You might also like

- Hilado and Hilado For Petitioner. Office of The Solicitor General For RespondentsDocument40 pagesHilado and Hilado For Petitioner. Office of The Solicitor General For Respondentsheidi marieNo ratings yet

- Lladoc Vs Commissioner of Internal RevenueDocument3 pagesLladoc Vs Commissioner of Internal RevenuebuloytedNo ratings yet

- Donors Tax CasesDocument66 pagesDonors Tax CasesMai ReamicoNo ratings yet

- Taxation CasesDocument353 pagesTaxation Casesjojazz74No ratings yet

- Lladoc Vs Commissioner of Internal Revenue (G.R. No. L-19201, June 16, 1965) PDFDocument4 pagesLladoc Vs Commissioner of Internal Revenue (G.R. No. L-19201, June 16, 1965) PDFFrancis Gillean OrpillaNo ratings yet

- Lladoc vs. CIR (G.R. No. L-19201 June 16, 1965) - H DIGESTDocument1 pageLladoc vs. CIR (G.R. No. L-19201 June 16, 1965) - H DIGESTHarleneNo ratings yet

- Lladoc v. CIRDocument6 pagesLladoc v. CIRKyrzen NovillaNo ratings yet

- UntitledDocument1 pageUntitledAKnownKneeMouseeNo ratings yet

- Tax2 - Donors TaxDocument34 pagesTax2 - Donors TaxJia FriasNo ratings yet

- Supreme Court Upholds Donee's Gift Tax on Donation to Catholic ChurchDocument3 pagesSupreme Court Upholds Donee's Gift Tax on Donation to Catholic ChurchVirgillo V. Adonis, Jr.No ratings yet

- Lladoc vs. Commissioner of Internal Revenue, 14 SCRA 292, No. L-19201 June 16, 1965Document3 pagesLladoc vs. Commissioner of Internal Revenue, 14 SCRA 292, No. L-19201 June 16, 1965PNP MayoyaoNo ratings yet

- Rev FR Casimiro Lladoc Vs Commissioner of Internal Revenue (CIR) 121 Phil 1074 14 SCRA 292Document3 pagesRev FR Casimiro Lladoc Vs Commissioner of Internal Revenue (CIR) 121 Phil 1074 14 SCRA 292RaymondNo ratings yet

- Chapter Vi: Taxation NO. 3: Hilado and Hilado For Petitioner. Office of The Solicitor General For RespondentsDocument3 pagesChapter Vi: Taxation NO. 3: Hilado and Hilado For Petitioner. Office of The Solicitor General For RespondentsIncess CessNo ratings yet

- Donee Gift Tax CaseDocument1 pageDonee Gift Tax CaseJJMONo ratings yet

- Case 90 Lladoc vs. Comm. of Int. Rev. 14 SCRA 292 1965 Facts: Sometime in 1957, The M.B. Estate, Inc., of Bacolod City, Donated P10,000.00 inDocument6 pagesCase 90 Lladoc vs. Comm. of Int. Rev. 14 SCRA 292 1965 Facts: Sometime in 1957, The M.B. Estate, Inc., of Bacolod City, Donated P10,000.00 inDawn Jessa GoNo ratings yet

- Rev. Fr. Casimiro Lladoc vs. CirDocument5 pagesRev. Fr. Casimiro Lladoc vs. CirJoyce VillanuevaNo ratings yet

- Catholic Diocese Liable for Gift Tax on Church DonationDocument40 pagesCatholic Diocese Liable for Gift Tax on Church Donationheidi marieNo ratings yet

- REV. FR. CASIMIRO LLADOC, Petitioner, vs. The Commissioner of Internal Revenue and The Court of Tax Appeals, RespondentsDocument3 pagesREV. FR. CASIMIRO LLADOC, Petitioner, vs. The Commissioner of Internal Revenue and The Court of Tax Appeals, RespondentsAname BarredoNo ratings yet

- Petitioner vs. VS.: Second DivisionDocument5 pagesPetitioner vs. VS.: Second DivisionBest KuroroNo ratings yet

- Case Digest - TaxationDocument7 pagesCase Digest - TaxationJane Dela CruzNo ratings yet

- Case Digest Political LawDocument21 pagesCase Digest Political LawJayne CabuhalNo ratings yet

- Lladoc Vs CIRDocument2 pagesLladoc Vs CIRBryne Angelo BrillantesNo ratings yet

- Lladoc VS CirDocument2 pagesLladoc VS CirLeonardo Jr LawasNo ratings yet

- Lladoc vs. Commissioner of Internal RevenueDocument2 pagesLladoc vs. Commissioner of Internal RevenueCecil MoriNo ratings yet

- CASE DIGEST: Lladoc Vs Commissioner of Internal Revenue G.R. No. L-19201Document2 pagesCASE DIGEST: Lladoc Vs Commissioner of Internal Revenue G.R. No. L-19201Lyka Angelique Cisneros100% (2)

- Lladoc's Contention: at The Time of The Donation, He Was Not The Parish Priest in Victorias That There IsDocument2 pagesLladoc's Contention: at The Time of The Donation, He Was Not The Parish Priest in Victorias That There IsKarenliambrycejego RagragioNo ratings yet

- Lladoc vs. CommissionerDocument2 pagesLladoc vs. CommissionerCZARINA AUDREY SILVANONo ratings yet

- Taxation Case DigestDocument23 pagesTaxation Case DigestAnonymous vUC7HI2BNo ratings yet

- Lladoc vs. CIR Digested CaseDocument1 pageLladoc vs. CIR Digested CaseRaymer OclaritNo ratings yet

- Lladoc VS CirDocument2 pagesLladoc VS CirKath LeenNo ratings yet

- Lladoc VS CirDocument1 pageLladoc VS CirYosi IsoyNo ratings yet

- CIR Gift Tax RulingDocument2 pagesCIR Gift Tax RulingNurwisa SamlaNo ratings yet

- Abra Vs Hernando DigestDocument1 pageAbra Vs Hernando DigestJann Tecson-FernandezNo ratings yet

- Power of Taxation - 3. Lladoc v. CIRDocument1 pagePower of Taxation - 3. Lladoc v. CIRPaul Joshua Torda SubaNo ratings yet

- Freila Digest - Lladoc Vs CirDocument1 pageFreila Digest - Lladoc Vs CirRen MagallonNo ratings yet

- Lladoc vs. CommissionerDocument3 pagesLladoc vs. CommissionerJanMarkMontedeRamosWongNo ratings yet

- Lladoc Vs CirDocument1 pageLladoc Vs CirRea RomeroNo ratings yet

- Taxation and Due Process CasesDocument124 pagesTaxation and Due Process CasesAG DQNo ratings yet

- Province of Abra vs. HernandoDocument2 pagesProvince of Abra vs. HernandoBryce KingNo ratings yet

- Lladoc vs. vs. CIRDocument1 pageLladoc vs. vs. CIRHoney Joy MBNo ratings yet

- VNJDocument2 pagesVNJjulyenfortunatoNo ratings yet

- Lladoc V CIRDocument1 pageLladoc V CIRM A J esty FalconNo ratings yet

- 34 Lladoc vs. Commissioner of Internal RevenueDocument1 page34 Lladoc vs. Commissioner of Internal RevenueAmity Rose RiveroNo ratings yet

- Donor Tax GuideDocument13 pagesDonor Tax GuideRovi Anne IgoyNo ratings yet

- Donor Tax GuideDocument13 pagesDonor Tax GuideRovi IgoyNo ratings yet

- Case Digest - QuizDocument6 pagesCase Digest - Quizjennalyn nemoNo ratings yet

- Lladoc V CIRDocument2 pagesLladoc V CIRM A J esty FalconNo ratings yet

- Province of Abra V HernandoDocument1 pageProvince of Abra V HernandoM A J esty FalconNo ratings yet

- 3 TAXATION DigestsDocument9 pages3 TAXATION DigestsSam ENo ratings yet

- Batch 2 Consti 2Document10 pagesBatch 2 Consti 2Ivann EndozoNo ratings yet

- 34 The Province of Abra vs. HernandoDocument2 pages34 The Province of Abra vs. HernandoFred Michael L. GoNo ratings yet

- 101-CIR v. Bishop of The Missionary District, August 31, 1965Document3 pages101-CIR v. Bishop of The Missionary District, August 31, 1965Jopan SJNo ratings yet

- Province of Abra Tax Exemption CaseDocument1 pageProvince of Abra Tax Exemption CaselexxNo ratings yet

- Province of Abra Vs Judge Hernando (Case Digest)Document2 pagesProvince of Abra Vs Judge Hernando (Case Digest)Johney Doe100% (2)

- TaxationDocument2 pagesTaxationotthonrpolisisNo ratings yet

- The Clergyman's Hand-book of Law: The Law of Church and GraveFrom EverandThe Clergyman's Hand-book of Law: The Law of Church and GraveNo ratings yet

- The Rise and Progress of Whiskey-Drinking in Scotland, and the Working of the 'Public-Houses (Scotland) ACT', Commonly Called the Forbes McKenzie ACTFrom EverandThe Rise and Progress of Whiskey-Drinking in Scotland, and the Working of the 'Public-Houses (Scotland) ACT', Commonly Called the Forbes McKenzie ACTNo ratings yet

- Act, Declaration, & Testimony for the Whole of our Covenanted Reformation, as Attained to, and Established in Britain and Ireland; Particularly Betwixt the Years 1638 and 1649, InclusiveFrom EverandAct, Declaration, & Testimony for the Whole of our Covenanted Reformation, as Attained to, and Established in Britain and Ireland; Particularly Betwixt the Years 1638 and 1649, InclusiveNo ratings yet

- Churchwardens' Manual their duties, powers, rights, and privilagesFrom EverandChurchwardens' Manual their duties, powers, rights, and privilagesNo ratings yet

- Perspectives Tet Offensive PDFDocument4 pagesPerspectives Tet Offensive PDFJoielyn Dy DimaanoNo ratings yet

- 1) When Compelling Reasons So Warrant or When The PurposeDocument16 pages1) When Compelling Reasons So Warrant or When The PurposeJoielyn Dy DimaanoNo ratings yet

- Bar Bulletin 10Document8 pagesBar Bulletin 10xdesczaNo ratings yet

- Dimaano v. Manila PoliceDocument4 pagesDimaano v. Manila PoliceJoielyn Dy DimaanoNo ratings yet

- Tet OffensiveDocument2 pagesTet OffensiveJoielyn Dy DimaanoNo ratings yet

- Solidbank Corporation/ Metropolitan Bank and Trust Company, Petitioner, vs. SPOUSES PETER and SUSAN TAN, RespondentsDocument9 pagesSolidbank Corporation/ Metropolitan Bank and Trust Company, Petitioner, vs. SPOUSES PETER and SUSAN TAN, RespondentsJoielyn Dy DimaanoNo ratings yet

- Dear Graduate:: (Married But Not Living With (Born A Child But Not Married) Spouse)Document3 pagesDear Graduate:: (Married But Not Living With (Born A Child But Not Married) Spouse)Joielyn Dy DimaanoNo ratings yet

- UkygkuygjhDocument2 pagesUkygkuygjhJoielyn Dy DimaanoNo ratings yet

- Poli Rev Case DigestsDocument95 pagesPoli Rev Case DigestsJoielyn Dy DimaanoNo ratings yet

- Chartered Bank Vs SenateDocument2 pagesChartered Bank Vs SenateJoielyn Dy DimaanoNo ratings yet

- Poli Digests85 126 PDFDocument64 pagesPoli Digests85 126 PDFJoielyn Dy DimaanoNo ratings yet

- Ladlad V COmelecDocument3 pagesLadlad V COmelecJoielyn Dy DimaanoNo ratings yet

- Civil Syllabus PDFDocument14 pagesCivil Syllabus PDFHabib SimbanNo ratings yet

- Civil Syllabus PDFDocument14 pagesCivil Syllabus PDFHabib SimbanNo ratings yet

- Ra 9165Document35 pagesRa 9165Aya FernandezNo ratings yet

- Poli Rev Case DigestsDocument95 pagesPoli Rev Case DigestsJoielyn Dy DimaanoNo ratings yet

- Chartered Bank Vs SenateDocument2 pagesChartered Bank Vs SenateJoielyn Dy DimaanoNo ratings yet

- 1 42 - Polirev Case Digests PDFDocument83 pages1 42 - Polirev Case Digests PDFJoielyn Dy DimaanoNo ratings yet

- CHAN WAN V TAN KIMDocument1 pageCHAN WAN V TAN KIMJoielyn Dy DimaanoNo ratings yet

- 1 42 - Polirev Case Digests PDFDocument83 pages1 42 - Polirev Case Digests PDFJoielyn Dy DimaanoNo ratings yet

- Wells Fargo V CollectorDocument10 pagesWells Fargo V CollectorJoielyn Dy DimaanoNo ratings yet

- KLM LKDocument3 pagesKLM LKJoielyn Dy DimaanoNo ratings yet

- Re: Request of National Committee On Legal Aid Citation: A.M. No. 08-11-7-SC Date of Promulgation: August 28, 2009 Ponente: Corona, JDocument5 pagesRe: Request of National Committee On Legal Aid Citation: A.M. No. 08-11-7-SC Date of Promulgation: August 28, 2009 Ponente: Corona, JJoielyn Dy DimaanoNo ratings yet

- Tagolino V HRET DigestDocument2 pagesTagolino V HRET DigestKrizzia Gojar100% (1)

- Policy Effective June 22, 1999Document6 pagesPolicy Effective June 22, 1999Joielyn Dy DimaanoNo ratings yet

- Cocofed Vs RepublicDocument1 pageCocofed Vs Republicmanilyn0925% (4)

- PNB v RITRATTO: Preliminary Injunction Lifted Due to Dismissal of CaseDocument7 pagesPNB v RITRATTO: Preliminary Injunction Lifted Due to Dismissal of CaseJoielyn Dy DimaanoNo ratings yet

- Federal V LinesDocument5 pagesFederal V LinesJoielyn Dy DimaanoNo ratings yet

- Federal V LinesDocument5 pagesFederal V LinesJoielyn Dy DimaanoNo ratings yet

- IhiouhDocument27 pagesIhiouhJoielyn Dy DimaanoNo ratings yet

- Mumbai Airport To MumbaiDocument3 pagesMumbai Airport To MumbaiAbhishek UpadhyayNo ratings yet

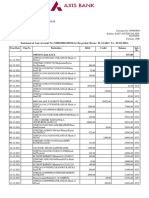

- Statement of Axis Account No:920010006130934 For The Period (From: 01-12-2021 To: 09-05-2022)Document13 pagesStatement of Axis Account No:920010006130934 For The Period (From: 01-12-2021 To: 09-05-2022)subhadeepNo ratings yet

- New TDS & TCS Provisions - SummaryDocument12 pagesNew TDS & TCS Provisions - Summaryyashgoyal87502No ratings yet

- TRACKING#:13390535151384: Delhivery SurfaceDocument2 pagesTRACKING#:13390535151384: Delhivery SurfaceSiva SankariNo ratings yet

- Swiggy Order 44287204323 PDFDocument2 pagesSwiggy Order 44287204323 PDFAmazon AmazonNo ratings yet

- Week 3 Course Material For Income TaxationDocument11 pagesWeek 3 Course Material For Income TaxationAshly MateoNo ratings yet

- Guest Accounting SORIADocument3 pagesGuest Accounting SORIAJennifer AdvientoNo ratings yet

- APC 210813164011619null 1795785832Document1 pageAPC 210813164011619null 1795785832ratnesh vaviaNo ratings yet

- Supplier Details Address of Delivery Bill To Party DetailsDocument4 pagesSupplier Details Address of Delivery Bill To Party DetailsMANGAL MUNSHINo ratings yet

- SSE UK Utility BillDocument2 pagesSSE UK Utility BillGeorge Ricky Hawkins100% (2)

- CUNY Standard Verification WorksheetDocument3 pagesCUNY Standard Verification Worksheethicu0No ratings yet

- Policy New Cheque Dishonour LATESTDocument18 pagesPolicy New Cheque Dishonour LATESTAdam MarakNo ratings yet

- 21 870 Campbelltown To Liverpool Via Glenfield 20230925 20231007 1Document6 pages21 870 Campbelltown To Liverpool Via Glenfield 20230925 20231007 1Neng RegsNo ratings yet

- PBBK Credit Card Form 201912Document5 pagesPBBK Credit Card Form 201912faezNo ratings yet

- HOUSING LOAN SELF-DECLARATIONDocument1 pageHOUSING LOAN SELF-DECLARATIONNAGARAJ M O100% (6)

- FGB SMS Banking User GuideDocument4 pagesFGB SMS Banking User GuideshahabduNo ratings yet

- CHAPTER 10 ALLOWABLE DEDUCTIONSDocument17 pagesCHAPTER 10 ALLOWABLE DEDUCTIONSKyle BacaniNo ratings yet

- SVA Statement 1547538374524 PDFDocument2 pagesSVA Statement 1547538374524 PDFTaufik KurrohmanNo ratings yet

- Christian Medical College Appointment for Bangladeshi PatientDocument2 pagesChristian Medical College Appointment for Bangladeshi Patientrana ranaNo ratings yet

- Fish Farming Project Proposal in PNGDocument1 pageFish Farming Project Proposal in PNGWillie PayneNo ratings yet

- OPN Hotline Bill Smart May 2023Document4 pagesOPN Hotline Bill Smart May 2023Joel R. BarbosaNo ratings yet

- ViewGOPDF - list - user (21) (1) शासनादेश PDFDocument3 pagesViewGOPDF - list - user (21) (1) शासनादेश PDFMadan ChaturvediNo ratings yet

- 6018-P1-Akuntansi-Lembar Kerja-Siklus PT Prima ElektronikDocument10 pages6018-P1-Akuntansi-Lembar Kerja-Siklus PT Prima ElektronikAlilaNo ratings yet

- Ascertaining What Constitutes A Permanent Establishment: An Analysis of DIT vs. M/S Samsung Heavy Industries Co. LTDDocument3 pagesAscertaining What Constitutes A Permanent Establishment: An Analysis of DIT vs. M/S Samsung Heavy Industries Co. LTDplag scan0% (1)

- Taxation 2 Midterm ExamDocument8 pagesTaxation 2 Midterm ExamMonkeyhead Dacono100% (1)

- Indian Income Tax Return Acknowledgement SummaryDocument1 pageIndian Income Tax Return Acknowledgement SummaryGanesh DasaraNo ratings yet

- Explai The Business Model of Nagad and SurjopayDocument5 pagesExplai The Business Model of Nagad and SurjopayGolam ZelaniNo ratings yet

- HSBC'S Swipe For Essentials Promo: Terms and ConditionsDocument3 pagesHSBC'S Swipe For Essentials Promo: Terms and Conditionsreuven sioseNo ratings yet

- Term Test 1Document5 pagesTerm Test 1lalshahbaz57No ratings yet

- What is an Open Check? (39 charactersDocument5 pagesWhat is an Open Check? (39 charactersEfren ChanNo ratings yet