You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 6 Laning of Pimpalgaon Nashik Gonde Vol. IIDocument260 pages6 Laning of Pimpalgaon Nashik Gonde Vol. IIshuttel_lifeNo ratings yet

- Timeline: The Press-Enterprise - Part 2Document1 pageTimeline: The Press-Enterprise - Part 2The Press-Enterprise / pressenterprise.comNo ratings yet

- Foreign Exchange Hedging Strategies at General MotorsDocument10 pagesForeign Exchange Hedging Strategies at General MotorsHaninditaGuritnaNo ratings yet

- Hingna MidcDocument15 pagesHingna Midcshuttel_lifeNo ratings yet

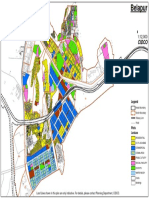

- BelapurDocument1 pageBelapurshuttel_life100% (1)

- 11 Chapter 4Document92 pages11 Chapter 4shuttel_lifeNo ratings yet

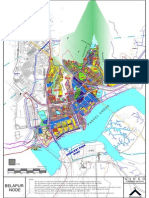

- BelapurDocument1 pageBelapurshuttel_lifeNo ratings yet

- Production and Marketing of Apple in Himachal Pradesh: An Empirical StudyDocument7 pagesProduction and Marketing of Apple in Himachal Pradesh: An Empirical StudyTinaNo ratings yet

- Keywords: Trading Suspension, Forced Delisting, Capital Market, Indonesia Stock ExchangeDocument25 pagesKeywords: Trading Suspension, Forced Delisting, Capital Market, Indonesia Stock ExchangeAlexander AgungNo ratings yet

- Plastic Fines in Graded Aggregates and Soils by Use of The Sand Equivalent TestDocument2 pagesPlastic Fines in Graded Aggregates and Soils by Use of The Sand Equivalent TestDiana MoscosoNo ratings yet

- Research Paper On Lean ManufacturingDocument5 pagesResearch Paper On Lean Manufacturingbsinababu1100% (2)

- C GTQ W4 N Pyvg PFedhDocument2 pagesC GTQ W4 N Pyvg PFedhAbhinav VermaNo ratings yet

- Business Organizations Grade 8: Private SectorDocument14 pagesBusiness Organizations Grade 8: Private SectorPrinceyoon22No ratings yet

- The BMW Group Corporate Fleet Program BrochureDocument2 pagesThe BMW Group Corporate Fleet Program BrochureNeil PottsNo ratings yet

- Wellshin Molded PlugDocument96 pagesWellshin Molded PlugtungNo ratings yet

- T.L.E. - Business 3rd Term ReviewerDocument12 pagesT.L.E. - Business 3rd Term ReviewerDaniel TorralbaNo ratings yet

- Commissioner of Internal Revenue, Petitioner, V. La Flor Dela Isabela, Inc., Respondent. DecisionDocument7 pagesCommissioner of Internal Revenue, Petitioner, V. La Flor Dela Isabela, Inc., Respondent. DecisionFrancis Coronel Jr.No ratings yet

- Bimstec: Download FromDocument4 pagesBimstec: Download FromTarun Kumar MahorNo ratings yet

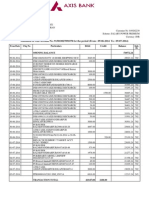

- Account StatementDocument2 pagesAccount StatementgobeyondskyNo ratings yet

- I.TAx 302Document4 pagesI.TAx 302tadepalli patanjaliNo ratings yet

- Open Checkbook Visualization - Group by VendorDocument175 pagesOpen Checkbook Visualization - Group by VendorGaniyou AdenidjiNo ratings yet

- W-8BEN: Vinicius Nascimento BittencourtDocument1 pageW-8BEN: Vinicius Nascimento BittencourtVinicius Nascimento BittencourtNo ratings yet

- Degaradtion Forest and Unemployment: Towards Small Scale Forest ManagementDocument13 pagesDegaradtion Forest and Unemployment: Towards Small Scale Forest ManagementMuhammadArmy ChairuddinNo ratings yet

- ECO111 Assignment1Document2 pagesECO111 Assignment1Nguyễn HoaNo ratings yet

- IELTS Writing Task 1Document42 pagesIELTS Writing Task 1Lokesh Konganapalle93% (14)

- SIMULUS 8 Offline RegistrationDocument8 pagesSIMULUS 8 Offline RegistrationNeutral Body NursingNo ratings yet

- FY 2019 Summary Prpoposed Progams/Projects (In Thousand Pesos) School/Divison Tier 1 Tier 2 PS Mooe CO Rlip Total PS Mooe CO Mayag Nhs (JHS) 354Document34 pagesFY 2019 Summary Prpoposed Progams/Projects (In Thousand Pesos) School/Divison Tier 1 Tier 2 PS Mooe CO Rlip Total PS Mooe CO Mayag Nhs (JHS) 354Lex AmarieNo ratings yet

- State Wise GST Number of IRCTCDocument1 pageState Wise GST Number of IRCTCStNo ratings yet

- POPAI Awards Book 2013Document60 pagesPOPAI Awards Book 2013raheelehsanNo ratings yet

- 244-Gcsa QBDocument17 pages244-Gcsa QBjeet_singh_deepNo ratings yet

- India Warehousing Market Report 2021Document98 pagesIndia Warehousing Market Report 2021starmine@rediffmail.comNo ratings yet

- Guidelines For Watershed AssociationDocument3 pagesGuidelines For Watershed Associationsatyaguru1971No ratings yet

- Lecture 05 - Exchange Rate DeterminationDocument7 pagesLecture 05 - Exchange Rate DeterminationTrương Ngọc Minh ĐăngNo ratings yet

- Economics - WikipediaDocument42 pagesEconomics - WikipediakamaalNo ratings yet

- Training Manual November 2007 PDFDocument112 pagesTraining Manual November 2007 PDFJune AlapaNo ratings yet