You might also like

- Harvey Norman Tallaght - 394488 - 22.10.20Document2 pagesHarvey Norman Tallaght - 394488 - 22.10.20IONUT BABEINo ratings yet

- Lesson 5 Trend Rider StrategyDocument22 pagesLesson 5 Trend Rider StrategyKrimar HK Ltd100% (1)

- Business Finance: Quarter 4 - Module 1 The Different Types of InvestmentsDocument22 pagesBusiness Finance: Quarter 4 - Module 1 The Different Types of Investmentsrandy magbudhi71% (7)

- BUSN 115 Final Exam Answers - All Possible QuestionsDocument7 pagesBUSN 115 Final Exam Answers - All Possible QuestionsrebecapriceNo ratings yet

- Less Even Expansion, Rising Trade Tensions: For ReleaseDocument9 pagesLess Even Expansion, Rising Trade Tensions: For ReleaseTroyNo ratings yet

- IMF July 2019Document9 pagesIMF July 2019Carlos G.No ratings yet

- Executive Summary: World Economic Outlook: Tensions From The Two-Speed RecoveryDocument3 pagesExecutive Summary: World Economic Outlook: Tensions From The Two-Speed RecoveryVin odNo ratings yet

- Final MPR REPORT - 1Document14 pagesFinal MPR REPORT - 1HeenaNo ratings yet

- Executive Summary: A Weakening ExpansionDocument2 pagesExecutive Summary: A Weakening Expansionprashantk_106No ratings yet

- India Investment Strategy - November 18Document26 pagesIndia Investment Strategy - November 18shahavNo ratings yet

- Text Weo Update Jan 23Document11 pagesText Weo Update Jan 23pmendiet100% (1)

- Executive Summary: Global Economic EnvironmentDocument5 pagesExecutive Summary: Global Economic EnvironmentcherrypickerNo ratings yet

- 2015.10 Q3 CMC Efficient Frontier NewsletterDocument8 pages2015.10 Q3 CMC Efficient Frontier NewsletterJohn MathiasNo ratings yet

- Americas: Economic Review January 2011: at A GlanceDocument9 pagesAmericas: Economic Review January 2011: at A Glancemathew_rexNo ratings yet

- Foreword PDFDocument2 pagesForeword PDFyelzNo ratings yet

- Economy SlowdownDocument19 pagesEconomy Slowdownvipulgarg475651No ratings yet

- DM House ViewDocument2 pagesDM House ViewBolajoko OlusanyaNo ratings yet

- Asia: Bolstering Resilience Amid The SlowdownDocument19 pagesAsia: Bolstering Resilience Amid The SlowdownbreitnerNo ratings yet

- IMF - World Economic Outlook - Jul'23Document11 pagesIMF - World Economic Outlook - Jul'23wasranaNo ratings yet

- BBT Scott Stringfellow Jan 2019Document3 pagesBBT Scott Stringfellow Jan 2019rchawdhry123No ratings yet

- AIA Quarterly Investment InsightsDocument10 pagesAIA Quarterly Investment InsightsdesmondNo ratings yet

- World Economic Update July 2022Document19 pagesWorld Economic Update July 2022Tesfaye Taye EtanaNo ratings yet

- Team 2 Preliminary MPRDocument11 pagesTeam 2 Preliminary MPRHeenaNo ratings yet

- 2019 Themes Strategy En-2Document44 pages2019 Themes Strategy En-2Yahia Mohammed AbdelatifNo ratings yet

- The Global Economic EnvironnmentDocument51 pagesThe Global Economic EnvironnmentAbhinav AgrawalNo ratings yet

- Nedbank Se Rentekoers-Barometer November 2016Document4 pagesNedbank Se Rentekoers-Barometer November 2016Netwerk24SakeNo ratings yet

- Executive Summary: International Monetary Fund - October 2016Document4 pagesExecutive Summary: International Monetary Fund - October 2016Daniel GonzálezNo ratings yet

- Monetary Policy Summary and Minutes of The Monetary Policy Committee Meeting Ending On 6 February 2019Document13 pagesMonetary Policy Summary and Minutes of The Monetary Policy Committee Meeting Ending On 6 February 2019leseNo ratings yet

- Navigating A New Uncertainty: Market PerformanceDocument11 pagesNavigating A New Uncertainty: Market Performancedbr trackdNo ratings yet

- Quarterly Outlook - SVDocument6 pagesQuarterly Outlook - SVAldo WdnrNo ratings yet

- Economic World Article and The AnalysisDocument2 pagesEconomic World Article and The Analysisrahmirika0No ratings yet

- The Economy and Housing Continue To Tread Water: Two-Year Yields On Greek Debt SurgeDocument6 pagesThe Economy and Housing Continue To Tread Water: Two-Year Yields On Greek Debt SurgeRossy JonesNo ratings yet

- Safiullah Sir AssDocument6 pagesSafiullah Sir AssAvijit SahaNo ratings yet

- NAB Forecast (12 July 2011) : World Slows From Tsunami Disruptions and Tighter Policy.Document18 pagesNAB Forecast (12 July 2011) : World Slows From Tsunami Disruptions and Tighter Policy.International Business Times AUNo ratings yet

- Minutes January 2008Document10 pagesMinutes January 2008alina.w.siddiquiNo ratings yet

- Global Forecast: UpdateDocument6 pagesGlobal Forecast: Updatebkginting6300No ratings yet

- Group 5 - Marquette Case 8Document7 pagesGroup 5 - Marquette Case 8Bimly Shafara100% (1)

- Westpac WeeklyDocument10 pagesWestpac WeeklysugengNo ratings yet

- Tate Ank of Akistan: Onetary Olicy OmmitteeDocument2 pagesTate Ank of Akistan: Onetary Olicy OmmitteeSaqib Ahmed KhanNo ratings yet

- Monetary Policy Report - CanadaDocument12 pagesMonetary Policy Report - CanadaHeenaNo ratings yet

- Financial Crisis Means: IntroductionDocument3 pagesFinancial Crisis Means: IntroductionKaushlya DagaNo ratings yet

- Economic Outlook Q2 2011Document5 pagesEconomic Outlook Q2 2011Mark PaineNo ratings yet

- EP202306EDocument17 pagesEP202306EHenry J AlvarezNo ratings yet

- Global Real GDP Growth Is Currently Tracking A 3Document18 pagesGlobal Real GDP Growth Is Currently Tracking A 3Mai PhamNo ratings yet

- Global Financial CrisisDocument15 pagesGlobal Financial CrisisAkash JNo ratings yet

- G P P C: Group of TwentyDocument13 pagesG P P C: Group of Twentya10family10No ratings yet

- ForewordDocument3 pagesForeword5gny4dfrqzNo ratings yet

- Directors' Report: I. Economic Backdrop and Banking EnvironmentDocument53 pagesDirectors' Report: I. Economic Backdrop and Banking EnvironmentPuja BhallaNo ratings yet

- Investment Outlook February 2024Document7 pagesInvestment Outlook February 2024byron7cuevaNo ratings yet

- August 2016 Strategy UpdateDocument2 pagesAugust 2016 Strategy UpdateAmin KhakianiNo ratings yet

- The World Economy - 19/03/2010Document3 pagesThe World Economy - 19/03/2010Rhb InvestNo ratings yet

- Global Real Estate Outlook DecDocument6 pagesGlobal Real Estate Outlook Decramachandra rao sambangiNo ratings yet

- Weekly Economic Commentary 06-27-2011Document3 pagesWeekly Economic Commentary 06-27-2011Jeremy A. MillerNo ratings yet

- Indian Economy - Nov 2019Document6 pagesIndian Economy - Nov 2019Rajeshree JadhavNo ratings yet

- Fidelity Perspective Dec2011Document3 pagesFidelity Perspective Dec2011lenovojiNo ratings yet

- Winter 2016Document3 pagesWinter 2016Amin KhakianiNo ratings yet

- Q1 2015 Market Review & Outlook: in BriefDocument3 pagesQ1 2015 Market Review & Outlook: in Briefapi-284581037No ratings yet

- FactorsDocument2 pagesFactorsmaheshabNo ratings yet

- Interim Economic Outlook: Puzzles and UncertaintiesDocument8 pagesInterim Economic Outlook: Puzzles and Uncertaintiesapi-296228558No ratings yet

- Fear of Global Economic RecessionDocument6 pagesFear of Global Economic RecessionT ForsythNo ratings yet

- Nedbank Se Rentekoers-Barometer Vir Mei 2016Document4 pagesNedbank Se Rentekoers-Barometer Vir Mei 2016Netwerk24SakeNo ratings yet

- Investment DecisionsDocument4 pagesInvestment DecisionsDevadutt M.SNo ratings yet

- InfoEdge Annual Report 2023Document1 pageInfoEdge Annual Report 2023Aditya RoyNo ratings yet

- IGWT Report 23 - Nuggets 17 - The Synchronous Bull Market IndicatorDocument29 pagesIGWT Report 23 - Nuggets 17 - The Synchronous Bull Market IndicatorSerigne Modou NDIAYENo ratings yet

- Regionalism V/s Multilateralism: Presented By: Anuratn Purushottam Sunita AroraDocument22 pagesRegionalism V/s Multilateralism: Presented By: Anuratn Purushottam Sunita AroraankycoolNo ratings yet

- Chapter 14 Europe and The WorldDocument10 pagesChapter 14 Europe and The WorlditsisaNo ratings yet

- Kotler Pom17e PPT 12Document47 pagesKotler Pom17e PPT 12solehah sapieNo ratings yet

- Producer Organisations: Chris Penrose-BuckleyDocument201 pagesProducer Organisations: Chris Penrose-BuckleyOxfamNo ratings yet

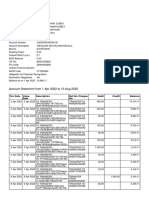

- Your Requested Statement: Statement Date: From Date: To DateDocument8 pagesYour Requested Statement: Statement Date: From Date: To DateOne koeNo ratings yet

- This Study Resource WasDocument8 pagesThis Study Resource WasSNRBTNo ratings yet

- Ijarah: Basic Rules of Ijarah/LeasingDocument6 pagesIjarah: Basic Rules of Ijarah/Leasingali_zain_7No ratings yet

- Group7 MacroeconomicsDocument21 pagesGroup7 MacroeconomicsAashay JainNo ratings yet

- The Customs Value of Imported Goods &: Advance Valuation RulingDocument8 pagesThe Customs Value of Imported Goods &: Advance Valuation RulingYanisa M. OscarNo ratings yet

- Incoterms 2020 Rules Chart of Responsibility: Any Transport Mode Sea/Inland Waterway Transport Any Transport ModeDocument2 pagesIncoterms 2020 Rules Chart of Responsibility: Any Transport Mode Sea/Inland Waterway Transport Any Transport ModeRicardo PirelaNo ratings yet

- Crypto Payments Industry Research ReportDocument55 pagesCrypto Payments Industry Research ReportRodrix DigitalNo ratings yet

- Tissari To ITC and ITTO On World Furniture Markets 22 04 2005 PDFDocument265 pagesTissari To ITC and ITTO On World Furniture Markets 22 04 2005 PDFaneekNo ratings yet

- SMUSA Financial Policies and ProceduresDocument36 pagesSMUSA Financial Policies and ProceduresLiau Cheong ZerNo ratings yet

- Chapter 06 Test BankDocument46 pagesChapter 06 Test BankShaochong WangNo ratings yet

- ECON140-Chapter 25-Measuring Domestic Output and National IncomeDocument18 pagesECON140-Chapter 25-Measuring Domestic Output and National IncomeI GuessNo ratings yet

- Sample Paperpre Board II Acct 2324-2Document10 pagesSample Paperpre Board II Acct 2324-2kanakchauhan206No ratings yet

- Laytime Calculation Geared VesselDocument4 pagesLaytime Calculation Geared Vesselraditya wpNo ratings yet

- Account Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubham TyagiNo ratings yet

- GR 11 Accounting P2 (English) November 2022 Question PaperDocument14 pagesGR 11 Accounting P2 (English) November 2022 Question Paperphafane2020No ratings yet

- Kalyani Technoforge LTD - 301 - 18-10-2021Document1 pageKalyani Technoforge LTD - 301 - 18-10-2021Pragnesh PrajapatiNo ratings yet

- International Economics Exam-1Document5 pagesInternational Economics Exam-1Barış AsaNo ratings yet

- Pharma Erp BrochureDocument8 pagesPharma Erp BrochuresanthoshinouNo ratings yet

- Foreign Policy Concept For 2014-2020Document9 pagesForeign Policy Concept For 2014-2020aidaniumonlineNo ratings yet