You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Employee DevelopmentDocument7 pagesEmployee DevelopmentSančo PansaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Drug and Alcohol Awareness-Employee TrainingDocument59 pagesDrug and Alcohol Awareness-Employee TrainingRaymond M. LacsonNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Gokuldas Case StudyDocument4 pagesGokuldas Case Studymadhuri_trivedi04No ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Forfeiture of GratuityDocument40 pagesForfeiture of GratuitySangeetha SasidharanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Human Capital Leader InterviewDocument11 pagesHuman Capital Leader Interviewapi-655123959No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Employee Bonus Policy TemplateDocument3 pagesEmployee Bonus Policy Templatekool100% (3)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- "Shaking Pillow": "Manage Your Time To A Better Life"Document26 pages"Shaking Pillow": "Manage Your Time To A Better Life"Shahriar ZamanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Quality Manual - IsO 900Document31 pagesQuality Manual - IsO 900अंजनी श्रीवास्तवNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Module 1 Trainer Manual PDFDocument26 pagesModule 1 Trainer Manual PDFSanath KamilaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Indian Weekender 27 October 2017Document32 pagesIndian Weekender 27 October 2017Indian WeekenderNo ratings yet

- Lee vs. Smsls-Naflu-KmuDocument3 pagesLee vs. Smsls-Naflu-KmuOlan Dave Lachica100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- National Grid Safety Procedure: N-1402 Contractor Safety Requirements DateDocument50 pagesNational Grid Safety Procedure: N-1402 Contractor Safety Requirements DateKevin DucusinNo ratings yet

- STRM042 Critical Issues in Business Chandana Kumara 18414494 Final v3Document10 pagesSTRM042 Critical Issues in Business Chandana Kumara 18414494 Final v3PradeepaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Philippines Covid-19 Emergency Response Project: DraftDocument118 pagesPhilippines Covid-19 Emergency Response Project: DraftMikoleta RamosNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- AlbaniaDocument12 pagesAlbaniaHermes GjinajNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Guidelines On The Grant of Collective Negotiation Agreement Incentive FY 2012Document8 pagesGuidelines On The Grant of Collective Negotiation Agreement Incentive FY 2012Jonas Reduta CabacunganNo ratings yet

- ApplicationFoEmployment - Revised 010117 - EnglishDocument4 pagesApplicationFoEmployment - Revised 010117 - EnglishSuman DakNo ratings yet

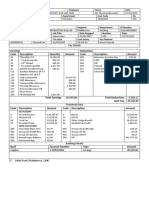

- Pay Details: Earnings Deductions Code Description Quantity Amount Code Description AmountDocument1 pagePay Details: Earnings Deductions Code Description Quantity Amount Code Description AmountVee-kay Vicky KatekaniNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Akerlof Shiller Animal SpiritsDocument8 pagesAkerlof Shiller Animal Spiritsgemba88No ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Assesment 1 BSBLDRDocument20 pagesAssesment 1 BSBLDRstar trendz100% (2)

- 03 Service CharacteristicsDocument20 pages03 Service CharacteristicsShikha GuptaNo ratings yet

- Workmen's Compensation Act, 1923Document15 pagesWorkmen's Compensation Act, 1923Saksham Gaur50% (2)

- Printedintheu S ADocument32 pagesPrintedintheu S AIATSENo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Summer Internship Report On Human Resource Management At: Zeba ShafiqDocument63 pagesSummer Internship Report On Human Resource Management At: Zeba ShafiqSatyam Shukla100% (1)

- January 22, 2016 Strathmore TimesDocument36 pagesJanuary 22, 2016 Strathmore TimesStrathmore TimesNo ratings yet

- William Mathews EU Design CaseDocument5 pagesWilliam Mathews EU Design Caseeduardo.honorato5586No ratings yet

- QW-Performance Review TemplatesDocument19 pagesQW-Performance Review TemplatesLaksana Anugrah PutraNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- PAFLU vs. Binalbagan Isabela Sugar CoDocument6 pagesPAFLU vs. Binalbagan Isabela Sugar CoFaithmaeNo ratings yet

- Gender Equality Is A Human RightDocument4 pagesGender Equality Is A Human RightjjhjhjNo ratings yet

- Project Proposal For The Construction of Mixed Use Building: Promoter:-Mr - Mohammednazif Aba MechaDocument42 pagesProject Proposal For The Construction of Mixed Use Building: Promoter:-Mr - Mohammednazif Aba MechaRidwan Sultan100% (2)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)