You might also like

- Stock Volatility Perspective4Document5 pagesStock Volatility Perspective4annawitkowski88No ratings yet

- Hussman Funds - Stocks Extreme Conditions and Typical Outcomes - May 2, 2011Document6 pagesHussman Funds - Stocks Extreme Conditions and Typical Outcomes - May 2, 2011KoalaCapitalSICAVNo ratings yet

- Welcome To Financial Trend ForecasterDocument48 pagesWelcome To Financial Trend ForecasterPrincess BinsonNo ratings yet

- Supertrends (Review and Analysis of Tvede's Book)From EverandSupertrends (Review and Analysis of Tvede's Book)Rating: 5 out of 5 stars5/5 (2)

- Mauldin August 8Document10 pagesMauldin August 8richardck61No ratings yet

- Yield Curve What Is It Predicting YardeniDocument28 pagesYield Curve What Is It Predicting YardenisuksesNo ratings yet

- What Works When Infl Ation Hits?: May 2021 Time To Read: 8 MinutesDocument8 pagesWhat Works When Infl Ation Hits?: May 2021 Time To Read: 8 MinutesgdsfgdfaNo ratings yet

- Lessons From Capital Market History, Part 2: ViewpointDocument2 pagesLessons From Capital Market History, Part 2: ViewpointjamilkhannNo ratings yet

- Emp2Document8 pagesEmp2dpbasicNo ratings yet

- Historical U.S. Money Growth, Inflation, and Inflation CredibilityDocument12 pagesHistorical U.S. Money Growth, Inflation, and Inflation CredibilityTabletop237No ratings yet

- Understanding Economic Recessions and Their ImpactDocument70 pagesUnderstanding Economic Recessions and Their ImpactVivian ClementNo ratings yet

- Cycles BusinessDocument6 pagesCycles BusinessdeepakpaharyaNo ratings yet

- Lane Asset Management Market Commentary For Q3 2017Document15 pagesLane Asset Management Market Commentary For Q3 2017Edward C LaneNo ratings yet

- Advisory PDFDocument12 pagesAdvisory PDFAnonymous Feglbx5No ratings yet

- Wild But Not CrazyDocument5 pagesWild But Not Crazybeetho1990No ratings yet

- Market Analysis July 2022-1Document23 pagesMarket Analysis July 2022-1Abdulaziz AlshemaliNo ratings yet

- Bis Financial VolDocument15 pagesBis Financial VolmeetwithsanjayNo ratings yet

- Quarterly Report To ClientsDocument20 pagesQuarterly Report To ClientsgnarayNo ratings yet

- Yield CurveDocument10 pagesYield Curvekhurram_ahmedNo ratings yet

- Uncertainty and Style Dynamics: Portfolios Under ConstructionDocument27 pagesUncertainty and Style Dynamics: Portfolios Under ConstructionRaphael100% (1)

- 3 Scenarios For The Next BubbleDocument10 pages3 Scenarios For The Next Bubbleambasyapare1No ratings yet

- Perspective: Economic and MarketDocument6 pagesPerspective: Economic and MarketdpbasicNo ratings yet

- GTA Introduction RIA ProDocument7 pagesGTA Introduction RIA Prostreettalk700100% (2)

- Pring Turner Approach To Business Cycle Investing1Document12 pagesPring Turner Approach To Business Cycle Investing1Minh NguyễnNo ratings yet

- EMPv2Document6 pagesEMPv2dpbasicNo ratings yet

- Perspective: Economic and MarketDocument4 pagesPerspective: Economic and MarketdpbasicNo ratings yet

- Gloom Today, Boom TomorrowDocument11 pagesGloom Today, Boom TomorrowcafemutualNo ratings yet

- Investing For A New World: Managing Through Low Yields and High VolatilityDocument16 pagesInvesting For A New World: Managing Through Low Yields and High VolatilityPenna111No ratings yet

- Review of 2015 Executive Summary: Jim Freeman, CFP / Chris Jaccard, CFP, Cfa January 2016Document3 pagesReview of 2015 Executive Summary: Jim Freeman, CFP / Chris Jaccard, CFP, Cfa January 2016Anonymous Ht0MIJNo ratings yet

- Credit Suisse, Market Focus, Jan 17,2013Document12 pagesCredit Suisse, Market Focus, Jan 17,2013Glenn ViklundNo ratings yet

- Business Cycles Explained: Phases, Theories & Economic Indicators (39Document28 pagesBusiness Cycles Explained: Phases, Theories & Economic Indicators (39rajapatnaNo ratings yet

- TtoDocument34 pagesTtoParesh Shah100% (1)

- Perspective: Economic and MarketDocument6 pagesPerspective: Economic and MarketdpbasicNo ratings yet

- VORACIOUS VOLATILITY: A TIME TO REACT OR STAY THE COURSEDocument8 pagesVORACIOUS VOLATILITY: A TIME TO REACT OR STAY THE COURSElimesinferiorNo ratings yet

- The Bark Is Worse Than The BiteDocument6 pagesThe Bark Is Worse Than The BitedpbasicNo ratings yet

- Lane Asset Management Stock Market Commentary September 2015Document10 pagesLane Asset Management Stock Market Commentary September 2015Edward C LaneNo ratings yet

- PIMCO - Trend-Following Through The Rates CycleDocument8 pagesPIMCO - Trend-Following Through The Rates CyclespogoliNo ratings yet

- Financial Market AnalysisDocument83 pagesFinancial Market AnalysisAlessandra ZannellaNo ratings yet

- 1 - Dollar Cost Averaging: Stock Market TimingDocument30 pages1 - Dollar Cost Averaging: Stock Market TimingkenNo ratings yet

- Don't Worry Over CurrenciesDocument8 pagesDon't Worry Over CurrenciesbenmackNo ratings yet

- Time Series and Forecasting: Learning ObjectivesDocument33 pagesTime Series and Forecasting: Learning ObjectivesAkhlaq Ul HassanNo ratings yet

- Crashes and BustDocument17 pagesCrashes and BustAhmed GulNo ratings yet

- New Complete Market Breadth IndicatorsDocument30 pagesNew Complete Market Breadth Indicatorsemirav2100% (2)

- NoteDocument3 pagesNoteK59 Do Man NghiNo ratings yet

- VBDDocument10 pagesVBDLuvuyo MemelaNo ratings yet

- 02 SynopsisDocument44 pages02 SynopsisSanaullah M SultanpurNo ratings yet

- Liam Mescall Swaption ProjectDocument20 pagesLiam Mescall Swaption ProjectLiam MescallNo ratings yet

- Easy Volatility Investing StrategiesDocument33 pagesEasy Volatility Investing StrategiescttfsdaveNo ratings yet

- Investment Strategy: 'Tis The Season?Document5 pagesInvestment Strategy: 'Tis The Season?marketfolly.comNo ratings yet

- Why Is Market Volatility So Low?: Point of ViewDocument4 pagesWhy Is Market Volatility So Low?: Point of ViewSiti Aishah Umairah Naser Binti Abdul RahmanNo ratings yet

- UBS DEC Letter enDocument6 pagesUBS DEC Letter enDim moNo ratings yet

- Istilah NFPDocument6 pagesIstilah NFPHenry AndersonNo ratings yet

- Gokrn SpeechDocument13 pagesGokrn Speechashwini.krs80No ratings yet

- Mind the Gap: Commodities Face Dark Tunnel in Q1Document25 pagesMind the Gap: Commodities Face Dark Tunnel in Q1mirceastnNo ratings yet

- Charts and DescriptionsDocument4 pagesCharts and Descriptionsemirav2No ratings yet

- Economist Insights 2014 04 283Document2 pagesEconomist Insights 2014 04 283buyanalystlondonNo ratings yet

- The Best Strategies For Inflationary TimesDocument32 pagesThe Best Strategies For Inflationary TimesAlvaro Neto TarcilioNo ratings yet

- Jesse Livermore-How To Trade in Stocks (1940 Original) - EN PDFDocument80 pagesJesse Livermore-How To Trade in Stocks (1940 Original) - EN PDFSteve Yarnall100% (4)

- Understanding antitrust laws and how they protect consumersDocument10 pagesUnderstanding antitrust laws and how they protect consumersselozok1No ratings yet

- Background: Bai' 'Inah Concept Is Used in Malaysian Islamic Banking System and Capital MarketDocument3 pagesBackground: Bai' 'Inah Concept Is Used in Malaysian Islamic Banking System and Capital MarketNurDianaDzulkiplyNo ratings yet

- MT760 - GOLD FCO Liberty Local Miners LTD - MT 760 (5 - 10 MT)Document8 pagesMT760 - GOLD FCO Liberty Local Miners LTD - MT 760 (5 - 10 MT)Inverplay CorpNo ratings yet

- Chapter 9 SolutionsDocument4 pagesChapter 9 SolutionsVaibhav MehtaNo ratings yet

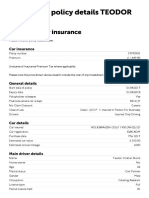

- Policy Details PageDocument2 pagesPolicy Details PageLuci PoroNo ratings yet

- Management Accounting Chapter 3 (Cost-Volume-Profit Chapter22)Document59 pagesManagement Accounting Chapter 3 (Cost-Volume-Profit Chapter22)yimerNo ratings yet

- Department of Management Studies Curriculum Bachelor of Business Management (BBM) 2013Document124 pagesDepartment of Management Studies Curriculum Bachelor of Business Management (BBM) 2013Sanjay YadavNo ratings yet

- Dev Academy of Science and Commerce March Examination 12 EconomicsDocument2 pagesDev Academy of Science and Commerce March Examination 12 Economicsरजत जाँगडाNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementShaikh GM33% (3)

- IS-LM Model ExplainedDocument36 pagesIS-LM Model ExplainedSyed Ali Zain100% (1)

- Consumer Behaviour On Impulse BuyingDocument17 pagesConsumer Behaviour On Impulse Buyingskv30june100% (23)

- Investor Behaviour MatrixDocument23 pagesInvestor Behaviour Matrixabhishek sharmaNo ratings yet

- Inven HW1Document2 pagesInven HW1Yolo PhongNo ratings yet

- Mikro EkonomiDocument3 pagesMikro EkonomiririanNo ratings yet

- INDUSTRY ANALYSIS FRAMEWORKDocument15 pagesINDUSTRY ANALYSIS FRAMEWORKChaitanya Reddy KondaNo ratings yet

- Kotak PMS Special Situations Value Presentation - Jan 18Document36 pagesKotak PMS Special Situations Value Presentation - Jan 18kanna275No ratings yet

- Economics For Managers Global Edition 3rd Edition Farnham Solutions ManualDocument16 pagesEconomics For Managers Global Edition 3rd Edition Farnham Solutions Manualchristinetayloraegynjcxdf100% (11)

- Fico Imp Interview QuestionsDocument50 pagesFico Imp Interview QuestionsNaveenNo ratings yet

- AssignmentDocument2 pagesAssignmentnavneet26101988No ratings yet

- RevenueDocument5 pagesRevenueTanya AroraNo ratings yet

- Road User Cost Models and Safety AnalysisDocument118 pagesRoad User Cost Models and Safety AnalysisMwawiNo ratings yet

- Chapter 11Document24 pagesChapter 11Julien KerroucheNo ratings yet

- Managerial Applications of StatisticsDocument10 pagesManagerial Applications of StatisticsSai Aditya100% (1)

- ACTG22a Midterm B 1Document5 pagesACTG22a Midterm B 1Kimberly RojasNo ratings yet

- IBNS Journal 38-3Document68 pagesIBNS Journal 38-3Aumair MalikNo ratings yet

- FILE 20220406 151306 Part 5 ToeicDocument380 pagesFILE 20220406 151306 Part 5 ToeicThuy TranNo ratings yet

- What Is The Capital Asset Pricing Model?Document5 pagesWhat Is The Capital Asset Pricing Model?Anne Kristine OniaNo ratings yet

- Understanding the Difference Between Positive and Normative EconomicsDocument21 pagesUnderstanding the Difference Between Positive and Normative EconomicsKevin Fernandez MendioroNo ratings yet

- 4 Inventory Planning and ControlDocument55 pages4 Inventory Planning and ControlSandeep SonawaneNo ratings yet

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)