You might also like

- Ti Cycle Case StudyDocument11 pagesTi Cycle Case StudyDines ShindeNo ratings yet

- Oreo Case StudyDocument8 pagesOreo Case StudyArpit KapoorNo ratings yet

- Principles of Accounting Vol 2 Managerial Accounting Chapter 3 - Answer KeysDocument4 pagesPrinciples of Accounting Vol 2 Managerial Accounting Chapter 3 - Answer KeysAnonymous MNo ratings yet

- IASP 2016 Poster Abstracts - Wednesday PDFDocument731 pagesIASP 2016 Poster Abstracts - Wednesday PDFHendriik ViicarloNo ratings yet

- Mobile Data AnalysisDocument34 pagesMobile Data AnalysisAswathy Ashokan50% (8)

- Cost-Volume-Profit Analysis: Mcgraw-Hill EducationDocument53 pagesCost-Volume-Profit Analysis: Mcgraw-Hill Educationkindergarten tutorialNo ratings yet

- Business Plan TemplateDocument18 pagesBusiness Plan Templatesusliana silaban100% (3)

- Events Marketing Proposal: Prepared For Willifred IndustriesDocument12 pagesEvents Marketing Proposal: Prepared For Willifred IndustriesKaleigh ForrestNo ratings yet

- Volkswagen of America Final PaperDocument16 pagesVolkswagen of America Final PaperJawadNo ratings yet

- CVP AnalysisDocument36 pagesCVP Analysisghosh71No ratings yet

- Cost-Volume-Profit Analysis: Mcgraw-Hill/IrwinDocument78 pagesCost-Volume-Profit Analysis: Mcgraw-Hill/IrwinSheila Jane Maderse AbraganNo ratings yet

- CVP PPT 1st YrDocument81 pagesCVP PPT 1st YrZachary AstorNo ratings yet

- Hilton 11e Chap007 StudentsDocument38 pagesHilton 11e Chap007 StudentsMelix SianturiNo ratings yet

- IPPTChap 007Document53 pagesIPPTChap 007Khaled BarakatNo ratings yet

- CVP Analysis 08Document52 pagesCVP Analysis 08Maulani DwiNo ratings yet

- Chapter Six Ba 315-Lpc Umsl: (Contribution Margin)Document53 pagesChapter Six Ba 315-Lpc Umsl: (Contribution Margin)NAZHIM KERENNo ratings yet

- MAS Hilton Chap07Document30 pagesMAS Hilton Chap07YahiMicuaVillandaNo ratings yet

- Hilton 11e Chap007PPTDocument53 pagesHilton 11e Chap007PPTNgô Khánh HòaNo ratings yet

- Chap 008Document34 pagesChap 008alishamrozNo ratings yet

- Assignment 02 - SolutionDocument4 pagesAssignment 02 - SolutionSuman Paul ChowdhuryNo ratings yet

- Cost Volume Profit Analysis - Chapter 6Document39 pagesCost Volume Profit Analysis - Chapter 6Maria Maganda MalditaNo ratings yet

- CH 8 Part 2Document15 pagesCH 8 Part 2Hanif QusyairyNo ratings yet

- CVP Relationship Kelompok 3Document42 pagesCVP Relationship Kelompok 3Enrico Jovian S SNo ratings yet

- CVP AnalysisDocument40 pagesCVP Analysissbjafri0No ratings yet

- Answer Key To Test #3 - ACCT-312 - Fall 2019Document8 pagesAnswer Key To Test #3 - ACCT-312 - Fall 2019Amir ContrerasNo ratings yet

- Chap006 CVPDocument57 pagesChap006 CVPaulia eflinaNo ratings yet

- BUACC2614Document6 pagesBUACC2614SanjeevParajuliNo ratings yet

- A181 Bkam3023 Topic 1 - CVP AnalysisDocument64 pagesA181 Bkam3023 Topic 1 - CVP AnalysisJagethiswari RajahNo ratings yet

- CVP Analysis - Jan18Document23 pagesCVP Analysis - Jan18Jobert DiliNo ratings yet

- Chapter 4 CVP AnalysisDocument15 pagesChapter 4 CVP AnalysisMaria Beatriz NavecisNo ratings yet

- Topic 04 - Cost and Management Accounting Course Notes 2021 PWC Conversion ProgrammeDocument84 pagesTopic 04 - Cost and Management Accounting Course Notes 2021 PWC Conversion ProgrammejerrymaNo ratings yet

- Chapter - 8 - Cost-Volume-Profit Analysis - UETDocument19 pagesChapter - 8 - Cost-Volume-Profit Analysis - UETZia UddinNo ratings yet

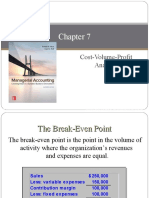

- Equation Method: Sales Variable Expenses + Fixed Expenses + Profits (At The Break-Even Point Profits Equal Zero)Document4 pagesEquation Method: Sales Variable Expenses + Fixed Expenses + Profits (At The Break-Even Point Profits Equal Zero)Aly TerrenalNo ratings yet

- Chapter 9 - CVP AnalysisDocument60 pagesChapter 9 - CVP AnalysisKunal ObhraiNo ratings yet

- Hilton 11e Chap007PPT-STUDocument52 pagesHilton 11e Chap007PPT-STUNgọc ĐỗNo ratings yet

- b4 Biaya Profit VolumeDocument42 pagesb4 Biaya Profit Volumemaria fransiscaNo ratings yet

- b4 Biaya Profit VolumeDocument55 pagesb4 Biaya Profit Volumevi. bluesNo ratings yet

- Cost-Volume-Profit (CVP) Analysis Template: Strictly ConfidentialDocument4 pagesCost-Volume-Profit (CVP) Analysis Template: Strictly Confidentialterhua11100% (1)

- Tutorial 3 AnswersDocument7 pagesTutorial 3 AnswersFEI FEINo ratings yet

- 1415J M - Sesi 07 08 - Akuntansi Manajemen - CVP TDMDocument59 pages1415J M - Sesi 07 08 - Akuntansi Manajemen - CVP TDMAnonymous yMOMM9bs100% (1)

- Break-Even Analysis - Revision.: A Technique To Help Answer Some Key QuestionsDocument18 pagesBreak-Even Analysis - Revision.: A Technique To Help Answer Some Key QuestionsUncle MattNo ratings yet

- Cost Volume Profit PresentasiDocument89 pagesCost Volume Profit Presentasimuhammad raflyNo ratings yet

- CA TM 2nd Edition Chapter 22 EngDocument38 pagesCA TM 2nd Edition Chapter 22 EngIp NicoleNo ratings yet

- Cost-Volume-Profit Relationships: Acc 3202 Management Accounting 2Document88 pagesCost-Volume-Profit Relationships: Acc 3202 Management Accounting 2akuszmylifeNo ratings yet

- Kelompok 1 - CVP Analysis - Akmen (A4)Document20 pagesKelompok 1 - CVP Analysis - Akmen (A4)Yuliana RiskaNo ratings yet

- Chapter 7Document36 pagesChapter 718071052 Nguyễn Thị MaiNo ratings yet

- Practice ManualDocument679 pagesPractice ManualSaikrishna AlluNo ratings yet

- b4 Biaya Profit VolumeDocument42 pagesb4 Biaya Profit VolumedianaNo ratings yet

- Cost-Volume-Profit Analysis RelationshipsDocument95 pagesCost-Volume-Profit Analysis Relationshipsmohamed el kadyNo ratings yet

- Master Budget Formulas Module 6 Management AccountingDocument14 pagesMaster Budget Formulas Module 6 Management AccountingcykablyatNo ratings yet

- Sol ch13Document6 pagesSol ch13Kailash KumarNo ratings yet

- Cost-Volume-Profit Relationships: Chapter SixDocument82 pagesCost-Volume-Profit Relationships: Chapter SixThet MatiasNo ratings yet

- ACN 213 Chapter 3Document84 pagesACN 213 Chapter 3Sakib Ahmed SharilNo ratings yet

- Afrah Azzahira Wismono - 008202000053 - Assignment Week 14Document6 pagesAfrah Azzahira Wismono - 008202000053 - Assignment Week 14Afrah AzzahiraNo ratings yet

- Chap 06 NotesDocument74 pagesChap 06 NotesNancy HineyNo ratings yet

- Cost-Volume-Profit Relationships: Chapter SixDocument70 pagesCost-Volume-Profit Relationships: Chapter SixFadillah AhmadNo ratings yet

- Managerial Accounting 14Th Edition Warren Solutions Manual Full Chapter PDFDocument67 pagesManagerial Accounting 14Th Edition Warren Solutions Manual Full Chapter PDFykydxnjk4100% (9)

- Let's calculate the break-even point for this firm selling multiple productsDocument34 pagesLet's calculate the break-even point for this firm selling multiple productsMuhammad HasanNo ratings yet

- 202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Document11 pages202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Sayhan Hosen Arif100% (1)

- CVP Income StatementDocument2 pagesCVP Income StatementmuayadNo ratings yet

- CVP AnalysisDocument25 pagesCVP AnalysisemonNo ratings yet

- Week 8 (Unit 7) - Tutorial Solutions: Review QuestionDocument10 pagesWeek 8 (Unit 7) - Tutorial Solutions: Review QuestionSheenam SinghNo ratings yet

- Pertemuan 11 Chap007-008 Hilton - EditDocument58 pagesPertemuan 11 Chap007-008 Hilton - Editferly12No ratings yet

- Management Accounting: Dr. Jagriti AroraDocument31 pagesManagement Accounting: Dr. Jagriti AroraMahamNo ratings yet

- IPPTChap 003Document97 pagesIPPTChap 003Rina TruNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Wiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)No ratings yet

- Tugas ORDocument2 pagesTugas ORHendriik ViicarloNo ratings yet

- Dr. Niniet Indah A.: Course: Contemporary Logistics Graduate ProgrammeDocument3 pagesDr. Niniet Indah A.: Course: Contemporary Logistics Graduate ProgrammeHendriik ViicarloNo ratings yet

- Models For The Layout ProblemDocument26 pagesModels For The Layout ProblemHendriik ViicarloNo ratings yet

- Analisis Risiko Pada Proyek Pembangunan Parkir Basement Jalan Sulawesi DenpasarDocument11 pagesAnalisis Risiko Pada Proyek Pembangunan Parkir Basement Jalan Sulawesi DenpasarLi BertNo ratings yet

- Pembangkit Listrik Tenaga UapDocument12 pagesPembangkit Listrik Tenaga UapHendriik ViicarloNo ratings yet

- Chap005 PDFDocument63 pagesChap005 PDFTrần Gia LinhNo ratings yet

- ORL - Tugas 5 - 32003Document4 pagesORL - Tugas 5 - 32003Hendriik ViicarloNo ratings yet

- ORL - Tugas 5 - 32003Document1 pageORL - Tugas 5 - 32003Hendriik ViicarloNo ratings yet

- PLTUDocument44 pagesPLTUMarsha ButlerNo ratings yet

- Chap005 PDFDocument63 pagesChap005 PDFTrần Gia LinhNo ratings yet

- IaspDocument5 pagesIaspHendriik ViicarloNo ratings yet

- Business Objectives and Key Concepts in Information Systems QuizDocument15 pagesBusiness Objectives and Key Concepts in Information Systems QuizNalin KannangaraNo ratings yet

- Walmart StrategyDocument14 pagesWalmart Strategyclassmate100% (4)

- Assignment MKTDocument36 pagesAssignment MKTsyaaismail100% (2)

- ch04 (1) ThompsonDocument16 pagesch04 (1) ThompsonAminul Islam AmuNo ratings yet

- Nestle Maggi: Submitted By: Pavan S GhodkeDocument19 pagesNestle Maggi: Submitted By: Pavan S GhodkeSanthosh K KolekarNo ratings yet

- Bem102 7Document22 pagesBem102 7Mellisa AndileNo ratings yet

- Substitue (Biyan)Document3 pagesSubstitue (Biyan)AbiyanSatrioPNo ratings yet

- Course Code and Title: Lesson Number: Topic: Role of The Relationship Manager ProfessorDocument8 pagesCourse Code and Title: Lesson Number: Topic: Role of The Relationship Manager ProfessorJha Jha CaLvezNo ratings yet

- Project report on SWOT analysis of Pepsi CoDocument29 pagesProject report on SWOT analysis of Pepsi CoRitika KhuranaNo ratings yet

- Online Buying Behavior of Kasiglahan Village StudentsDocument2 pagesOnline Buying Behavior of Kasiglahan Village StudentsCarmela Kristine JordaNo ratings yet

- India Telecom Industry InsightsDocument46 pagesIndia Telecom Industry InsightsJayant LoharNo ratings yet

- Kellogg's Marketing Mistakes in India and How to SucceedDocument4 pagesKellogg's Marketing Mistakes in India and How to SucceedKattaSiddharthaNo ratings yet

- ITC Team Market Analysis Aashirvaad Atta CompetitorsDocument19 pagesITC Team Market Analysis Aashirvaad Atta CompetitorsAkshit Gangwal50% (2)

- PM Y2group3 PDF FreeDocument5 pagesPM Y2group3 PDF FreeGroup ShareNo ratings yet

- VML Commerce The B2B Future Shopper Report 2023Document77 pagesVML Commerce The B2B Future Shopper Report 2023mkckq5jhhqNo ratings yet

- PM7e PindyckRubinfeld Microeconomics Ch12ab - Az.ch12Document35 pagesPM7e PindyckRubinfeld Microeconomics Ch12ab - Az.ch12Wisnu Fajar Baskoro100% (1)

- Chapter 14 Firms in Competitive Markets 08042021 075713pmDocument18 pagesChapter 14 Firms in Competitive Markets 08042021 075713pmHasnain GoharNo ratings yet

- Entrepreneurship & Engineering Management 18 - Mechanical EngineeringDocument20 pagesEntrepreneurship & Engineering Management 18 - Mechanical EngineeringSaFdaR QaZiNo ratings yet

- Andrew Ongso 03011180055 18M1 QUIZDocument4 pagesAndrew Ongso 03011180055 18M1 QUIZAndrew OngsoNo ratings yet

- Consumer Attitu-WPS OfficebDocument13 pagesConsumer Attitu-WPS OfficebPrince AjNo ratings yet

- E-Commerce & E-Business Guide to E-Commerce, E-Business Models, Data Warehousing & MiningDocument13 pagesE-Commerce & E-Business Guide to E-Commerce, E-Business Models, Data Warehousing & MiningHussainNo ratings yet

- CIMA 2010 Qualification Structure and SyllabusDocument80 pagesCIMA 2010 Qualification Structure and SyllabusMuhammad AshrafNo ratings yet

- CleverAds ProfileDocument12 pagesCleverAds ProfileMaiBachNo ratings yet

- Consumer-Oriented E-Commerce: Key Differences and Success FactorsDocument23 pagesConsumer-Oriented E-Commerce: Key Differences and Success FactorsABHISHEK BNo ratings yet