You might also like

- B. Com I All PapersnDocument14 pagesB. Com I All Papersnrahim Abbas aliNo ratings yet

- Institute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartDocument3 pagesInstitute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartSafi SheikhNo ratings yet

- Topper 2 101 504 549 Accountancy Question Up201801231745 1516709744 8573Document15 pagesTopper 2 101 504 549 Accountancy Question Up201801231745 1516709744 8573gauravNo ratings yet

- FND Partnership QuestionDocument3 pagesFND Partnership QuestionShweta BhadauriaNo ratings yet

- Financial Accounting Paper1.1Document20 pagesFinancial Accounting Paper1.1MahediNo ratings yet

- 12 Accountancy t2 sp10Document21 pages12 Accountancy t2 sp1015. FutureNo ratings yet

- Acc311 2021Document4 pagesAcc311 2021hoghidan1No ratings yet

- Chartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalDocument81 pagesChartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalPrashant Sagar GautamNo ratings yet

- RTP Dec 2020 QnsDocument13 pagesRTP Dec 2020 QnsbinuNo ratings yet

- Financial Accounting 2019Document8 pagesFinancial Accounting 2019Ivy NinjaNo ratings yet

- Questions On AccountancyDocument34 pagesQuestions On AccountancyAshwin ChoudharyNo ratings yet

- RTP May 2018 New Gr1Document122 pagesRTP May 2018 New Gr1subhanvts7781No ratings yet

- 201.AFA IP.L II December 2020Document4 pages201.AFA IP.L II December 2020leyaketjnuNo ratings yet

- CFS - ProblemsDocument5 pagesCFS - Problemskatasani likhithNo ratings yet

- Partnership 1Document7 pagesPartnership 1asamoahfredrica5No ratings yet

- Group Assignment OneDocument2 pagesGroup Assignment Oneehitemariam berhanu100% (2)

- Sem3 14 Bcom Hons Sem-3 Financial Accounting II CC 3.1ch - 1201Document5 pagesSem3 14 Bcom Hons Sem-3 Financial Accounting II CC 3.1ch - 1201ruPAM DeyNo ratings yet

- Assignment QuestionsDocument3 pagesAssignment QuestionsKARTIK CHADHANo ratings yet

- Corporate Accounting Ii-1Document4 pagesCorporate Accounting Ii-1ARAVIND V KNo ratings yet

- Syjc - B. K. - Prelim Exam No. 7Document4 pagesSyjc - B. K. - Prelim Exam No. 7karkeraadiyaNo ratings yet

- 1st Semi Prelium Chp. 1, 3, 4, 5, 6 (40 Marks) Dt. 07.12.2020 (All Branch)Document3 pages1st Semi Prelium Chp. 1, 3, 4, 5, 6 (40 Marks) Dt. 07.12.2020 (All Branch)Arthur ShelbyNo ratings yet

- FDN J22 - TS 2 - P1 Account - QueDocument5 pagesFDN J22 - TS 2 - P1 Account - QueShantanu JadhavNo ratings yet

- Paper 1Document19 pagesPaper 1GianNo ratings yet

- Bcom 3 Sem Corporate Accounting 1 19102078 Oct 2019Document5 pagesBcom 3 Sem Corporate Accounting 1 19102078 Oct 2019xyxx1221No ratings yet

- 2accounting Questions Nov Dec 2019 CL PDFDocument3 pages2accounting Questions Nov Dec 2019 CL PDFRazib Das RaazNo ratings yet

- Financial Management - II CA QPDocument4 pagesFinancial Management - II CA QPSivaramkrishna KasilingamNo ratings yet

- CBSE Class 12 Accountancy Accounting For Partnership Firms Sure Shot QuestionsDocument6 pagesCBSE Class 12 Accountancy Accounting For Partnership Firms Sure Shot Questionsdakshrwt06No ratings yet

- Account - 1Document6 pagesAccount - 1kakajumaNo ratings yet

- Zimbabwe School Examinations Council: General Certificate of Education Advanced Level 6001/3Document7 pagesZimbabwe School Examinations Council: General Certificate of Education Advanced Level 6001/3chauromweaNo ratings yet

- Board Paper 2018Document14 pagesBoard Paper 2018zaraniyaz14No ratings yet

- 1Document5 pages1firoozdasmanNo ratings yet

- Xi Annual NewDocument5 pagesXi Annual NewPragadeshwar KarthikeyanNo ratings yet

- This Study Resource Was: Tutorial 6Document4 pagesThis Study Resource Was: Tutorial 6Nicole CapundanNo ratings yet

- CA Inter Adv. Accounting Top 50 Question May 2021Document117 pagesCA Inter Adv. Accounting Top 50 Question May 2021Sumitra yadavNo ratings yet

- Accounting Problems With SolutionsDocument63 pagesAccounting Problems With Solutionssumit_sagar69% (13)

- Admission WorksheetDocument9 pagesAdmission WorksheetShristi BishtNo ratings yet

- Accrual & Prepaid HW QDocument4 pagesAccrual & Prepaid HW Q小仙女哈哈哈No ratings yet

- Ent 2-2Document4 pagesEnt 2-2danielzashleybobNo ratings yet

- Worksheet - Retirement & DissolutionDocument4 pagesWorksheet - Retirement & DissolutionYogesh AdhikariNo ratings yet

- 2020 FA L4 To L10 StudentsDocument40 pages2020 FA L4 To L10 Students徐恺民No ratings yet

- Xi Accounting Set 3Document6 pagesXi Accounting Set 3aashirwad2076No ratings yet

- Test Series: April, 2022 Mock Test Paper 2 Intermediate: Group - I Paper - 1: AccountingDocument7 pagesTest Series: April, 2022 Mock Test Paper 2 Intermediate: Group - I Paper - 1: AccountingVishal MehraNo ratings yet

- Fragment M 11Document7 pagesFragment M 11sm munNo ratings yet

- Goodwill QuestionsDocument7 pagesGoodwill QuestionsTanisha JainNo ratings yet

- Account - 2Document6 pagesAccount - 2kakajumaNo ratings yet

- PartnershipDocument10 pagesPartnershipOm JainNo ratings yet

- 640 / 240 / 260: Advanced Financial Accounting (New Regulations)Document7 pages640 / 240 / 260: Advanced Financial Accounting (New Regulations)Emind Annamalai JPNagarNo ratings yet

- Financial Accounting Question BankDocument10 pagesFinancial Accounting Question BankLAKSHMIKANTH.B MEC-AP/MCNo ratings yet

- Contentitemfile Clakzwt9mx9sk0a212lma0ytv PDFDocument4 pagesContentitemfile Clakzwt9mx9sk0a212lma0ytv PDFJoseph OndariNo ratings yet

- Ty Baf TaxationDocument4 pagesTy Baf TaxationAkki GalaNo ratings yet

- Ty Baf TaxationDocument4 pagesTy Baf TaxationAkki GalaNo ratings yet

- CHP 6 Partnership Exercise 1-4Document5 pagesCHP 6 Partnership Exercise 1-4jasongojinkai2007No ratings yet

- Accounting Assignment 04A 207Document10 pagesAccounting Assignment 04A 207Aniyah's RanticsNo ratings yet

- ACC 281 SEMINAR QUESTIONS Version 2Document8 pagesACC 281 SEMINAR QUESTIONS Version 2Joel SimonNo ratings yet

- MTP1 May2022 - Paper 5 Advanced AccountingDocument24 pagesMTP1 May2022 - Paper 5 Advanced AccountingYash YashwantNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- Dissertation Project of FinanceDocument7 pagesDissertation Project of FinanceWriteMyBiologyPaperGlendale100% (1)

- Acctg 321 A and B - Quiz - PPE - CSDocument5 pagesAcctg 321 A and B - Quiz - PPE - CSGet BurnNo ratings yet

- Berkshire Hathaway 2014Document15 pagesBerkshire Hathaway 2014Vik SinghNo ratings yet

- AAT AVBK AnswersDocument3 pagesAAT AVBK AnswersShailendra KelaniNo ratings yet

- Fsy Tutorial 5Document4 pagesFsy Tutorial 5TACN-4TC-19ACN Nguyen Thu HienNo ratings yet

- Chapter 4 - Fundamentals of Corporate Finance 9th Edition - Test BankDocument26 pagesChapter 4 - Fundamentals of Corporate Finance 9th Edition - Test BankKellyGibbons100% (2)

- Withholding VAT Guideline (2017-18)Document29 pagesWithholding VAT Guideline (2017-18)banglauserNo ratings yet

- Chapter Eight: Functional and Activity-Based BudgetingDocument43 pagesChapter Eight: Functional and Activity-Based BudgetingRecki SeptiandaNo ratings yet

- Unit 1 Corporate LiquidationDocument2 pagesUnit 1 Corporate LiquidationAndrea BreisNo ratings yet

- Ias 20, 23, 40 Practice Questions-1Document4 pagesIas 20, 23, 40 Practice Questions-1Ivy NjorogeNo ratings yet

- Training ReportDocument61 pagesTraining ReportMonu GoyatNo ratings yet

- Conceptual Famework FASB IASBDocument36 pagesConceptual Famework FASB IASBMusab AhmedNo ratings yet

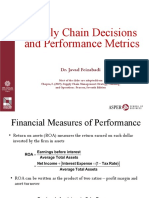

- 3-Supply Chain Decisions and Performance Metrics (A)Document21 pages3-Supply Chain Decisions and Performance Metrics (A)eeman kNo ratings yet

- - Huỳnh Thị Thiên Nhi: Câu HỏiDocument9 pages- Huỳnh Thị Thiên Nhi: Câu HỏiBông GấuNo ratings yet

- April 2006Document8 pagesApril 2006Mohd HafizNo ratings yet

- Pcab LlimDocument634 pagesPcab LlimPankaj RaneNo ratings yet

- Error DiscussionDocument2 pagesError DiscussionGloria Beltran100% (1)

- Shares: Prepared By: R.AnbalaganDocument10 pagesShares: Prepared By: R.AnbalaganKishan SinghNo ratings yet

- Mutual Fund Type of Fund Inception Date Nav/Unit 1 Month YTD 1 Year 2 Years 3 Years 5 Years 10 Years Since InceptionDocument1 pageMutual Fund Type of Fund Inception Date Nav/Unit 1 Month YTD 1 Year 2 Years 3 Years 5 Years 10 Years Since Inceptionlpm_smiNo ratings yet

- Indian Accounting Standards An Overview (Revised 2019)Document15 pagesIndian Accounting Standards An Overview (Revised 2019)Pooja GuptaNo ratings yet

- Chapter 15 M&A, Takeovers, Corporate Control5Document22 pagesChapter 15 M&A, Takeovers, Corporate Control5toshiba1234No ratings yet

- Textbook Materials - ch11Document47 pagesTextbook Materials - ch11OZZYMANNo ratings yet

- 2023 PP Topik 2 FirmaDocument1 page2023 PP Topik 2 FirmaRLin MeeNo ratings yet

- BINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Document5 pagesBINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )johanes ongoNo ratings yet

- F2 - Mock - QDocument14 pagesF2 - Mock - Qjekiyas228No ratings yet

- Statement of Comprehensive Income Part 2Document8 pagesStatement of Comprehensive Income Part 2AG VenturesNo ratings yet

- Acova Radiateurs SolutionDocument14 pagesAcova Radiateurs SolutionSarvagya Jha100% (1)

- 1 Anand, Anurag, AtulDocument8 pages1 Anand, Anurag, AtulIsha KatiyarNo ratings yet

- My Watchlist - Value ResearchDocument1 pageMy Watchlist - Value ResearchpksNo ratings yet

- Jawaban P5-1Document3 pagesJawaban P5-1Nadillah LeicaNo ratings yet