You might also like

- Brokerage Business PlanDocument19 pagesBrokerage Business PlanMuhammad Ahmed50% (4)

- Project ReportDocument23 pagesProject ReportAkshay GonewarNo ratings yet

- Sample SAP FI BlueprintDocument80 pagesSample SAP FI BlueprintYinka FaluaNo ratings yet

- Pro Forma Financial Statements 2014 2015 2016 Income StatementDocument4 pagesPro Forma Financial Statements 2014 2015 2016 Income Statementpriyanka khobragadeNo ratings yet

- NPS BookletDocument12 pagesNPS BookletBhuvanNo ratings yet

- NPS LeafletDocument2 pagesNPS LeafletMOHIT GUPTA jiNo ratings yet

- The New Pension System - (NPS) - (NPS)Document17 pagesThe New Pension System - (NPS) - (NPS)Adv.Trupti Bhamare PingaleNo ratings yet

- Brochure HDFC NPSDocument2 pagesBrochure HDFC NPSkonupoddarNo ratings yet

- Nps One PagerDocument2 pagesNps One PagerldorayaNo ratings yet

- What Is National Pension Scheme?: Exit Before RetirementDocument9 pagesWhat Is National Pension Scheme?: Exit Before Retirementparidhi guptaNo ratings yet

- Week 6.pptx - WatermarkDocument69 pagesWeek 6.pptx - Watermarkkhushi jaiswalNo ratings yet

- SAP CRA Approved (1.0) POPDocument25 pagesSAP CRA Approved (1.0) POPJoe BenzNo ratings yet

- National Pension System (NPS)Document4 pagesNational Pension System (NPS)Anupam AwasthiNo ratings yet

- FAQ On NPSDocument7 pagesFAQ On NPSRaddyNo ratings yet

- Prs Booklet WebDocument12 pagesPrs Booklet WebNur Khairunnisa Malik100% (1)

- NpsDocument48 pagesNpsEcademyNo ratings yet

- Cra Subscriber BrochureDocument12 pagesCra Subscriber Brochureramankant_pauNo ratings yet

- National Pension System (NPS) : (E, C and G)Document5 pagesNational Pension System (NPS) : (E, C and G)Shiva SinghNo ratings yet

- FAQ's: Who Are Central Record Keeping Agency?Document27 pagesFAQ's: Who Are Central Record Keeping Agency?Sampada mowadeNo ratings yet

- Redefining GovernanceDocument16 pagesRedefining Governancerajamanickam511925No ratings yet

- WMPFP - Retirement and Estate PlanningDocument34 pagesWMPFP - Retirement and Estate PlanningNANDINI GUPTANo ratings yet

- Security Analysis and Portfolio Management: - Prof. Samidha AngneDocument44 pagesSecurity Analysis and Portfolio Management: - Prof. Samidha AngneSudhir Kumar AgarwalNo ratings yet

- All About New Pension SchemeDocument2 pagesAll About New Pension SchemedhirennagareyaNo ratings yet

- Entities Involved in The New Pension SystemDocument4 pagesEntities Involved in The New Pension Systemmmmppp1No ratings yet

- Icici Brochure - PENSION PLAN ULIPDocument10 pagesIcici Brochure - PENSION PLAN ULIPAbhishek PrabhakarNo ratings yet

- National Pension SystemDocument3 pagesNational Pension SystemRamesh KumarNo ratings yet

- Income Tax Saving - 5 Investment Options Offering Fixed Interest Rate Without Stock Market VolatilityDocument2 pagesIncome Tax Saving - 5 Investment Options Offering Fixed Interest Rate Without Stock Market VolatilityNikhil SharmaNo ratings yet

- Nps For Nris: Eligibility Source of Contributions in NpsDocument12 pagesNps For Nris: Eligibility Source of Contributions in NpsMohammed Shoukat AliNo ratings yet

- NPS National Pension SystemDocument7 pagesNPS National Pension SystemHari BhaskarNo ratings yet

- National Pension Scheme (NPS) Guidelines FY 2019-20Document21 pagesNational Pension Scheme (NPS) Guidelines FY 2019-20harrishNo ratings yet

- National Pension System FAQs GeneralDocument8 pagesNational Pension System FAQs GeneralvrknraoNo ratings yet

- Frequently Asked Questions (Faq) : Under National Pension System (NPS)Document11 pagesFrequently Asked Questions (Faq) : Under National Pension System (NPS)Satish KumarNo ratings yet

- PruBSN Platinum Brochure EngDocument10 pagesPruBSN Platinum Brochure EngfaizahNo ratings yet

- The New National Pension SchemeDocument2 pagesThe New National Pension Schemegurudev001No ratings yet

- FAQs On NPS (UOS)Document27 pagesFAQs On NPS (UOS)abhinavNo ratings yet

- Public Mutual Private Retiremenent Scheme ProducthighlightDocument12 pagesPublic Mutual Private Retiremenent Scheme ProducthighlightBenNo ratings yet

- Pension Markets and Products in IndiaDocument26 pagesPension Markets and Products in IndiaSiddhartha JainNo ratings yet

- NPS PPT - HDFC BankDocument17 pagesNPS PPT - HDFC BankPankaj Kothari100% (1)

- Nps Note and MCQDocument37 pagesNps Note and MCQRSMENNo ratings yet

- Service Rules MCQDocument56 pagesService Rules MCQArshad100% (4)

- National Pension System - Retirement Plan For All - National Portal of IndiaDocument7 pagesNational Pension System - Retirement Plan For All - National Portal of IndiaLalrohlui RalteNo ratings yet

- Smile More! Smile More!: Higher Than The Highest NAV GUARANTEEDDocument12 pagesSmile More! Smile More!: Higher Than The Highest NAV GUARANTEEDspcalNo ratings yet

- FAQ On NPSDocument7 pagesFAQ On NPSsecunsharmaNo ratings yet

- Faq National Pension SystemDocument5 pagesFaq National Pension Systemjageshwar dewanganNo ratings yet

- Harsh Jain PTPDocument12 pagesHarsh Jain PTPJatin JainNo ratings yet

- Jeevan PlansDocument18 pagesJeevan PlansGangadhar CHNo ratings yet

- National Pension SchemeDocument24 pagesNational Pension SchemenicesreekanthNo ratings yet

- ING Prospering Life BrochureDocument8 pagesING Prospering Life BrochureJoin RiotNo ratings yet

- SIP Insure PresentationDocument20 pagesSIP Insure PresentationbghanshyamNo ratings yet

- Handy Financial Tips Ebook EnglishDocument24 pagesHandy Financial Tips Ebook EnglishJPNo ratings yet

- Retirement Planning With Group SuperannuationDocument5 pagesRetirement Planning With Group SuperannuationRutul DaveNo ratings yet

- New Welcome Kit 396945283Document14 pagesNew Welcome Kit 396945283Belur BaxiNo ratings yet

- Vibhu Verma PTP Project Section 80cDocument12 pagesVibhu Verma PTP Project Section 80cJatin JainNo ratings yet

- National Pension Scheme - Process Note - v1Document11 pagesNational Pension Scheme - Process Note - v1Pratap ReddyNo ratings yet

- FAQs On NPS - HDFC - v3Document16 pagesFAQs On NPS - HDFC - v3Pratap ReddyNo ratings yet

- Facts - National Pension SchemeDocument2 pagesFacts - National Pension SchemechaitanyaNo ratings yet

- Facts - National Pension Scheme (NPS)Document2 pagesFacts - National Pension Scheme (NPS)siddharth gautamNo ratings yet

- Facts - National Pension Scheme (NPS)Document2 pagesFacts - National Pension Scheme (NPS)rupeshNo ratings yet

- MKT Plus GRK (Compatibility Mode)Document32 pagesMKT Plus GRK (Compatibility Mode)PARAGNNo ratings yet

- Chapter 3 RoughDocument8 pagesChapter 3 Roughchandrujayaraman1205No ratings yet

- Annexure New Pension SchemeDocument3 pagesAnnexure New Pension SchemeAbhilasha MathurNo ratings yet

- Press Release - Increase of Joining Age Under Nps-Private Sector From 60 To 65 YearsDocument1 pagePress Release - Increase of Joining Age Under Nps-Private Sector From 60 To 65 YearsAnkur SrivastavaNo ratings yet

- Do-It-Yourself Financial Plans: VeriPlan User Guide - 2023From EverandDo-It-Yourself Financial Plans: VeriPlan User Guide - 2023No ratings yet

- New Doc 2018-02-03 PDFDocument1 pageNew Doc 2018-02-03 PDFNikhil MendheNo ratings yet

- Request LetterDocument1 pageRequest LetterNikhil MendheNo ratings yet

- Plot No Netarea (SQ FT) Category Totalarea (SQ MTR) Tanarea (SQ MTR) Netarea (SQ MTR) StatusDocument10 pagesPlot No Netarea (SQ FT) Category Totalarea (SQ MTR) Tanarea (SQ MTR) Netarea (SQ MTR) StatusNikhil MendheNo ratings yet

- Nitesh ChudasamaDocument2 pagesNitesh ChudasamaNikhil MendheNo ratings yet

- Team PRTC 1stPB May 2024 - AFARDocument7 pagesTeam PRTC 1stPB May 2024 - AFARAnne Marie SositoNo ratings yet

- Zee Learn Analyst PresentationDocument58 pagesZee Learn Analyst PresentationAsha PrabhacarNo ratings yet

- Read Writ U6 ComercioDocument3 pagesRead Writ U6 ComercioRosaFuentes100% (1)

- Horizontal Analaysis GLOBEDocument2 pagesHorizontal Analaysis GLOBEjerameelnacalaban1No ratings yet

- Acc 252 Practice ExamDocument5 pagesAcc 252 Practice ExamEmy ManiyarNo ratings yet

- GpaDocument8 pagesGpaarunzexyNo ratings yet

- Financial Analysis of Bata BangladeshDocument20 pagesFinancial Analysis of Bata BangladeshSajeed Mahmud MaheeNo ratings yet

- Ijasmp Even WatermarkDocument164 pagesIjasmp Even WatermarkKota Mani KantaNo ratings yet

- Taxation Law: Questions and Suggested AnswersDocument142 pagesTaxation Law: Questions and Suggested AnswersDianne MedianeroNo ratings yet

- Case List - Remedies Under The NIRCDocument29 pagesCase List - Remedies Under The NIRCdonsiccuan100% (1)

- 2012 HKDSE Econ Mock Exam Paper 1 - Set 1Document18 pages2012 HKDSE Econ Mock Exam Paper 1 - Set 1黃俊安No ratings yet

- Accenture Fast Forward To Growth v2Document72 pagesAccenture Fast Forward To Growth v2Arkajyoti JanaNo ratings yet

- Fin3n Cap Budgeting Quiz 1Document1 pageFin3n Cap Budgeting Quiz 1Kirsten Marie EximNo ratings yet

- 395 Midterm 1 Cheat SheetDocument2 pages395 Midterm 1 Cheat Sheetchrisjames20036No ratings yet

- Latihan Alk Gayuh Nata Imahdi Al AfghaniDocument14 pagesLatihan Alk Gayuh Nata Imahdi Al AfghaniYoga Arif PratamaNo ratings yet

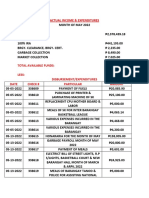

- Actual Income & ExpendituresDocument5 pagesActual Income & Expendituressan nicolas 2nd betis guagua pampangaNo ratings yet

- Kalbe Farma TBK 31 Des 2020Document173 pagesKalbe Farma TBK 31 Des 2020A. A Gede Wimanta Wari Bawantu32 DarmaNo ratings yet

- 1st Prelim Reviewer in FinanceDocument7 pages1st Prelim Reviewer in FinancemarieNo ratings yet

- UBS Business Plan - Stategic Planning and Financing Basis - Model For Generating A Business Plan - (UBS AG) PDFDocument26 pagesUBS Business Plan - Stategic Planning and Financing Basis - Model For Generating A Business Plan - (UBS AG) PDFQuantDev-MNo ratings yet

- Chapter 6Document14 pagesChapter 6Louie Ann CasabarNo ratings yet

- Kakao: March 2016 Investor RelationsDocument15 pagesKakao: March 2016 Investor RelationsMila BaquerizoNo ratings yet

- Assignment Drive SPRING 2017 Program MBA Semester I Ssubject Code & Name MBA104 Financial and Management Accounting BK Id B1624 Credit 4 Marks 60Document3 pagesAssignment Drive SPRING 2017 Program MBA Semester I Ssubject Code & Name MBA104 Financial and Management Accounting BK Id B1624 Credit 4 Marks 60rakeshNo ratings yet

- Chevron Philippines, Inc. vs. Bases Conversion Development Authority and Clark Development Corporation, G.R. No. 173863, September 15, 2010Document1 pageChevron Philippines, Inc. vs. Bases Conversion Development Authority and Clark Development Corporation, G.R. No. 173863, September 15, 2010Jeselle Ann VegaNo ratings yet

- High CountryDocument2 pagesHigh CountryHenny DeWillisNo ratings yet

- Modern Marketing Center of Excellence Best Practices GuideDocument22 pagesModern Marketing Center of Excellence Best Practices GuideDemand MetricNo ratings yet

- Problem Set - III The Value of Common StocksDocument2 pagesProblem Set - III The Value of Common StocksVlipperNo ratings yet

- Formula Sheet Corporate Finance (COF) : Stockholm Business SchoolDocument6 pagesFormula Sheet Corporate Finance (COF) : Stockholm Business SchoolLinus AhlgrenNo ratings yet