You might also like

- NRI Banking FinalDocument60 pagesNRI Banking Finalहर्ष मोहन100% (6)

- Summer Internship Report at Future Generali Insurance LTDDocument44 pagesSummer Internship Report at Future Generali Insurance LTDpratiksha2467% (3)

- Project On LIC IndiaDocument73 pagesProject On LIC IndiaViPul86% (73)

- Assignment Liquidation Lump SumDocument10 pagesAssignment Liquidation Lump SumCresenciano Malabuyoc100% (1)

- Study in ICICI LombardDocument64 pagesStudy in ICICI LombardDebabrato SasmalNo ratings yet

- SBI Life InsuranceDocument73 pagesSBI Life Insuranceiloveyoujaan50% (6)

- ICICI Lombard Project ReportDocument91 pagesICICI Lombard Project ReportMahesh Parab75% (4)

- A Project Report On Kotak InsuranceDocument82 pagesA Project Report On Kotak Insurancevarun_bawa251915No ratings yet

- Project Report On Kotak Life InsuranceDocument62 pagesProject Report On Kotak Life InsuranceMrvikas78% (9)

- Student Transcript Corporate Finance Institute®: Student No.: Student Name: Date of BirthDocument9 pagesStudent Transcript Corporate Finance Institute®: Student No.: Student Name: Date of BirthHarshit100% (2)

- Project SBIDocument70 pagesProject SBIanshushah_144850168No ratings yet

- Star Company ReportDocument67 pagesStar Company ReportParvat PatilNo ratings yet

- Indian Insurance Industry AnalysisDocument90 pagesIndian Insurance Industry Analysismansidube138680% (10)

- Marketing of Insurance in ICICI Prudential Life InsuranceDocument89 pagesMarketing of Insurance in ICICI Prudential Life InsuranceksumitkapoorNo ratings yet

- A Study On Sbi Life InsuranceDocument40 pagesA Study On Sbi Life InsuranceprabhuNo ratings yet

- SBI Life InsuranceDocument38 pagesSBI Life InsuranceParth Bhatt50% (2)

- A Project ON: "Comprative Study of General Insurance Company Oriential Insurance With New India Assurance Company India"Document73 pagesA Project ON: "Comprative Study of General Insurance Company Oriential Insurance With New India Assurance Company India"Rohit MalviyaNo ratings yet

- Role of LIC in Indian InsuranceDocument61 pagesRole of LIC in Indian Insurancenikita950100% (2)

- A Project Report On Organization Study and Awareness of ICICI Prudential Life Insurance Co. LTDDocument78 pagesA Project Report On Organization Study and Awareness of ICICI Prudential Life Insurance Co. LTDBabasab Patil (Karrisatte)No ratings yet

- A Comparative Study of Public Private Life Insurance Companies in IndiaDocument5 pagesA Comparative Study of Public Private Life Insurance Companies in IndiaAkansha GoyalNo ratings yet

- A Project Report On ICICI Prudential Life InsuranceDocument37 pagesA Project Report On ICICI Prudential Life InsuranceSudha Sandesh Ambekar86% (42)

- LIC Project FinalDocument50 pagesLIC Project Finalprayaas67% (3)

- Bajaj AllianzDocument57 pagesBajaj AllianzDIpesh Joshi93% (30)

- Project Report SmuDocument76 pagesProject Report SmuChandan Srivastava100% (1)

- Insurance Sector of IndiaDocument66 pagesInsurance Sector of IndiaVijay94% (36)

- A Project Report ON: Royal Sundaram Insurance CompanyDocument12 pagesA Project Report ON: Royal Sundaram Insurance CompanyKritika PrasadNo ratings yet

- A Project Report: Consumer Behavior Towards Birla Sunlife Insurance LTDDocument65 pagesA Project Report: Consumer Behavior Towards Birla Sunlife Insurance LTDakhilNo ratings yet

- Project On Icici Lombard General InsuranceDocument69 pagesProject On Icici Lombard General InsuranceParikshit Ramjiyani100% (3)

- Project Report On Icici Lombard General Insurance LTDDocument72 pagesProject Report On Icici Lombard General Insurance LTDjay0% (2)

- Insurance Industry in IndiaDocument43 pagesInsurance Industry in IndiaManojNo ratings yet

- A Project Report On Insurance As An Investment Tool With Regards To ULIP at ICICI LTDDocument96 pagesA Project Report On Insurance As An Investment Tool With Regards To ULIP at ICICI LTDBabasab Patil (Karrisatte)50% (2)

- Project On Icici Prudential Life Insurance Company Limited.Document80 pagesProject On Icici Prudential Life Insurance Company Limited.Komal Yadav75% (8)

- A Project Study Report On Training Undertaken At: Deepshikha College of Technical Education, JaipurDocument78 pagesA Project Study Report On Training Undertaken At: Deepshikha College of Technical Education, JaipurLaxmikant Sharma100% (2)

- HDFC Standard Life Insurance ProjectDocument58 pagesHDFC Standard Life Insurance Projectj_y_o_t_i80% (10)

- Role of Insurance Industry in Economic Growth of India0Document70 pagesRole of Insurance Industry in Economic Growth of India0Omkar pawar50% (2)

- New India Assurance CoDocument59 pagesNew India Assurance CoAnandi KonarNo ratings yet

- Comparative Study of Ulip Plans Offered by Icici Prudential and Other Life Insurance Companies 11031 140405024137 Phpapp01 PDFDocument78 pagesComparative Study of Ulip Plans Offered by Icici Prudential and Other Life Insurance Companies 11031 140405024137 Phpapp01 PDFRenowntechnologies VisakhapatnamNo ratings yet

- ING Vysya Life Insurance Training & Development ReportDocument46 pagesING Vysya Life Insurance Training & Development ReportSurendra ShuklaNo ratings yet

- Privatization of Insurance Industry in IndiaDocument78 pagesPrivatization of Insurance Industry in IndiaAnkush Anam0% (1)

- In Partial Fulfillment For The Award of The Degree Of: Under Corporate Guide Submitted By: Vivek KumarDocument44 pagesIn Partial Fulfillment For The Award of The Degree Of: Under Corporate Guide Submitted By: Vivek Kumarhoney biswarajNo ratings yet

- Heading Functional ProjectDocument6 pagesHeading Functional ProjectTusharJoshiNo ratings yet

- A Summer Placement Report On HDFC Standard Life Insurance Company LimitedDocument79 pagesA Summer Placement Report On HDFC Standard Life Insurance Company LimitedRisha RainaNo ratings yet

- A Comparative Study On The Offerings of Insurance Products Between LICDocument26 pagesA Comparative Study On The Offerings of Insurance Products Between LICk b paliwal91% (22)

- Sanika Shinde Roll No 7840Document101 pagesSanika Shinde Roll No 7840prasaddk39No ratings yet

- Project ReportDocument77 pagesProject ReportJatin DuaNo ratings yet

- Icici PrudentialDocument141 pagesIcici PrudentialBura NareshNo ratings yet

- A Study on Online Trading DerivativesDocument44 pagesA Study on Online Trading DerivativesTusharJoshiNo ratings yet

- Project Report: Submitted For The Partial Fulfillment of The Requirement For TheDocument87 pagesProject Report: Submitted For The Partial Fulfillment of The Requirement For Themr.avdheshsharmaNo ratings yet

- Project Report Consumer Behaviour (Icici Pru)Document90 pagesProject Report Consumer Behaviour (Icici Pru)balaji bysani67% (6)

- Understanding Marketing & Selling Process at Icici Prudential Life Insurance.Document8 pagesUnderstanding Marketing & Selling Process at Icici Prudential Life Insurance.ganesh balu bhoirNo ratings yet

- SIP ProjectDocument29 pagesSIP ProjectAnuradha PatelNo ratings yet

- Ulips Kamlesh Prajapati MBA Grand ProjectDocument76 pagesUlips Kamlesh Prajapati MBA Grand ProjectKrishna PrajapatiNo ratings yet

- Vdocument - in - Sip Report 55d6c4d76d5a1Document81 pagesVdocument - in - Sip Report 55d6c4d76d5a1Monnu montoNo ratings yet

- Consumer perception study of SBI Life's claim settlement processDocument39 pagesConsumer perception study of SBI Life's claim settlement processSaroj KhadangaNo ratings yet

- Ruchi File2Document63 pagesRuchi File2BOT XNo ratings yet

- Sanika Shinde Roll No 7840Document103 pagesSanika Shinde Roll No 7840prasaddk39No ratings yet

- Mukesh Kumar 1815270069Document69 pagesMukesh Kumar 1815270069Abhishek SharmaNo ratings yet

- My Project Report On ICICI PruDocument90 pagesMy Project Report On ICICI PruNabinSundar Nayak100% (2)

- Anil Project IDFCDocument77 pagesAnil Project IDFCAnil Kumar GudigantiNo ratings yet

- Gaurav - Marketing HDFC SLIC ProjectDocument94 pagesGaurav - Marketing HDFC SLIC ProjectSanjeev KumarNo ratings yet

- A Project On "Customer Acquisition For Aditya Birla Sun Life Insurance Company, Pune."Document48 pagesA Project On "Customer Acquisition For Aditya Birla Sun Life Insurance Company, Pune."Shashank Rangari100% (1)

- Effectiveness of Advertisement On Insurance CompanyDocument78 pagesEffectiveness of Advertisement On Insurance Companysumit lakraNo ratings yet

- Project Report On: "Problem and Prospects of Insurances Agencies "Document79 pagesProject Report On: "Problem and Prospects of Insurances Agencies "narpalchauhanNo ratings yet

- Minor Project Report On "NRI Banking"Document5 pagesMinor Project Report On "NRI Banking"हर्ष मोहनNo ratings yet

- Monetization Explained: Neither Game Changer nor CatastropheDocument4 pagesMonetization Explained: Neither Game Changer nor CatastropheKaran NainNo ratings yet

- Name: Roll No.: Microeconomics Quiz 2Document1 pageName: Roll No.: Microeconomics Quiz 2हर्ष मोहनNo ratings yet

- Akh (O Og8 One: Ar) AdenhemendtDocument8 pagesAkh (O Og8 One: Ar) Adenhemendtहर्ष मोहनNo ratings yet

- Performance of Scheduled Commercial Banks in India and Mandya District: Recent TrendsDocument9 pagesPerformance of Scheduled Commercial Banks in India and Mandya District: Recent TrendsIOSRjournalNo ratings yet

- C S: Icici Lombard: ASE Tudy ONDocument13 pagesC S: Icici Lombard: ASE Tudy ONहर्ष मोहनNo ratings yet

- Brand AwarenessDocument41 pagesBrand Awarenessहर्ष मोहनNo ratings yet

- Summer internship certificate for insurance marketingDocument1 pageSummer internship certificate for insurance marketingहर्ष मोहनNo ratings yet

- Pdcs 2 2017 Question PaperDocument2 pagesPdcs 2 2017 Question Paperहर्ष मोहनNo ratings yet

- BankDocument13 pagesBankहर्ष मोहनNo ratings yet

- Project On ICICI BankDocument78 pagesProject On ICICI BankViPul90% (41)

- Pdcs 2 2017 Question PaperDocument2 pagesPdcs 2 2017 Question Paperहर्ष मोहनNo ratings yet

- Pdcs 2 2017 Question PaperDocument2 pagesPdcs 2 2017 Question Paperहर्ष मोहनNo ratings yet

- Project On ICICI BankDocument78 pagesProject On ICICI BankViPul90% (41)

- Ip Bba 4th 2011 Ibei (B&i)Document1 pageIp Bba 4th 2011 Ibei (B&i)हर्ष मोहनNo ratings yet

- NRI Banking2Document60 pagesNRI Banking2हर्ष मोहनNo ratings yet

- NRI BankingDocument62 pagesNRI Bankingहर्ष मोहन100% (1)

- Project Report ON "Financial Analysis" OF: IciciDocument102 pagesProject Report ON "Financial Analysis" OF: Iciciहर्ष मोहनNo ratings yet

- Ip Bba 4th 2012 Ibei (B&i)Document1 pageIp Bba 4th 2012 Ibei (B&i)हर्ष मोहनNo ratings yet

- IP BBA 4th 2013 Business Environment PDFDocument1 pageIP BBA 4th 2013 Business Environment PDFहर्ष मोहनNo ratings yet

- On Risk Management in BanksDocument7 pagesOn Risk Management in Banksहर्ष मोहन100% (1)

- IP BBA 4th 2013 Business EnvironmentDocument1 pageIP BBA 4th 2013 Business Environmentहर्ष मोहनNo ratings yet

- NRI Banking Report SummaryDocument77 pagesNRI Banking Report Summaryहर्ष मोहनNo ratings yet

- Various Committees On Corporate GovernanceDocument11 pagesVarious Committees On Corporate GovernanceFouzia imzNo ratings yet

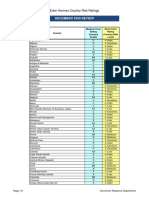

- December 2020 Review: Euler Hermes Country Risk RatingsDocument5 pagesDecember 2020 Review: Euler Hermes Country Risk RatingsLFNo ratings yet

- Test Bank For Auditing A Practical Approach With Data Analytics 1st Edition Raymond N Johnson Laura Davis Wiley Robyn Moroney Fiona Campbell Jane HamiltonDocument11 pagesTest Bank For Auditing A Practical Approach With Data Analytics 1st Edition Raymond N Johnson Laura Davis Wiley Robyn Moroney Fiona Campbell Jane Hamiltonironerpaijama.pe2ddu100% (44)

- Errors Omissions InsuranceDocument1 pageErrors Omissions InsuranceMilan PasulaNo ratings yet

- Ch3 Acct2105 UpDocument59 pagesCh3 Acct2105 Upgor jamNo ratings yet

- Accounting Principles and PracticesDocument10 pagesAccounting Principles and PracticesGaganpreet KaurNo ratings yet

- An Instrument Is Non-Negotiable Under The Negotiable Instruments Law (NIL) If It StatesDocument2 pagesAn Instrument Is Non-Negotiable Under The Negotiable Instruments Law (NIL) If It StatesHarjade Segura DammangNo ratings yet

- Securities Instructon FormDocument1 pageSecurities Instructon FormAngelica DerechoNo ratings yet

- Finance Department Egovernance Group: Government of West BengalDocument77 pagesFinance Department Egovernance Group: Government of West BengalDebjaniDasNo ratings yet

- ARSOP 2.0 Allowance For Doubtful AccountsDocument5 pagesARSOP 2.0 Allowance For Doubtful AccountsSelenge DaaduuNo ratings yet

- February 17, 2010Document13 pagesFebruary 17, 2010LargeCapTraderNo ratings yet

- Asset Liabilities + Owner'S EquityDocument4 pagesAsset Liabilities + Owner'S EquitydenixngNo ratings yet

- Ali Mousa and Sons ContractingDocument1 pageAli Mousa and Sons ContractingMohsin aliNo ratings yet

- Lecture 4 Exercises Sofp 1Document2 pagesLecture 4 Exercises Sofp 1Ziyodullo IsroilovNo ratings yet

- May 5, 2018 Chandigarh: Presenter: CA Akesh VyasDocument33 pagesMay 5, 2018 Chandigarh: Presenter: CA Akesh Vyassukumar basuNo ratings yet

- Hire Purchase Lease Financing - Part 2Document38 pagesHire Purchase Lease Financing - Part 2KomalNo ratings yet

- Accounting For Manager Complete NotesDocument105 pagesAccounting For Manager Complete NotesAARTI100% (2)

- Standalone Cash Flow Statement InsightsDocument2 pagesStandalone Cash Flow Statement InsightsRupasinghNo ratings yet

- Control Final o LevelDocument18 pagesControl Final o Levelparwez_0505No ratings yet

- Unit 1Document40 pagesUnit 1Neha GargNo ratings yet

- Deutsche Bank - Global Banking Trends After The GFCDocument24 pagesDeutsche Bank - Global Banking Trends After The GFClelaissezfaire100% (2)

- Expenditure Cycle Part II: Payroll & Fixed Asset ProceduresDocument14 pagesExpenditure Cycle Part II: Payroll & Fixed Asset ProceduresJessalyn DaneNo ratings yet

- Direct MayDocument8 pagesDirect MayabcNo ratings yet

- ACT 2100 Worksheet IVDocument7 pagesACT 2100 Worksheet IVAshmini PershadNo ratings yet

- Rbi Act 1934Document50 pagesRbi Act 1934manisha sonawaneNo ratings yet

- Donaldson - Thinking About CreditDocument145 pagesDonaldson - Thinking About CreditMelih OktayNo ratings yet

- Tata AigDocument11 pagesTata AigAmit ChoudhuryNo ratings yet

- Frequently Asked Questions on Finacle Core Banking SolutionDocument76 pagesFrequently Asked Questions on Finacle Core Banking Solutionbalraj0% (1)