You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Comparative Analysis of Financial Statement of Two CompaniesDocument24 pagesComparative Analysis of Financial Statement of Two Companiesrexieace75% (4)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Curled Metal IncDocument3 pagesCurled Metal IncNiharika padmanabhanNo ratings yet

- BHP Billiton CaseDocument30 pagesBHP Billiton CaseMonjurul Hassan100% (2)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Egger's Roast CoffeeDocument21 pagesEgger's Roast CoffeeemedinillaNo ratings yet

- Krajewski TIF Chapter 10Document26 pagesKrajewski TIF Chapter 10Güítår Hêárt100% (2)

- MKT Nature View FarmDocument17 pagesMKT Nature View FarmnamzrulzNo ratings yet

- 1370 Application For Special Admission To Membership FAiDocument10 pages1370 Application For Special Admission To Membership FAiMonjurul HassanNo ratings yet

- Corpoarte Stratgies HASANDocument11 pagesCorpoarte Stratgies HASANMonjurul HassanNo ratings yet

- Assumption A - The Fair Value of The Old Air Conditioning System at The Time of Acquiring The Facility Was NIS 10Document1 pageAssumption A - The Fair Value of The Old Air Conditioning System at The Time of Acquiring The Facility Was NIS 10Monjurul HassanNo ratings yet

- VAT and SD Act 2012 EnglishDocument91 pagesVAT and SD Act 2012 EnglishMonjurul HassanNo ratings yet

- Arabic Vocabulary Bank: (Madinah Book 1 Chapter 1-23)Document29 pagesArabic Vocabulary Bank: (Madinah Book 1 Chapter 1-23)mazad1985No ratings yet

- IAS 37 Provisions, Contingent Liabilities and Contingent AssetsDocument6 pagesIAS 37 Provisions, Contingent Liabilities and Contingent AssetsMonjurul HassanNo ratings yet

- I Wrote This Poem So I Can Learn A Bit of Chem. I Hope You Enjoy These Few Lines of (Ahh I'm Out of Rhymes)Document1 pageI Wrote This Poem So I Can Learn A Bit of Chem. I Hope You Enjoy These Few Lines of (Ahh I'm Out of Rhymes)Monjurul HassanNo ratings yet

- DBZ Theme PDFDocument8 pagesDBZ Theme PDFMonjurul HassanNo ratings yet

- BangladeshDocument3 pagesBangladeshMonjurul HassanNo ratings yet

- TDS CodeDocument1 pageTDS CodeMonjurul HassanNo ratings yet

- Mkt337 PresentationDocument31 pagesMkt337 PresentationSyedSalmanRahmanNo ratings yet

- Product Life Cycle - Case StudyDocument2 pagesProduct Life Cycle - Case StudyPurav RiatNo ratings yet

- Firm Behaviour: Microeconomics (Exercises)Document9 pagesFirm Behaviour: Microeconomics (Exercises)Камилла МолдалиеваNo ratings yet

- In The Calculation of Return On Shareholders Investments The Referred Investment Deals WithDocument20 pagesIn The Calculation of Return On Shareholders Investments The Referred Investment Deals WithAnilKumarNo ratings yet

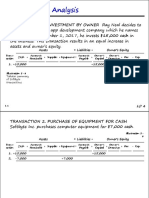

- Transaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToDocument31 pagesTransaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToSophia LocreNo ratings yet

- Cases in Finance - FIN 200Document3 pagesCases in Finance - FIN 200avegaNo ratings yet

- Mike IKEA CaseDocument3 pagesMike IKEA CaseMichael HarringtonNo ratings yet

- ProQuestDocuments 2013 03 08Document147 pagesProQuestDocuments 2013 03 08Oktaria MayasariNo ratings yet

- Economic Consequences and Positive Accounting TheoryDocument24 pagesEconomic Consequences and Positive Accounting TheorysethnurulmnNo ratings yet

- Pizza HutDocument26 pagesPizza Hutعبدالرحمن الحماديNo ratings yet

- Internship Report On An Analysis of Marketing Activities of Biswas Builders LimitedDocument44 pagesInternship Report On An Analysis of Marketing Activities of Biswas Builders LimitedNoman ParvezNo ratings yet

- Case Study - ActDocument10 pagesCase Study - ActJohnloyd daracanNo ratings yet

- Productivity - NotesDocument16 pagesProductivity - Notesjac bnvstaNo ratings yet

- Literature Review: A) Theoretical FrameworkDocument4 pagesLiterature Review: A) Theoretical FrameworkCALVIN GOMEZNo ratings yet

- Analytical Review ProceduresDocument5 pagesAnalytical Review ProceduresnderitulinetNo ratings yet

- Supply Chain of Oil and GasDocument4 pagesSupply Chain of Oil and GasNitin BighaneNo ratings yet

- Ucsp 11 Mod. 7 Answer KeyDocument5 pagesUcsp 11 Mod. 7 Answer KeyJOHN GLENLY PILLAZO MAHUSAYNo ratings yet

- Landed Costs SAP B1Document18 pagesLanded Costs SAP B1sehemNo ratings yet

- CH 09Document84 pagesCH 09trang lêNo ratings yet

- DsaddDocument2 pagesDsaddVel JuneNo ratings yet

- ICTC Training Program: Cc-By-Nc-SaDocument43 pagesICTC Training Program: Cc-By-Nc-SaEric TeoNo ratings yet

- Influencer Marketing PresentationDocument5 pagesInfluencer Marketing Presentationjaimadhwa.accNo ratings yet

- SPORTSDocument30 pagesSPORTSlenny.brosse04No ratings yet

- Unit 1.1 Nature of Business ActivityDocument40 pagesUnit 1.1 Nature of Business ActivityroshanNo ratings yet

- ch04 - SM - Rankin - 2e MeasurementDocument18 pagesch04 - SM - Rankin - 2e MeasurementU2003053 STUDENTNo ratings yet