You might also like

- Risk RegisterDocument8 pagesRisk Registershafaat_nedian0% (1)

- Managing Project Risks (2021 Update) - 042340Document11 pagesManaging Project Risks (2021 Update) - 042340Joseph Kwafo MensahNo ratings yet

- Risk Management: Reported By: Darroca, John Rolde Augustine G. Deraper, Rachelle Mae Felismino, Mary R. Patoc, NinoDocument31 pagesRisk Management: Reported By: Darroca, John Rolde Augustine G. Deraper, Rachelle Mae Felismino, Mary R. Patoc, NinoMary FelisminoNo ratings yet

- Risk Management in ProjectsDocument22 pagesRisk Management in Projectscandystick8950% (2)

- 15 Best Practices For Effective Project Risk ManagementDocument9 pages15 Best Practices For Effective Project Risk ManagementAnonymous Xb3zHioNo ratings yet

- X SamplesDocument26 pagesX SamplesBhavish RamroopNo ratings yet

- Giao trinh riskDocument3 pagesGiao trinh riskNguyễn Ngọc QuỳnhNo ratings yet

- Spec 2 A1 Tierra MoniqueDocument8 pagesSpec 2 A1 Tierra MoniqueMonique TierraNo ratings yet

- Assessment 3 - Script in Word FormatDocument4 pagesAssessment 3 - Script in Word FormatVladimir BloodymirNo ratings yet

- Pm652 Lm6 NotesDocument5 pagesPm652 Lm6 NotesNatasha ReavesNo ratings yet

- Construction Risk ManagementDocument4 pagesConstruction Risk ManagementNeeleshSoganiNo ratings yet

- RiskDocument4 pagesRiskadylanNo ratings yet

- Research Paper On Project Risk ManagementDocument5 pagesResearch Paper On Project Risk Managementlemvhlrif100% (1)

- 10 Golden Rules of Project Risk ManagementDocument5 pages10 Golden Rules of Project Risk ManagementNitin GuptaNo ratings yet

- Answer 1: IntroductionDocument9 pagesAnswer 1: IntroductionAman SharmaNo ratings yet

- Project Risk Management: 10 Rules for Managing Project RiskDocument3 pagesProject Risk Management: 10 Rules for Managing Project RiskMary FelisminoNo ratings yet

- Risk Is Defined As Any Uncertain Event Management EssayDocument5 pagesRisk Is Defined As Any Uncertain Event Management EssayHND Assignment HelpNo ratings yet

- Business Planning and Project Management: Faculty Name: Ms. Supriya KamaleDocument21 pagesBusiness Planning and Project Management: Faculty Name: Ms. Supriya KamaleTaha MerchantNo ratings yet

- Risk Analysis & Assessment in Nigerian Banks IIDocument16 pagesRisk Analysis & Assessment in Nigerian Banks IIShowman4100% (1)

- Group 8 Risk ManagementDocument22 pagesGroup 8 Risk ManagementStephen OlufekoNo ratings yet

- Project Risk ManagementDocument15 pagesProject Risk ManagementEng abdifatah saidNo ratings yet

- Risk Management Research Paper OutlineDocument4 pagesRisk Management Research Paper Outlineofahxdcnd100% (1)

- Chapter 5Document23 pagesChapter 5mdhillonhasnain1122No ratings yet

- Chapter One The Concept of Project RiskDocument10 pagesChapter One The Concept of Project RiskBelay Tadesse100% (1)

- Project Risk Management Identification and ExposureDocument24 pagesProject Risk Management Identification and ExposureARUNGREESMANo ratings yet

- Steps On Risk Management PlanDocument14 pagesSteps On Risk Management PlanEdgard Laurenz Montellano GeronimoNo ratings yet

- Project Risk Management Term PaperDocument5 pagesProject Risk Management Term Paperafmzeracmdvbfe100% (1)

- FME Project RiskDocument39 pagesFME Project RiskAndika WibowoNo ratings yet

- Project Scope Management: Syllabus For Chapter 4Document10 pagesProject Scope Management: Syllabus For Chapter 4rehan44No ratings yet

- What Is Risk MGTDocument6 pagesWhat Is Risk MGTخصفيانNo ratings yet

- Risk AssignmentDocument53 pagesRisk AssignmentNafiz ImtiazNo ratings yet

- Project Risk Management PHD ThesisDocument4 pagesProject Risk Management PHD Thesisfjdqvrcy100% (2)

- Importance of Risk Management in Project ManagementDocument4 pagesImportance of Risk Management in Project ManagementAman JainNo ratings yet

- Chapter 2 - Looking at Projects RISKDocument22 pagesChapter 2 - Looking at Projects RISKErmia MogeNo ratings yet

- Azerbaijan State University of EconomicsDocument15 pagesAzerbaijan State University of EconomicsAnar hummatovNo ratings yet

- Risk Management Part 1Document6 pagesRisk Management Part 1Isay Guazon AbelardoNo ratings yet

- Rule 1: Make Risk Management Part of Your ProjectDocument4 pagesRule 1: Make Risk Management Part of Your ProjectAneuxAgamNo ratings yet

- 10 Golden Rules of Project Risk ManagementDocument10 pages10 Golden Rules of Project Risk ManagementVinodPotphodeNo ratings yet

- Copie de Risk Management Professional Training LPCDocument40 pagesCopie de Risk Management Professional Training LPCjunby.dubNo ratings yet

- Identifying RiskDocument14 pagesIdentifying RiskDennis MokNo ratings yet

- Fundamentals of Risk Management: Enterprise X, AZ 85016 CM, Inc.:: 2415 E. Camelback Road.:: Suite 700:: PhoeniDocument4 pagesFundamentals of Risk Management: Enterprise X, AZ 85016 CM, Inc.:: 2415 E. Camelback Road.:: Suite 700:: PhoeniJulio VargasNo ratings yet

- 10 Rules of PRMDocument9 pages10 Rules of PRMNicolae CojusneanuNo ratings yet

- Universal Human Values and Professional Ethics MCQDocument27 pagesUniversal Human Values and Professional Ethics MCQShruti NigamNo ratings yet

- 4.5 PresentationDocument13 pages4.5 PresentationHajar SadikiNo ratings yet

- 10 Golden Rules of Project Risk ManagementDocument12 pages10 Golden Rules of Project Risk Managementrelupandit100% (1)

- Project risk plan analysisDocument13 pagesProject risk plan analysisMOHAMED SLIMANINo ratings yet

- Research Paper of Risk ManagementDocument4 pagesResearch Paper of Risk Managementtgkeqsbnd100% (1)

- MGT 10 ReportDocument25 pagesMGT 10 ReportVESENTH MAY RUBINOSNo ratings yet

- Lecture-6 RiskDocument51 pagesLecture-6 RiskZafar Farooq100% (2)

- Part 6 Risk AnalysisDocument24 pagesPart 6 Risk Analysissamrawit aysheshimNo ratings yet

- Risk Management PDFDocument10 pagesRisk Management PDFAlok Raj100% (1)

- Project Risk Management Research PapersDocument5 pagesProject Risk Management Research Papersaypewibkf100% (1)

- Agribusiness Project Risk ManagementDocument82 pagesAgribusiness Project Risk ManagementNinuca ChanturiaNo ratings yet

- Thesis Topics Risk ManagementDocument4 pagesThesis Topics Risk Managementbshpab74100% (2)

- Lec # 09 Construction ManagementDocument17 pagesLec # 09 Construction ManagementNoor Uddin ZangiNo ratings yet

- Unit 4 NotesDocument24 pagesUnit 4 Notessushant mohodNo ratings yet

- Risk CategoriesDocument10 pagesRisk CategoriesJon TkelNo ratings yet

- Project Risk Management Dissertation TopicsDocument8 pagesProject Risk Management Dissertation TopicsBuyWritingPaperCanada100% (1)

- Name:-Gifta Jebakani J Reg - No. 16MCA0017Document6 pagesName:-Gifta Jebakani J Reg - No. 16MCA0017ANUPAM SURNo ratings yet

- Poverty RateDocument2 pagesPoverty RateJudy Ann CerenadoNo ratings yet

- State Universities and Colleges Faculty-Student Ratio by RegionDocument4 pagesState Universities and Colleges Faculty-Student Ratio by RegionWestCentralDumagueteNo ratings yet

- 14 Chapter 14 Vigorously Advancing Science Technology and Innovation 1.14.2019Document3 pages14 Chapter 14 Vigorously Advancing Science Technology and Innovation 1.14.2019John Mathew Alday BrionesNo ratings yet

- Final Exam CE421 PDFDocument3 pagesFinal Exam CE421 PDFJohn Mathew Alday BrionesNo ratings yet

- Higher Education Graduates by Discipline from 2008-2018Document1 pageHigher Education Graduates by Discipline from 2008-2018John Mathew Alday BrionesNo ratings yet

- Business ModelDocument4 pagesBusiness ModelJohn Mathew Alday BrionesNo ratings yet

- S 3Document1 pageS 3John Mathew Alday BrionesNo ratings yet

- Republic of The PhilippinesDocument2 pagesRepublic of The PhilippinesJohn Mathew Alday BrionesNo ratings yet

- Table 5A. List of Autonomous Higher Education InstitutionsDocument4 pagesTable 5A. List of Autonomous Higher Education InstitutionsJohn Mathew Alday BrionesNo ratings yet

- DocumentDocument4 pagesDocumentJohn Mathew Alday BrionesNo ratings yet

- Online PaperDocument7 pagesOnline PaperJohn Mathew Alday BrionesNo ratings yet

- Table of ContentsDocument8 pagesTable of ContentsJohn Mathew Alday BrionesNo ratings yet

- Rules of ProcedureDocument2 pagesRules of ProcedureDerly ObtialNo ratings yet

- Lecture 3 PDFDocument20 pagesLecture 3 PDFJohn Mathew Alday BrionesNo ratings yet

- VEHICLE CLASSIFICATION: MS18 LoadingDocument78 pagesVEHICLE CLASSIFICATION: MS18 LoadingJohn Mathew Alday BrionesNo ratings yet

- Civil & Sanitary Engineering Department: Engr. Edwin D. AbrigondaDocument2 pagesCivil & Sanitary Engineering Department: Engr. Edwin D. AbrigondaJohn Mathew Alday BrionesNo ratings yet

- PaperDocument5 pagesPaperJohn Mathew Alday BrionesNo ratings yet

- WerDocument2 pagesWerJohn Mathew Alday BrionesNo ratings yet

- Identifying Risks and AddressingDocument5 pagesIdentifying Risks and AddressingJohn Mathew Alday BrionesNo ratings yet

- AkweDocument1 pageAkweJohn Mathew Alday BrionesNo ratings yet

- CC CDPlan 2017 - 2019 PDFDocument127 pagesCC CDPlan 2017 - 2019 PDFMariz PorlayNo ratings yet

- Design of One - Way Slab (S-1)Document5 pagesDesign of One - Way Slab (S-1)John Mathew Alday BrionesNo ratings yet

- PICE Amended by LawsDocument21 pagesPICE Amended by Lawsalden cayagaNo ratings yet

- How Globalized is Your Home? Activity #1Document1 pageHow Globalized is Your Home? Activity #1John Mathew Alday BrionesNo ratings yet

- EstimateDocument49 pagesEstimateJohn Mathew Alday BrionesNo ratings yet

- Design of One - Way Slab (S-1)Document5 pagesDesign of One - Way Slab (S-1)John Mathew Alday BrionesNo ratings yet

- PICE Amended by Laws 1Document1 pagePICE Amended by Laws 1John Mathew Alday BrionesNo ratings yet

- Chapter II-BrionesDocument14 pagesChapter II-BrionesJohn Mathew Alday BrionesNo ratings yet

- Urban Transport IssuesDocument3 pagesUrban Transport IssuesJohn Mathew Alday BrionesNo ratings yet

- Job Insecurity and GlobalizationDocument5 pagesJob Insecurity and GlobalizationJayboy SARTORIONo ratings yet

- Community Based Tourism Development in SikkimDocument28 pagesCommunity Based Tourism Development in SikkimAysha NargeezNo ratings yet

- Summary SIA Ch.13 - Expenditure CycleDocument3 pagesSummary SIA Ch.13 - Expenditure CycleAthiyya Nabila AyuNo ratings yet

- Attachmentsresources90316 101442 Advance Accounting Nov. 2008 PDFDocument25 pagesAttachmentsresources90316 101442 Advance Accounting Nov. 2008 PDFDipen AdhikariNo ratings yet

- Japan Since 1980Document330 pagesJapan Since 1980JianBre100% (3)

- Knowledge Managment BiaDocument18 pagesKnowledge Managment BiaAbhinav PandeyNo ratings yet

- Unit - III Labour CostDocument38 pagesUnit - III Labour CosttheriyathuNo ratings yet

- Rahmatina Awaliah KasriDocument21 pagesRahmatina Awaliah Kasrijaharuddin.hannoverNo ratings yet

- Chapter 09. Ch09 P18 Build A Model: Cost of DebtDocument2 pagesChapter 09. Ch09 P18 Build A Model: Cost of Debtk3jooo كيجوووNo ratings yet

- Report of Collections and DepositsDocument3 pagesReport of Collections and DepositsReign Hernandez100% (1)

- RaymondDocument12 pagesRaymondCharu SharmaNo ratings yet

- Logbook Gac022Document6 pagesLogbook Gac022PaulinaNo ratings yet

- Reliance Industries' Naphtha Swap DealDocument4 pagesReliance Industries' Naphtha Swap DealPrabha ArunNo ratings yet

- Final Report - Draft - Feasibility RPLDocument76 pagesFinal Report - Draft - Feasibility RPLmajaliwaally100% (1)

- LOG MM 005 PresentationDocument73 pagesLOG MM 005 Presentationaler1984No ratings yet

- Chapter Two - Types of Information SystemsDocument20 pagesChapter Two - Types of Information SystemsMary KalukiNo ratings yet

- COVID-19 and Its Impact On The Indian EconomyDocument17 pagesCOVID-19 and Its Impact On The Indian Economyuday xeroxNo ratings yet

- Internet Marketing Plan GuideDocument5 pagesInternet Marketing Plan GuideMario MitevskiNo ratings yet

- PAS 1 - Presentation of Financial Statements-1Document24 pagesPAS 1 - Presentation of Financial Statements-1Krizzia DizonNo ratings yet

- Name: Safira Yafiq Khairani NIM: 1802112130 Review Question Chapter 16Document9 pagesName: Safira Yafiq Khairani NIM: 1802112130 Review Question Chapter 16Safira KhairaniNo ratings yet

- Transfer ConfirmationDocument3 pagesTransfer Confirmationme NaderNo ratings yet

- Demonetisation The Nielsen ViewDocument4 pagesDemonetisation The Nielsen ViewShriram SNo ratings yet

- STFC X15Document7 pagesSTFC X15Kajol Keshri100% (1)

- AssignmentDocument4 pagesAssignmentShariq EjazNo ratings yet

- Mutasem Amr 16402752 - Operations MGMT - Ass2 - April 7Document13 pagesMutasem Amr 16402752 - Operations MGMT - Ass2 - April 7Mutasem AmrNo ratings yet

- SMChap 004Document49 pagesSMChap 004Rola KhouryNo ratings yet

- CAF 1 SupplementsDocument36 pagesCAF 1 SupplementsAb WasayNo ratings yet

- Vidhey Patel ResumeDocument2 pagesVidhey Patel ResumeadelaideglxNo ratings yet

- Maternal and Child Nutrition 3: SeriesDocument16 pagesMaternal and Child Nutrition 3: Seriesank2715No ratings yet

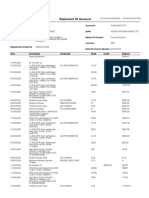

- 'Account StatementDocument11 pages'Account StatementSikander Qazi100% (2)

- Nutritional and Therapeutic Interventions for Diabetes and Metabolic SyndromeFrom EverandNutritional and Therapeutic Interventions for Diabetes and Metabolic SyndromeNo ratings yet

- Functional Safety from Scratch: A Practical Guide to Process Industry ApplicationsFrom EverandFunctional Safety from Scratch: A Practical Guide to Process Industry ApplicationsNo ratings yet

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- A Poison Like No Other: How Microplastics Corrupted Our Planet and Our BodiesFrom EverandA Poison Like No Other: How Microplastics Corrupted Our Planet and Our BodiesRating: 5 out of 5 stars5/5 (1)

- Artificial Intelligence Revolution: How AI Will Change our Society, Economy, and CultureFrom EverandArtificial Intelligence Revolution: How AI Will Change our Society, Economy, and CultureRating: 4.5 out of 5 stars4.5/5 (2)

- A Complete Guide to Safety Officer Interview Questions and AnswersFrom EverandA Complete Guide to Safety Officer Interview Questions and AnswersRating: 4 out of 5 stars4/5 (1)

- The ISO 45001:2018 Implementation Handbook: Guidance on Building an Occupational Health and Safety Management SystemFrom EverandThe ISO 45001:2018 Implementation Handbook: Guidance on Building an Occupational Health and Safety Management SystemNo ratings yet

- Guidelines for Auditing Process Safety Management SystemsFrom EverandGuidelines for Auditing Process Safety Management SystemsNo ratings yet

- Nir Eyal's Hooked: Proven Strategies for Getting Up to Speed Faster and Smarter SummaryFrom EverandNir Eyal's Hooked: Proven Strategies for Getting Up to Speed Faster and Smarter SummaryRating: 4 out of 5 stars4/5 (5)

- The User's Journey: Storymapping Products That People LoveFrom EverandThe User's Journey: Storymapping Products That People LoveRating: 3.5 out of 5 stars3.5/5 (8)

- Introduction to Petroleum Process SafetyFrom EverandIntroduction to Petroleum Process SafetyRating: 3 out of 5 stars3/5 (2)

- Trevor Kletz Compendium: His Process Safety Wisdom Updated for a New GenerationFrom EverandTrevor Kletz Compendium: His Process Safety Wisdom Updated for a New GenerationNo ratings yet

- Practical Troubleshooting of Electrical Equipment and Control CircuitsFrom EverandPractical Troubleshooting of Electrical Equipment and Control CircuitsRating: 4 out of 5 stars4/5 (5)

- Guidelines for Initiating Events and Independent Protection Layers in Layer of Protection AnalysisFrom EverandGuidelines for Initiating Events and Independent Protection Layers in Layer of Protection AnalysisRating: 5 out of 5 stars5/5 (1)

- Understanding Automotive Electronics: An Engineering PerspectiveFrom EverandUnderstanding Automotive Electronics: An Engineering PerspectiveRating: 3.5 out of 5 stars3.5/5 (16)

- Delft Design Guide -Revised edition: Perspectives- Models - Approaches - MethodsFrom EverandDelft Design Guide -Revised edition: Perspectives- Models - Approaches - MethodsNo ratings yet

- The Maker's Field Guide: The Art & Science of Making Anything ImaginableFrom EverandThe Maker's Field Guide: The Art & Science of Making Anything ImaginableNo ratings yet

- Design Is The Problem: The Future of Design Must Be SustainableFrom EverandDesign Is The Problem: The Future of Design Must Be SustainableRating: 1.5 out of 5 stars1.5/5 (2)

- 507 Mechanical Movements: Mechanisms and DevicesFrom Everand507 Mechanical Movements: Mechanisms and DevicesRating: 4 out of 5 stars4/5 (28)

- Design for How People Think: Using Brain Science to Build Better ProductsFrom EverandDesign for How People Think: Using Brain Science to Build Better ProductsRating: 4 out of 5 stars4/5 (8)

- Incidents That Define Process SafetyFrom EverandIncidents That Define Process SafetyNo ratings yet

- Practical Industrial Safety, Risk Assessment and Shutdown SystemsFrom EverandPractical Industrial Safety, Risk Assessment and Shutdown SystemsRating: 4 out of 5 stars4/5 (11)