You might also like

- IT Act Changes PDFDocument7 pagesIT Act Changes PDFSanjeev KumarNo ratings yet

- Pre Operative Expenses Meaning and TreatmentDocument2 pagesPre Operative Expenses Meaning and TreatmentAnindita HazraNo ratings yet

- Presentation - Employer Services062016 PDFDocument11 pagesPresentation - Employer Services062016 PDFABC 123No ratings yet

- Evaluation of The Impact of The CoVID-19 Pandemic On The Business of The CompanyDocument3 pagesEvaluation of The Impact of The CoVID-19 Pandemic On The Business of The CompanyNavnath BidgarNo ratings yet

- Deemed Interest IncomeDocument6 pagesDeemed Interest IncomeHaris HashimNo ratings yet

- No Question Proposed AnswerDocument3 pagesNo Question Proposed AnswerKianKianKianKianNo ratings yet

- No Question Proposed AnswerDocument3 pagesNo Question Proposed AnswerShahrizal IsmailNo ratings yet

- Sport NZ Template Financial Policies and Procedures: Section 5: Operating Expenditure & Payables Policy 1: PayrollDocument3 pagesSport NZ Template Financial Policies and Procedures: Section 5: Operating Expenditure & Payables Policy 1: PayrollShinil NambrathNo ratings yet

- Debt To Equity ConditionsDocument29 pagesDebt To Equity ConditionsEphraim TuganoNo ratings yet

- 25673cajournal Feb2012 13Document3 pages25673cajournal Feb2012 13Pravin DateNo ratings yet

- Application To ROC For Obtaining The Status of Dormant CompanyDocument11 pagesApplication To ROC For Obtaining The Status of Dormant CompanyLokiNo ratings yet

- FAQs on IFSCA (Payment Services) Regulations, 2024Document11 pagesFAQs on IFSCA (Payment Services) Regulations, 2024Hitesh MishraNo ratings yet

- Employer Services: Employees' PF OrganisationDocument11 pagesEmployer Services: Employees' PF OrganisationAnujit DebNo ratings yet

- FRS & FM of ERP PDFDocument405 pagesFRS & FM of ERP PDFDebasis BasaNo ratings yet

- Accounting Manual Employee Benefits Accounting Manual-Employee BenefitsDocument29 pagesAccounting Manual Employee Benefits Accounting Manual-Employee BenefitsRamkrishnarao BVNo ratings yet

- Primer: For Boi Registered CompaniesDocument13 pagesPrimer: For Boi Registered CompaniesSarah Jean TaliNo ratings yet

- CFAS Qualifying Exam ReviewerDocument20 pagesCFAS Qualifying Exam ReviewerCher Na100% (4)

- Singapore Law Related To Fund ManagementDocument3 pagesSingapore Law Related To Fund ManagementAnshul AgarwalNo ratings yet

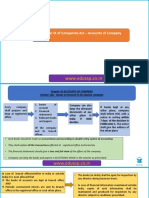

- WWW - Edutap.co - In: Chapter IX of Companies Act - Accounts of CompanyDocument15 pagesWWW - Edutap.co - In: Chapter IX of Companies Act - Accounts of Companyraahul dubeyNo ratings yet

- Particulars For Grant of Relaxation PDFDocument7 pagesParticulars For Grant of Relaxation PDFSanjeev KumarNo ratings yet

- Final Internal Audit Report 12-ICSIL-Ver-DraftDocument29 pagesFinal Internal Audit Report 12-ICSIL-Ver-DraftRamesh ChandraNo ratings yet

- Reporting On IFCDocument44 pagesReporting On IFCDharmendra SinghNo ratings yet

- Provident FundsDocument70 pagesProvident FundsSpeed HRNo ratings yet

- MCA Company Law Committee recommendations on Company AuditorsDocument2 pagesMCA Company Law Committee recommendations on Company AuditorsAvinash ShettyNo ratings yet

- IEPF Claim Instruction KitDocument10 pagesIEPF Claim Instruction KitAmit ZalaNo ratings yet

- Ministerial Resolution No 598 of 2022 Regarding The Wages Protection SystemDocument5 pagesMinisterial Resolution No 598 of 2022 Regarding The Wages Protection SystemAnees PmNo ratings yet

- Contractor MeetDocument26 pagesContractor MeetRaghav RaghavendraNo ratings yet

- Textual Learning Material - Module 3Document33 pagesTextual Learning Material - Module 3Jerry JohnNo ratings yet

- Comprehensive Financial Management System (CFMS) CFMS Circular - 8 Dt. 26.04.2018Document3 pagesComprehensive Financial Management System (CFMS) CFMS Circular - 8 Dt. 26.04.2018Samdhani StrikesNo ratings yet

- CA Inter Auditing RTP Nov22Document30 pagesCA Inter Auditing RTP Nov22tholkappiyanjk14No ratings yet

- Union Bank - 1581314273Document12 pagesUnion Bank - 1581314273Subrata PodderNo ratings yet

- AUDI314 Class Notes (September 10, 2021)Document2 pagesAUDI314 Class Notes (September 10, 2021)HatterlessNo ratings yet

- Project On Corporate ExistanceDocument13 pagesProject On Corporate ExistanceAnand ChoudharyNo ratings yet

- Audit Papers DecDocument164 pagesAudit Papers DecKeshav SethiNo ratings yet

- Corporate Governance and Clause 49 of The Listing AgreementDocument2 pagesCorporate Governance and Clause 49 of The Listing AgreementHeta MunjyasaraNo ratings yet

- 2022CC SEC Extension Offices Citizens Charter 2022 1st EditionDocument1,008 pages2022CC SEC Extension Offices Citizens Charter 2022 1st EditionGERALD DAANOYNo ratings yet

- Ch.5 Cashflow StatementDocument18 pagesCh.5 Cashflow StatementMalayaranjan PanigrahiNo ratings yet

- CDA guidelines for cooperative external auditor accreditationDocument11 pagesCDA guidelines for cooperative external auditor accreditationAndres Lorenzo III50% (2)

- Article PF Contributions On AllowancesDocument4 pagesArticle PF Contributions On Allowancestarlochan singhNo ratings yet

- Payment of Bonus Act, 1965Document28 pagesPayment of Bonus Act, 1965Apoorva JhaNo ratings yet

- SEZ fiscal incentives for developers, units in IndiaDocument4 pagesSEZ fiscal incentives for developers, units in IndiaRavirajSoniNo ratings yet

- Weekly UpdateDocument4 pagesWeekly UpdateKoko FerminNo ratings yet

- ICFR A Handbook For PVT Cos and Their AuditorsDocument97 pagesICFR A Handbook For PVT Cos and Their AuditorszeerakzahidNo ratings yet

- Misc. Information Regarding Provident Fund ImpDocument3 pagesMisc. Information Regarding Provident Fund Impajit25singhNo ratings yet

- Paper - 3: Advanced Auditing and Professional Ethics: (5 Marks)Document16 pagesPaper - 3: Advanced Auditing and Professional Ethics: (5 Marks)RashmiNo ratings yet

- EPF Organisation EO/AO GuideDocument189 pagesEPF Organisation EO/AO GuideRamesh Chidambaram88% (17)

- Missive Volume IV - July 2011: Transaction AdvisorsDocument11 pagesMissive Volume IV - July 2011: Transaction AdvisorsAkhil BansalNo ratings yet

- C P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaDocument54 pagesC P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaPradyoth C JohnNo ratings yet

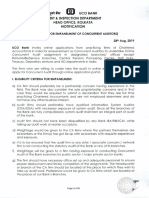

- UCO BANK Audit and InspectionDocument16 pagesUCO BANK Audit and Inspectionganpati megabuilderNo ratings yet

- Geeta Saar 99 Internal AuditDocument4 pagesGeeta Saar 99 Internal Auditcharanjeet singh chawlaNo ratings yet

- Statistics Directorate: National AccountsDocument7 pagesStatistics Directorate: National AccountsyellowNo ratings yet

- Sarbanes Oxley Vs PH LegislationsDocument5 pagesSarbanes Oxley Vs PH LegislationsJNo ratings yet

- ESOP Under FEMA RegulationDocument8 pagesESOP Under FEMA RegulationDeeksha NCNo ratings yet

- cf6a6742-0bd0-41de-8229-b707fbb139ccDocument5 pagescf6a6742-0bd0-41de-8229-b707fbb139ccSumitNo ratings yet

- Paper - 3: Advanced Auditing and Professional Ethics: (5 Marks)Document18 pagesPaper - 3: Advanced Auditing and Professional Ethics: (5 Marks)Suryanarayan RajanalaNo ratings yet

- AGNPO Midterms ReviewerDocument79 pagesAGNPO Midterms ReviewerKurt Morin Cantor100% (2)

- Instructions For Form 990: Internal Revenue ServiceDocument24 pagesInstructions For Form 990: Internal Revenue ServiceIRSNo ratings yet

- Instruction Kit For Eform Adt - 2: Page 1 of 8Document8 pagesInstruction Kit For Eform Adt - 2: Page 1 of 8maddy14350No ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- 2012-05-31 - Russian Mobile Market Trends PDFDocument5 pages2012-05-31 - Russian Mobile Market Trends PDFVvb SatyanarayanaNo ratings yet

- Harmonics 3Document5 pagesHarmonics 3Vvb SatyanarayanaNo ratings yet

- S&P Finance Company RatiosDocument5 pagesS&P Finance Company RatiosVvb SatyanarayanaNo ratings yet

- FM Ebook EmailDocument13 pagesFM Ebook EmailVvb SatyanarayanaNo ratings yet

- Private Excel Modelling TestDocument40 pagesPrivate Excel Modelling TestVvb SatyanarayanaNo ratings yet

- Nestle: Estimated Reach ExposureDocument8 pagesNestle: Estimated Reach ExposureVvb SatyanarayanaNo ratings yet

- Upwork FinancialDocument19 pagesUpwork FinancialVvb SatyanarayanaNo ratings yet

- T-Shirt Distribution List - CouncilDocument20 pagesT-Shirt Distribution List - CouncilVvb SatyanarayanaNo ratings yet

- Harmonics 1Document33 pagesHarmonics 1Vvb SatyanarayanaNo ratings yet

- Summary Curr Q32010 SupplyDocument4 pagesSummary Curr Q32010 SupplyVvb SatyanarayanaNo ratings yet

- Gi BSDocument8 pagesGi BSVvb SatyanarayanaNo ratings yet

- SOUL Interest Form 2016 - 18Document3 pagesSOUL Interest Form 2016 - 18Vvb SatyanarayanaNo ratings yet

- Radio OneDocument7 pagesRadio OneVvb Satyanarayana0% (1)

- Work CostDocument2 pagesWork CostVvb SatyanarayanaNo ratings yet

- Ratio AnalysisDocument5 pagesRatio AnalysisPiyush AroraNo ratings yet

- Valuation Cash Flow A Teaching NoteDocument5 pagesValuation Cash Flow A Teaching NoteVvb SatyanarayanaNo ratings yet

- YES BANK SIM-SLEEVE CASE STUDYDocument5 pagesYES BANK SIM-SLEEVE CASE STUDYVvb SatyanarayanaNo ratings yet

- J 2Document8 pagesJ 2Vvb SatyanarayanaNo ratings yet

- VitaDocument20 pagesVitaVvb SatyanarayanaNo ratings yet

- J 1Document3 pagesJ 1Vvb SatyanarayanaNo ratings yet

- Raw DataDocument48 pagesRaw DataVvb SatyanarayanaNo ratings yet

- Zeus Asset Management Inc. - Team 1 - Investment ManagementDocument4 pagesZeus Asset Management Inc. - Team 1 - Investment ManagementVvb SatyanarayanaNo ratings yet

- Upwork FinancialDocument19 pagesUpwork FinancialVvb SatyanarayanaNo ratings yet

- Upwork FinancialDocument19 pagesUpwork FinancialVvb SatyanarayanaNo ratings yet

- Risk Management Related Development Work: I. KEY ResponsibilitiesDocument2 pagesRisk Management Related Development Work: I. KEY ResponsibilitiesVvb SatyanarayanaNo ratings yet

- Selecting Things DemoDocument2 pagesSelecting Things DemoVvb SatyanarayanaNo ratings yet

- Strategy Indigo Report Group 7Document26 pagesStrategy Indigo Report Group 7Vvb SatyanarayanaNo ratings yet

- Fall 2016 First Capital Budgeting AssignmentDocument2 pagesFall 2016 First Capital Budgeting AssignmentVvb SatyanarayanaNo ratings yet

- IIM Ranchi - V V B Satyanarayana - FinanceDocument1 pageIIM Ranchi - V V B Satyanarayana - FinanceVvb SatyanarayanaNo ratings yet

- Khoadd - Uog1@st - Uel.edu - Vn-Diep Dang Khoa-BM5104-UoG0112-Assessment 2Document11 pagesKhoadd - Uog1@st - Uel.edu - Vn-Diep Dang Khoa-BM5104-UoG0112-Assessment 2Khoa Diệp Đăng100% (1)

- The Importance of Legal EnglishDocument1 pageThe Importance of Legal EnglishJas TacioNo ratings yet

- Case Study - Bombay Plywood Industry RawalpindiDocument11 pagesCase Study - Bombay Plywood Industry Rawalpindimyfams100% (2)

- The Difference Between Lineage and TraceabilityDocument7 pagesThe Difference Between Lineage and TraceabilitysalimmanzurNo ratings yet

- Economics Test 1Document4 pagesEconomics Test 1khurramsultanNo ratings yet

- SwiftDocument2 pagesSwiftpcchhabraNo ratings yet

- P2 - Performance ManagementDocument11 pagesP2 - Performance Managementmrshami7754No ratings yet

- FabIndia's Expansion Plans in the UK MarketDocument13 pagesFabIndia's Expansion Plans in the UK MarketSagar Deshmukh100% (1)

- Case Study Sprint 2598Document6 pagesCase Study Sprint 2598आकाश स्व.No ratings yet

- Direct Cool Fridge RatingsDocument28 pagesDirect Cool Fridge RatingskjfensNo ratings yet

- Transfer relocation claim stepsDocument3 pagesTransfer relocation claim stepschandraNo ratings yet

- Customer Perceptions of Service: Mcgraw-Hill/IrwinDocument27 pagesCustomer Perceptions of Service: Mcgraw-Hill/IrwinKoshiha LalNo ratings yet

- CMDBuild WorkflowManual ENG V240 PDFDocument70 pagesCMDBuild WorkflowManual ENG V240 PDFPaco De Peco EdmspjpNo ratings yet

- Clan CultureDocument3 pagesClan CulturemichaelNo ratings yet

- Totally Integrated AutomationDocument8 pagesTotally Integrated AutomationShamim Ahsan ParvezNo ratings yet

- IandE - Session 4 - Entrepreneurship - Deve Cycle and Brand Quiz - 7 FebDocument46 pagesIandE - Session 4 - Entrepreneurship - Deve Cycle and Brand Quiz - 7 Feblabolab344No ratings yet

- 07 X07 A ResponsibilityDocument12 pages07 X07 A ResponsibilityJohnMarkVincentGiananNo ratings yet

- Analisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemDocument7 pagesAnalisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemJasika Jurnal Sistem Informasi AkuntansiNo ratings yet

- Introduction of Partnership AccountsDocument12 pagesIntroduction of Partnership Accountsdeepika jainNo ratings yet

- Accountant interview questions to assess experience and skillsDocument1 pageAccountant interview questions to assess experience and skillsevaNo ratings yet

- Introduction to Experiential ExercisesDocument8 pagesIntroduction to Experiential ExercisesAntokaNo ratings yet

- Cir vs. TMX Sales and CtaDocument3 pagesCir vs. TMX Sales and CtaD De LeonNo ratings yet

- OAUX Wireframe Template Release 10 RDK V2Document32 pagesOAUX Wireframe Template Release 10 RDK V2dvartaNo ratings yet

- PS Full Cycle ImplementationDocument3 pagesPS Full Cycle Implementationsarada_jituNo ratings yet

- Fabian Valado n9875026 Case Analysis - Bang Bang HairDocument11 pagesFabian Valado n9875026 Case Analysis - Bang Bang HairAnonymous KpiSiVl4uXNo ratings yet

- Corporate Governance Elements ExplainedDocument24 pagesCorporate Governance Elements ExplainedNana AbaNo ratings yet

- Private and Public Banks DatabaseDocument37 pagesPrivate and Public Banks DatabasesagartikaitNo ratings yet

- What Is Strategic ManagementDocument10 pagesWhat Is Strategic ManagementREILENE ALAGASINo ratings yet

- Agenda: Majid Al Futtaim Properties ©Document36 pagesAgenda: Majid Al Futtaim Properties ©rtagarraNo ratings yet