagesNike Inc. Cost of Capital Case Analysisrmdelmando100% (6)

- Nike Case Final Group 4Document15 pagesNike Case Final Group 4Monika Maheshwari100% (1)

- Questions:: 1. Is Mercury An Appropriate Target For AGI? Why or Why Not?Document5 pagesQuestions:: 1. Is Mercury An Appropriate Target For AGI? Why or Why Not?Cuong NguyenNo ratings yet

- Airbus SpreadsheetDocument27 pagesAirbus SpreadsheetAnnie CondeNo ratings yet

- The Boeing 7E7Document8 pagesThe Boeing 7E7Irka Dewi Tanemaru100% (1)

- The Boeing 7E7Document8 pagesThe Boeing 7E7AmandaNo ratings yet

- Team 14 - Boeing 7E7Document10 pagesTeam 14 - Boeing 7E7Niken PramestiNo ratings yet

- Boeing 777Document5 pagesBoeing 777Tanvir Ahmed100% (1)

- Case 1Document4 pagesCase 1liyulongNo ratings yet

- AirbusDocument3 pagesAirbusHP KawaleNo ratings yet

- New Heritage Doll CompanyDocument5 pagesNew Heritage Doll CompanyRahul LalwaniNo ratings yet

- Crocs Case AnalysisDocument8 pagesCrocs Case Analysissiddis316No ratings yet

- 787 Financial AnalysisDocument25 pages787 Financial AnalysisJason MakowskiNo ratings yet

- Wrigley CaseDocument12 pagesWrigley Caseresat gürNo ratings yet

- FINAL Boeing Case Study (Group 4) 26042014Document29 pagesFINAL Boeing Case Study (Group 4) 26042014Amey WarudeNo ratings yet

- The Boeing 7E7 - Write UpDocument6 pagesThe Boeing 7E7 - Write UpVern CabreraNo ratings yet

- Team 14 - Boeing 7E7 - Very GoodDocument10 pagesTeam 14 - Boeing 7E7 - Very GoodAddler PluvioseNo ratings yet

- Team 14 - Boeing 7E7Document10 pagesTeam 14 - Boeing 7E7sam30121989No ratings yet

- Team 14 - Boeing 7E7Document10 pagesTeam 14 - Boeing 7E7Tommy Suryo100% (1)

- Boeing Analysis: Index BusinessDocument7 pagesBoeing Analysis: Index BusinessPang Chun100% (1)

- Boeing Case FinalDocument13 pagesBoeing Case Finalapi-247303303100% (1)

- Boeing 7E7Document3 pagesBoeing 7E7angecorin_527302262No ratings yet

- Nike, IncDocument19 pagesNike, IncRavi PrakashNo ratings yet

- Airbus A3XXDocument2 pagesAirbus A3XXPriyanka Agarwal0% (1)

- Friendly CS SolutionDocument8 pagesFriendly CS SolutionEfendiNo ratings yet

- DuPont QuestionsDocument1 pageDuPont QuestionssandykakaNo ratings yet

- Word Note Boeing 7E7 Case AnalysisDocument3 pagesWord Note Boeing 7E7 Case Analysisalka murarka75% (4)

- The Wm. Wrigley Jr. Company: Capital Structure, Valuation and Cost of CapitalDocument19 pagesThe Wm. Wrigley Jr. Company: Capital Structure, Valuation and Cost of CapitalMai Pham100% (1)

- Airbus TemplateDocument2 pagesAirbus Templateveda20No ratings yet

- Analysis Slides-WACC NikeDocument25 pagesAnalysis Slides-WACC NikePei Chin100% (3)

- Nike Inc. Case StudyDocument3 pagesNike Inc. Case Studyshikhagupta3288No ratings yet

- California Pizza Kitchen Rev2Document7 pagesCalifornia Pizza Kitchen Rev2ahmed mahmoud100% (1)

- Stephanie Ott Advanced Corporate Finance Midterm The Boeing 777Document11 pagesStephanie Ott Advanced Corporate Finance Midterm The Boeing 777Steph OttNo ratings yet

- WrigleyDocument28 pagesWrigleyKaran Rana100% (1)

- Case Nike - Cost of Capital Fix 1Document9 pagesCase Nike - Cost of Capital Fix 1Yousania RatuNo ratings yet

- Boeing & Airbus Case StudyDocument35 pagesBoeing & Airbus Case StudydeepakNo ratings yet

- Case Study 1Document5 pagesCase Study 1PrincessNo ratings yet

- External Analysis Boeing Assignment Final 2Document7 pagesExternal Analysis Boeing Assignment Final 2Himmie Eugene LangfordNo ratings yet

- Airbus PortersFF RuheeDocument2 pagesAirbus PortersFF RuheeNabila TabassumNo ratings yet

- Case Analysis EmbraerDocument14 pagesCase Analysis EmbraerfossacecaNo ratings yet

- Case Study Analysis Commercial Airline Industry: Airbus & BoeingDocument17 pagesCase Study Analysis Commercial Airline Industry: Airbus & BoeingShone ThattilNo ratings yet

- SM2 FinA1 Grp6 BoeingDocument11 pagesSM2 FinA1 Grp6 Boeingabhi2shek2003100% (1)

- Boeing 787 Case StudyDocument17 pagesBoeing 787 Case StudyJosh Krisha100% (1)

- Raibha Agra Bypass 2703 DT 17082016Document6 pagesRaibha Agra Bypass 2703 DT 17082016Juned QureshiNo ratings yet

- SCM - Manufacturing Cloud: Update 21B OverviewDocument26 pagesSCM - Manufacturing Cloud: Update 21B OverviewSAINTJOE100% (1)

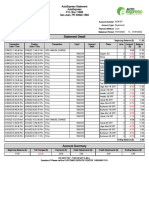

- Statement Detail: Autoexpreso Statement Autoexpreso P.O. Box 11888 San Juan, PR 00922-1888Document1 pageStatement Detail: Autoexpreso Statement Autoexpreso P.O. Box 11888 San Juan, PR 00922-1888alfredo velezNo ratings yet

- Canara - Epassbook - 2023-11-02 200708.530629Document95 pagesCanara - Epassbook - 2023-11-02 200708.530629manojsailor855No ratings yet

- Chapter - Iii Theoretical Framework of Financial Literacy and Financial Well-BeingDocument28 pagesChapter - Iii Theoretical Framework of Financial Literacy and Financial Well-Beingpooja shandilyaNo ratings yet

- IAS 30 and IFRS 7 CPA Anthony NjiruDocument51 pagesIAS 30 and IFRS 7 CPA Anthony NjiruMovie MovieNo ratings yet

- Manufacturing Performance Improvement Through Lean Production-2009Document11 pagesManufacturing Performance Improvement Through Lean Production-2009Juan BarronNo ratings yet

- Instructions: How To Use This TemplateDocument20 pagesInstructions: How To Use This TemplatemarsredjoNo ratings yet

- Uganda Public Finance Management Regulations, 2016Document24 pagesUganda Public Finance Management Regulations, 2016African Centre for Media Excellence100% (19)

- PrzysuskiM BerryRatioPaperDocument10 pagesPrzysuskiM BerryRatioPapersuperandrosaNo ratings yet

- Introduction To Entrepreneurship I (Elective) : MyinfoDocument4 pagesIntroduction To Entrepreneurship I (Elective) : MyinfoMichelle F. De GuzmanNo ratings yet

- Training - India PayrollDocument18 pagesTraining - India Payrollyenumula_inNo ratings yet

- Forms of Small Business OwnershipDocument38 pagesForms of Small Business OwnershipPatrick Brillante DeleonNo ratings yet

- Financial Delegated Authorities Policy: 1 PurposeDocument10 pagesFinancial Delegated Authorities Policy: 1 PurposetinmaungtheinNo ratings yet

- BandathimmapurDocument5 pagesBandathimmapurnagatejaNo ratings yet

- Irc SP 112-2017Document113 pagesIrc SP 112-2017Sanjay67% (9)

- Business HistoryDocument34 pagesBusiness HistorySamar Khanna GaorankhaNo ratings yet

- 2012 Index of Economic FreedomDocument483 pages2012 Index of Economic FreedomJose Carbonell SanchezNo ratings yet

- Afsar Raza CVDocument2 pagesAfsar Raza CVWaqas Malook KhattakNo ratings yet

- Crc-Ace Review School: TAXATION (1-70)Document10 pagesCrc-Ace Review School: TAXATION (1-70)LuisitoNo ratings yet

- Epm Course Outline 20 - 21 Bcom-BbaDocument2 pagesEpm Course Outline 20 - 21 Bcom-BbaIanNo ratings yet

- Module 2 - Fabm 1Document9 pagesModule 2 - Fabm 1Kurt Llessur Sid-ingNo ratings yet

- CLAY - Citra Putra Realty TBK.: Quarter (YTD)Document1 pageCLAY - Citra Putra Realty TBK.: Quarter (YTD)farialNo ratings yet

- Variable and Absorption M 02Document6 pagesVariable and Absorption M 02sm munNo ratings yet

- Inter Preneur ShipDocument135 pagesInter Preneur Shipkaran kushwahNo ratings yet

- Nestle Pakistan Research Project!!Document29 pagesNestle Pakistan Research Project!!Hassan Naeem89% (18)

- Sea Park Ayurvedic Beach ResortDocument16 pagesSea Park Ayurvedic Beach ResortFletcher Caroline JoyNo ratings yet

- BUS 698 Course Career Path Begins Bus698dotcomDocument20 pagesBUS 698 Course Career Path Begins Bus698dotcomEssayest2No ratings yet

- Business Plan For Plastic in Ethiopia DoDocument38 pagesBusiness Plan For Plastic in Ethiopia DofekadeNo ratings yet