You might also like

- Investing 101: From Stocks and Bonds to ETFs and IPOs, an Essential Primer on Building a Profitable PortfolioFrom EverandInvesting 101: From Stocks and Bonds to ETFs and IPOs, an Essential Primer on Building a Profitable PortfolioRating: 4.5 out of 5 stars4.5/5 (38)

- Solutions For End-of-Chapter Questions and Problems: Chapter EightDocument25 pagesSolutions For End-of-Chapter Questions and Problems: Chapter EightSam MNo ratings yet

- EOC08 UpdatedDocument25 pagesEOC08 Updatedtaha elbakkushNo ratings yet

- Human Resource Management EnvironmentDocument28 pagesHuman Resource Management EnvironmentSe SathyaNo ratings yet

- Finanzas CorporativasDocument2 pagesFinanzas CorporativasAshley MNo ratings yet

- CorporateFinanceGE2e PDFDocument2 pagesCorporateFinanceGE2e PDFAshley MNo ratings yet

- Chapter 5: Introduction To Risk, Return, and The Historical RecordDocument6 pagesChapter 5: Introduction To Risk, Return, and The Historical RecordMehrab Jami Aumit 1812818630No ratings yet

- Interest Rate: Education in Economics SeriesDocument32 pagesInterest Rate: Education in Economics Seriesnadine enseinNo ratings yet

- Interest Rate - Cap Rate Economics 2018Document15 pagesInterest Rate - Cap Rate Economics 2018Geraldy Dearma PradhanaNo ratings yet

- 2033314, Macro CIA-3Document8 pages2033314, Macro CIA-3Rohan GargNo ratings yet

- Inflation Deflation DebateDocument6 pagesInflation Deflation DebatemordenviabankNo ratings yet

- Chapter 5: Introduction To Risk, Return, and The Historical RecordDocument7 pagesChapter 5: Introduction To Risk, Return, and The Historical RecordQingyu MaiNo ratings yet

- Points To Remember #Document69 pagesPoints To Remember #Ryan DixonNo ratings yet

- Correlation and Diversification 1Document3 pagesCorrelation and Diversification 1Poonam BathijaNo ratings yet

- The Economy Is in A Recession:: Analysis of US Economy From 2005-2010Document6 pagesThe Economy Is in A Recession:: Analysis of US Economy From 2005-2010Jake SchnallNo ratings yet

- Impact of Rising Interest Rates On Equity MarketsDocument9 pagesImpact of Rising Interest Rates On Equity MarketsDeepak DharmavaramNo ratings yet

- Problem & SolutionDocument19 pagesProblem & Solutionfanuel kijojiNo ratings yet

- HY and Market MakersDocument6 pagesHY and Market MakersfcamargoeNo ratings yet

- Bonds Today Part 2 Its Not A Bound Its An OpinionDocument12 pagesBonds Today Part 2 Its Not A Bound Its An OpinionFranklinNo ratings yet

- Treasury Outlook MarDocument6 pagesTreasury Outlook Marelise_stefanikNo ratings yet

- Bundesbank Risk PaperDocument13 pagesBundesbank Risk PaperJohn HuttonNo ratings yet

- BNP Derivs 101Document117 pagesBNP Derivs 101hjortsberg100% (2)

- Chiến luocwjj đầu tưDocument8 pagesChiến luocwjj đầu tưTố NiênNo ratings yet

- What Effect Has Quantitative Easing Had On Your Share Price?Document4 pagesWhat Effect Has Quantitative Easing Had On Your Share Price?dhandadhanNo ratings yet

- Monetary: TrendsDocument20 pagesMonetary: Trendsapi-25887578No ratings yet

- Answer and ExplanationDocument2 pagesAnswer and ExplanationJohn TomNo ratings yet

- Mathematics in Financial Risk ManagementDocument10 pagesMathematics in Financial Risk ManagementJamel GriffinNo ratings yet

- Brooks - AQR Drivers of Bond YieldsDocument27 pagesBrooks - AQR Drivers of Bond YieldsStephen LinNo ratings yet

- Low Rates and Bank Stability: The Risk of A Tipping PointDocument4 pagesLow Rates and Bank Stability: The Risk of A Tipping Pointbob.winarskiNo ratings yet

- Chap 007Document20 pagesChap 007Adi SusiloNo ratings yet

- Financial Institutions Management - Solutions - Chap008Document19 pagesFinancial Institutions Management - Solutions - Chap008duncan01234No ratings yet

- Self Review MidtermDocument5 pagesSelf Review MidtermDanicaNo ratings yet

- The Relationship Between Property Yields and Interest RatesDocument9 pagesThe Relationship Between Property Yields and Interest RatesAlex PalcovNo ratings yet

- Bond StrategiesDocument6 pagesBond Strategiesamitva2007No ratings yet

- Iridian 3Q10 LetterDocument15 pagesIridian 3Q10 LetterHariharan SundaresanNo ratings yet

- El2018 06Document5 pagesEl2018 06TBP_Think_TankNo ratings yet

- EditedDocument12 pagesEditedKeii blackhoodNo ratings yet

- M&B HK Ch7 20Document2 pagesM&B HK Ch7 20K60 Phạm Thị Phương AnhNo ratings yet

- Types of Investment Risk TemplateDocument3 pagesTypes of Investment Risk TemplateShaari HusinNo ratings yet

- 1909 Ausbil Unitholder Report PDFDocument32 pages1909 Ausbil Unitholder Report PDFTonyNo ratings yet

- WEEK 12 MergedDocument21 pagesWEEK 12 MergedAnirudh KalraNo ratings yet

- Week in Pictures 10 17 22 1666106256Document13 pagesWeek in Pictures 10 17 22 1666106256Barry HeNo ratings yet

- BKM9e Answers Chap005Document6 pagesBKM9e Answers Chap005soul1971No ratings yet

- Chapter 008Document25 pagesChapter 008Muhammad Bilal TariqNo ratings yet

- 2019macro Outlook PDFDocument71 pages2019macro Outlook PDFAdiKangdraNo ratings yet

- Interest Rates Have Risen Sharply. But Is Monetary Policy Truly Tight - The EconomistDocument6 pagesInterest Rates Have Risen Sharply. But Is Monetary Policy Truly Tight - The EconomistDito InculoNo ratings yet

- The Politics of Forecast Bias Forecaster EffectDocument18 pagesThe Politics of Forecast Bias Forecaster EffectTraining TrainingNo ratings yet

- Chapter 5: Introduction To Risk, Return, and The Historical RecordDocument7 pagesChapter 5: Introduction To Risk, Return, and The Historical RecordBiloni KadakiaNo ratings yet

- Financial Markets, Institutions & Instruments: CourseworkDocument9 pagesFinancial Markets, Institutions & Instruments: CourseworkIago SelemeNo ratings yet

- Fixed and Variable Interest Rates: For Private Education LoansDocument12 pagesFixed and Variable Interest Rates: For Private Education LoansJahangir SafarovNo ratings yet

- EOC08 EdittedDocument12 pagesEOC08 EdittedFilip velico100% (1)

- CH 8Document9 pagesCH 8realsimplemusicNo ratings yet

- Fixed Income Is NecessaryDocument11 pagesFixed Income Is NecessaryAkshat TulsyanNo ratings yet

- When Interest Rates Rise: Less Than 2%Document11 pagesWhen Interest Rates Rise: Less Than 2%macurriNo ratings yet

- CFA Exercise With Solution - Chap 15Document5 pagesCFA Exercise With Solution - Chap 15Fagbola Oluwatobi OmolajaNo ratings yet

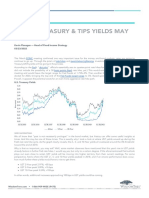

- Blog - Where Treasury TIPS Yields May Be HeadedDocument5 pagesBlog - Where Treasury TIPS Yields May Be HeadedOwm Close CorporationNo ratings yet

- Svensson, L. (2003) - Escaping From A Liquidity Trap and DeflationDocument26 pagesSvensson, L. (2003) - Escaping From A Liquidity Trap and DeflationAnonymous WFjMFHQNo ratings yet

- Forecasting in An Uncertain World - 8 Dec 2010Document12 pagesForecasting in An Uncertain World - 8 Dec 2010peter_martin9335No ratings yet

- Bond Yield Curve Holds Predictive PowersDocument15 pagesBond Yield Curve Holds Predictive PowersZuniButtNo ratings yet

- Common Sense Retirement Planning: Home, Savings and InvestmentFrom EverandCommon Sense Retirement Planning: Home, Savings and InvestmentNo ratings yet

- Brea ch05 BMM 7e SGDocument91 pagesBrea ch05 BMM 7e SGAshish BhallaNo ratings yet

- Economic History of Nazi Regime A. ToozeDocument14 pagesEconomic History of Nazi Regime A. ToozeIoproprioio100% (1)

- Unit IV - Impact of World War I & II On The Indian EconomyDocument6 pagesUnit IV - Impact of World War I & II On The Indian Economymayangpongen3No ratings yet

- Life Care (PVT) LTDDocument62 pagesLife Care (PVT) LTDmuza_marwan100% (1)

- Salary Survey 2016Document400 pagesSalary Survey 2016sinaNo ratings yet

- CSEC Economics June 2011 P1Document10 pagesCSEC Economics June 2011 P1Sachin BahadoorsinghNo ratings yet

- Procurement and Supplies Professionals A PDFDocument115 pagesProcurement and Supplies Professionals A PDFNyeko FrancisNo ratings yet

- Caligulas Economic ImpactDocument1 pageCaligulas Economic Impactbog macNo ratings yet

- Profit MGT & InflationDocument21 pagesProfit MGT & InflationParkhi AgarwalNo ratings yet

- 1234567890Document43 pages1234567890Aamir HusainNo ratings yet

- Solved Now Consider A TFP Shock That Is Permanent For ExampleDocument1 pageSolved Now Consider A TFP Shock That Is Permanent For ExampleM Bilal SaleemNo ratings yet

- TPIPL Final ReportDocument48 pagesTPIPL Final ReportNgoc Nguyen HongNo ratings yet

- Macroeconomics Ganesh Kumar NDocument44 pagesMacroeconomics Ganesh Kumar NHimanshu JainNo ratings yet

- Mgnrega A Critical AnalysisDocument33 pagesMgnrega A Critical AnalysisShubhankar Johari0% (1)

- Carlton Ihrm 6Document50 pagesCarlton Ihrm 6Prashant JadhavNo ratings yet

- Bolivia Poverty Report 1990Document180 pagesBolivia Poverty Report 1990ARKNo ratings yet

- 2019 MEFMI Prospectus PDFDocument44 pages2019 MEFMI Prospectus PDFBlessing KatukaNo ratings yet

- CHAPTER 3-The Impact of Inflation On PerformanceDocument10 pagesCHAPTER 3-The Impact of Inflation On PerformanceNelson PayendaNo ratings yet

- Chapter 23 - Measuring A Nation - S Income - 2 PDFDocument50 pagesChapter 23 - Measuring A Nation - S Income - 2 PDFthanhvu78No ratings yet

- Price Level AccountingDocument14 pagesPrice Level AccountingNadia StephensNo ratings yet

- 1.0 Determining Replacement Asset Value (Rav)Document3 pages1.0 Determining Replacement Asset Value (Rav)cksNo ratings yet

- 6.challenges Facing The Singapore EconomyDocument14 pages6.challenges Facing The Singapore EconomyLets LearnNo ratings yet

- Interest Rates and Their Role in FinanceDocument17 pagesInterest Rates and Their Role in FinanceClyden Jaile RamirezNo ratings yet

- SCQF Level 6 Program CurriculumDocument40 pagesSCQF Level 6 Program CurriculumbobbsuannaNo ratings yet

- Bugatti PESTLE AnalysisDocument4 pagesBugatti PESTLE AnalysisSaurabhkumar SinghNo ratings yet

- 06 Chapter 1Document52 pages06 Chapter 1yezdiarwNo ratings yet

- Macro-Economic Principles and Macro-Economic Objectives of A CountryDocument46 pagesMacro-Economic Principles and Macro-Economic Objectives of A Countrydush_qs_883176404No ratings yet

- The Money Masters - ReportDocument59 pagesThe Money Masters - ReportSamiyaIllias100% (2)

- Portfolio Management 1Document28 pagesPortfolio Management 1Sattar Md AbdusNo ratings yet