You might also like

- Manual Do UsuDocument500 pagesManual Do UsuRod Sb0% (1)

- Law Relating To Corporate Social ResponsibilityDocument12 pagesLaw Relating To Corporate Social ResponsibilityShivam RazorNo ratings yet

- CSR Project MergedDocument7 pagesCSR Project Mergedsyedsabafatima220No ratings yet

- ApplicabilityDocument4 pagesApplicabilityvasantharaoNo ratings yet

- Punjab Alkalies and Chemicals LTDDocument4 pagesPunjab Alkalies and Chemicals LTDAshrafNo ratings yet

- CSR - A Panoramic View - DR Bhasker ChatterjiDocument39 pagesCSR - A Panoramic View - DR Bhasker ChatterjicodemakitNo ratings yet

- Corporate Social ResponsibilityDocument6 pagesCorporate Social ResponsibilitycompetitivechahatNo ratings yet

- Corporate Social Responsibility 2013Document8 pagesCorporate Social Responsibility 2013sanjeevseshannaNo ratings yet

- Corporate Social ResponsibilityDocument7 pagesCorporate Social ResponsibilitySiva Sankar SanthoshNo ratings yet

- CSR Policy PDFDocument12 pagesCSR Policy PDFAkanksha DhandareNo ratings yet

- Corporate Social Responsibility in India Amity ProjectDocument4 pagesCorporate Social Responsibility in India Amity ProjectSanjay GroverNo ratings yet

- Section 135 of Companies Act For Corporate Social Responsibility - TDocument3 pagesSection 135 of Companies Act For Corporate Social Responsibility - TVivek ANo ratings yet

- Unit - 5 Study Material ACGDocument16 pagesUnit - 5 Study Material ACGAbhijeet UpadhyayNo ratings yet

- Corporate Social ResponsibilityDocument24 pagesCorporate Social ResponsibilityNaveen MettaNo ratings yet

- Company CSR Policy As Per Section 135 (4) - 24072018Document6 pagesCompany CSR Policy As Per Section 135 (4) - 24072018rajesh uluwatuNo ratings yet

- Corporate Social Responsibility RevisedDocument12 pagesCorporate Social Responsibility RevisedVipul NarwalNo ratings yet

- Chapter 3Document16 pagesChapter 3Mayank SenNo ratings yet

- Company Law CIA III CSRDocument6 pagesCompany Law CIA III CSRVedant GoswamiNo ratings yet

- Corporate Social ResponsibiltityDocument75 pagesCorporate Social ResponsibiltityyeshaNo ratings yet

- CSR NotesDocument14 pagesCSR NotesMallik SVNo ratings yet

- CSR PolicyDocument14 pagesCSR PolicyJilla Vishwas100% (1)

- Corporate Social Responsibility (CSR) Policy: Page 1 of 12Document12 pagesCorporate Social Responsibility (CSR) Policy: Page 1 of 12Shubham Jain ModiNo ratings yet

- Rar Unit 4Document12 pagesRar Unit 4raval123690No ratings yet

- Report On CSRDocument9 pagesReport On CSRVinay VimalNo ratings yet

- Company CSR Policy As Per Section 135 (4) - 17012020Document5 pagesCompany CSR Policy As Per Section 135 (4) - 17012020rajesh uluwatuNo ratings yet

- 1 Section 135 of ActDocument1 page1 Section 135 of ActLew BlumNo ratings yet

- CORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer LawrieDocument13 pagesCORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer Lawriekusum2016thadaNo ratings yet

- CSR PolicyDocument5 pagesCSR PolicyRitik SinghalNo ratings yet

- Corporate Social Responsibility (Section-135) : by Akhil Kodam 20464Document24 pagesCorporate Social Responsibility (Section-135) : by Akhil Kodam 20464Kodam AkhilNo ratings yet

- Corporate Social ResponsibilityDocument5 pagesCorporate Social Responsibilitypranavmenon19No ratings yet

- Twinings CSR PolicyDocument5 pagesTwinings CSR PolicyPyramid BalerNo ratings yet

- Corporate Social Responsibility Policy: Page 1 of 9Document9 pagesCorporate Social Responsibility Policy: Page 1 of 9Darshan KannurNo ratings yet

- Corporate Social Responsibility PolicyDocument5 pagesCorporate Social Responsibility PolicyRaaj SinghNo ratings yet

- Corporate Social ResponsibilityDocument33 pagesCorporate Social ResponsibilitySharma VishnuNo ratings yet

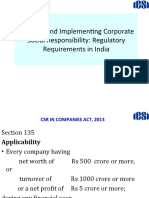

- Planning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaDocument23 pagesPlanning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaMuskan ManchandaNo ratings yet

- Warner Bros. Pictures (India) Private LimitedDocument8 pagesWarner Bros. Pictures (India) Private Limitedsaurav singhNo ratings yet

- CorpDocument3 pagesCorpMuskan KhatriNo ratings yet

- Legal Aspects of Business Corporate Social Responsibility: Management Development Institute, GurgaonDocument10 pagesLegal Aspects of Business Corporate Social Responsibility: Management Development Institute, GurgaonGautam BindlishNo ratings yet

- Policy For Corporate Social Responsibility of The Airports Authority of India-1Document56 pagesPolicy For Corporate Social Responsibility of The Airports Authority of India-1Manohar VennapusaNo ratings yet

- Franklin India CSR PolicyDocument7 pagesFranklin India CSR PolicyBhomik J ShahNo ratings yet

- AzureviewDocument6 pagesAzureviewshubham2904365No ratings yet

- Chapter 7Document5 pagesChapter 7Divyam sharma Roll no 175No ratings yet

- Timken - Corporate-Social-Responsibility-PolicyDocument5 pagesTimken - Corporate-Social-Responsibility-Policyadi.arrow7No ratings yet

- Wa0000.Document14 pagesWa0000.Nikhil KumarNo ratings yet

- CSR Policy FinalDocument4 pagesCSR Policy FinalNaresh khandelwalNo ratings yet

- SMEL Policy Doc CSR PolicyDocument7 pagesSMEL Policy Doc CSR Policyrounak sahuNo ratings yet

- CSR Rules Under Companies ActDocument10 pagesCSR Rules Under Companies ActSuperGuyNo ratings yet

- CSR LawDocument16 pagesCSR LawKarthikNo ratings yet

- Intex Tech India LTD-CSR PolicyDocument2 pagesIntex Tech India LTD-CSR PolicyBhomik J ShahNo ratings yet

- An Brief Overview On Corporate Social ResponsibilityDocument8 pagesAn Brief Overview On Corporate Social ResponsibilityMansangat Singh KohliNo ratings yet

- Section 135: Explanation.-For The Purposes of This Section "Average Net Profit" Shall Be CalculatedDocument1 pageSection 135: Explanation.-For The Purposes of This Section "Average Net Profit" Shall Be CalculatedNaveenNo ratings yet

- 0016 Avantika Tijare Assignment 2Document4 pages0016 Avantika Tijare Assignment 2AKSHAT SINGHNo ratings yet

- Microsoft Word - Compliance 2021 - DSL - RevisedDocument7 pagesMicrosoft Word - Compliance 2021 - DSL - RevisedSaikatmondalNo ratings yet

- Corporate Social ResponsibilityDocument8 pagesCorporate Social ResponsibilityBhareth Kumaran JNo ratings yet

- India's Mandatory CSR Law: Issues and Challenges: NavjeetDocument15 pagesIndia's Mandatory CSR Law: Issues and Challenges: NavjeetRohit KoulNo ratings yet

- CSR PolicyDocument8 pagesCSR PolicyChandra KumarNo ratings yet

- CSR20Final2002022015 Removed RemovedDocument6 pagesCSR20Final2002022015 Removed RemovedNeha MehtaNo ratings yet

- Module 03Document15 pagesModule 03Deepika SoniNo ratings yet

- MSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021Document11 pagesMSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021mgsalunke108No ratings yet

- Trend - IQVISIONv2 - 2 - Sales Presentation - As PresentedDocument42 pagesTrend - IQVISIONv2 - 2 - Sales Presentation - As PresentedPhangkie RecolizadoNo ratings yet

- How To Improve Listening b1Document5 pagesHow To Improve Listening b1malenatobeNo ratings yet

- Advanced Restorative Dentistry - PPT 3Document39 pagesAdvanced Restorative Dentistry - PPT 3Lim TechchhorngNo ratings yet

- Catalino Gallemit, vs. Ceferino Tabiliran: FactsDocument1 pageCatalino Gallemit, vs. Ceferino Tabiliran: Factsjeljeljelejel arnettarnettNo ratings yet

- JM20337 JMicronDocument2 pagesJM20337 JMicronRuben Perez AyoNo ratings yet

- MakeIntern MOUDocument5 pagesMakeIntern MOUKush Jain100% (1)

- Friction in Textile FibersDocument13 pagesFriction in Textile FibersElkaid fadjroNo ratings yet

- HS FNT02 00000080aec - DDocument4 pagesHS FNT02 00000080aec - DMarcoNo ratings yet

- Cleft Lip & PalateDocument33 pagesCleft Lip & PalatedyahNo ratings yet

- English 10: Quarter 2 - Week 8Document86 pagesEnglish 10: Quarter 2 - Week 8Shania Erica GabuyaNo ratings yet

- Shiv TantraDocument12 pagesShiv TantrasubhashNo ratings yet

- Postpartum BluesDocument6 pagesPostpartum BluesmiL_kathrinaNo ratings yet

- In The Lap of The Master.Document31 pagesIn The Lap of The Master.prashantkhatana50% (2)

- Folding Paint Booth: Technology Workshop Craft Home Food Play Outside CostumesDocument8 pagesFolding Paint Booth: Technology Workshop Craft Home Food Play Outside Costumesleotostes2011No ratings yet

- What Hetman Do I NeedDocument2 pagesWhat Hetman Do I NeedCem GüngörNo ratings yet

- Open Mind Beginner Unit 2 Grammar and Vocabulary Test A - EditableDocument3 pagesOpen Mind Beginner Unit 2 Grammar and Vocabulary Test A - Editableandresalvarez.moriNo ratings yet

- Vibratory Sieve Shaker AS 200 Control: General InformationDocument11 pagesVibratory Sieve Shaker AS 200 Control: General InformationSupriyo PNo ratings yet

- Ch7 Port Hinterlands LogisticsDocument37 pagesCh7 Port Hinterlands LogisticsAswinanderst Twilight-Forever TbcKuadratNo ratings yet

- Accounting MCQsDocument12 pagesAccounting MCQsLaraib AliNo ratings yet

- Soas Dissertation Results DateDocument7 pagesSoas Dissertation Results DatePaperWritingServicesForCollegeStudentsOmaha100% (1)

- 13 GU15 EIC2 Technical Guidelines For Educational Institutes ComplianceDocument18 pages13 GU15 EIC2 Technical Guidelines For Educational Institutes Compliancezainlv95No ratings yet

- Practice Notes FOR Quantity Surveyors: TenderingDocument12 pagesPractice Notes FOR Quantity Surveyors: TenderingMok JSNo ratings yet

- The Japanese ModelDocument3 pagesThe Japanese ModelSiva Prasad PasupuletiNo ratings yet

- WCC Communication en-USDocument1,098 pagesWCC Communication en-USRiyas ANo ratings yet

- Fluids AssingnmenmtDocument36 pagesFluids AssingnmenmtReD DotaNo ratings yet

- Soil Fertility Plant Nutrition 2014Document21 pagesSoil Fertility Plant Nutrition 2014Juan Felipe MuñozNo ratings yet

- 1) Chévere: (This Word Is Also Seen in Colombian Slang)Document14 pages1) Chévere: (This Word Is Also Seen in Colombian Slang)Dano ClaveliNo ratings yet

- Operating Manual: AmplifierDocument12 pagesOperating Manual: AmplifiermigfrayaNo ratings yet

- Henry J. Werdann Margaret Werdann v. Bill & Jenny Enterprises, Incorporated, and Niles Austin William Jones, 995 F.2d 1065, 4th Cir. (1993)Document6 pagesHenry J. Werdann Margaret Werdann v. Bill & Jenny Enterprises, Incorporated, and Niles Austin William Jones, 995 F.2d 1065, 4th Cir. (1993)Scribd Government DocsNo ratings yet