You might also like

- Project Report On Cement IndustryDocument25 pagesProject Report On Cement IndustryKripal Rathore67% (6)

- Report and Swot Analysis On Cement IndustryDocument23 pagesReport and Swot Analysis On Cement IndustryAhmed Raza Jafri50% (4)

- Cement Industry SWOT AnalysisDocument3 pagesCement Industry SWOT Analysispradeepab100% (2)

- Ratio Analysis of Fauji Cement and Lucky CementDocument46 pagesRatio Analysis of Fauji Cement and Lucky Cementsidra_ali82% (22)

- FESCO Online Consumer BillDocument2 pagesFESCO Online Consumer BillYasir Ayub67% (9)

- Stuvia 695663 Silke Prescribed Book .Document1,177 pagesStuvia 695663 Silke Prescribed Book .ConradeNo ratings yet

- Cement Industry in IndiaDocument19 pagesCement Industry in IndiaShobhit Chandak100% (14)

- Swot Analysis of Ultratech Cement LimitedDocument23 pagesSwot Analysis of Ultratech Cement Limitedtarunnayak11100% (3)

- Ambuja Cement - FinalDocument41 pagesAmbuja Cement - Finalddkshah1708100% (1)

- Working Capital & Ratio Analysis at Dalmia Cement (Bharat) LTDDocument75 pagesWorking Capital & Ratio Analysis at Dalmia Cement (Bharat) LTDSumit Yadav100% (4)

- Project Report On Cement IndustryDocument21 pagesProject Report On Cement Industryhafiz346No ratings yet

- Shreenathji Cement Industries MBA Project Report Prince DudhatraDocument56 pagesShreenathji Cement Industries MBA Project Report Prince DudhatrapRiNcE DuDhAtRa100% (1)

- Ratio Analysis in Cement IndustryDocument65 pagesRatio Analysis in Cement IndustrySiddharth Jain92% (13)

- Consumer Buying Behavior of J.K. Whtie CementDocument111 pagesConsumer Buying Behavior of J.K. Whtie Cementlokesh_045100% (5)

- Economic Reviev of Indian Cement IndustryDocument4 pagesEconomic Reviev of Indian Cement Industryshantanu12892% (13)

- Cement Industry and M&A PDFDocument5 pagesCement Industry and M&A PDFSourin SauNo ratings yet

- CH 08Document12 pagesCH 08Dafina Doci100% (1)

- Swot Analysis of Ultratech CementDocument31 pagesSwot Analysis of Ultratech Cementtarunnayak11100% (7)

- ACC Cement SM Group Project XMBA 24Document30 pagesACC Cement SM Group Project XMBA 24XMBA 24 ITM Vashi86% (7)

- Pestel Analysis On Ultratech Cement AssignmentDocument7 pagesPestel Analysis On Ultratech Cement AssignmentNick Sharma50% (2)

- Indian Cement IndustryDocument73 pagesIndian Cement Industryamit_kumaryad71% (7)

- Market Survey On Cement Industry (Final)Document2 pagesMarket Survey On Cement Industry (Final)Ashish Singh60% (5)

- My PPT Presentation On ULTRA TECH CEMENTDocument13 pagesMy PPT Presentation On ULTRA TECH CEMENTAshish Kumar Pani67% (3)

- Overview of Indian Cement Industry 2010Document17 pagesOverview of Indian Cement Industry 2010shubhav1988100% (2)

- Labour Unrest Edited. 2Document20 pagesLabour Unrest Edited. 2Aakash Saxena100% (1)

- Acc CementDocument30 pagesAcc CementNVNVNVNV43% (7)

- Project Report On CciDocument62 pagesProject Report On CciShilank Sharma100% (2)

- Factors Influencing Marketing of Cement Industry in BangladeshDocument55 pagesFactors Influencing Marketing of Cement Industry in BangladeshTanjin UrmiNo ratings yet

- Birla Cements MarketingDocument45 pagesBirla Cements MarketingDeependra Singh90% (10)

- Project Final - India CementsDocument73 pagesProject Final - India Cementsabhisekparija86% (7)

- Lucky Cement ReportDocument28 pagesLucky Cement ReportSarmad Sajid57% (7)

- A Case Study Depicting Unfair Treatment in A Organization: Haranahally Ramaswamy Institute of Higher EducationDocument9 pagesA Case Study Depicting Unfair Treatment in A Organization: Haranahally Ramaswamy Institute of Higher EducationVinutha CNo ratings yet

- Managerial Economics Project ReportDocument6 pagesManagerial Economics Project ReportchandanjeeNo ratings yet

- Dalmia CementDocument100 pagesDalmia Cementntr75125% (4)

- SCM of UltratechDocument29 pagesSCM of UltratechDisha GanatraNo ratings yet

- Cement Marketing in India: Challenges & Opportunities: SRM University, ChennaiDocument8 pagesCement Marketing in India: Challenges & Opportunities: SRM University, ChennaiAkram JavedNo ratings yet

- History of Aditya Birla GroupDocument9 pagesHistory of Aditya Birla GroupKailash YadavNo ratings yet

- Challenges Faced by Bharat PetroleumDocument2 pagesChallenges Faced by Bharat PetroleumPrerna K KaushikNo ratings yet

- Annual Report of CMADocument66 pagesAnnual Report of CMARiteshHPatelNo ratings yet

- Indian Cement IndustryDocument10 pagesIndian Cement IndustryJovi Agoc100% (1)

- 9-12 Cement Dec11Document4 pages9-12 Cement Dec11Pankaj SawankarNo ratings yet

- Planning Comision SummaryDocument11 pagesPlanning Comision Summarykumud_nishadNo ratings yet

- Indian Cement Industry: Riding The High Tide Managerial Economics Case AnalysisDocument11 pagesIndian Cement Industry: Riding The High Tide Managerial Economics Case AnalysisVrushabh ShelkarNo ratings yet

- Cement Industry and M&A PDFDocument5 pagesCement Industry and M&A PDFSourin SauNo ratings yet

- A Report On Swot Analysis and Pest Analysis of Birla GroupDocument5 pagesA Report On Swot Analysis and Pest Analysis of Birla Groupjustinlanger4100% (5)

- Cement Industry ResearchDocument9 pagesCement Industry ResearchSounakNo ratings yet

- Cement Demand Break Up: ST THDocument42 pagesCement Demand Break Up: ST THsatyamehtaNo ratings yet

- NTPC - Cement Manufacturers AssociationDocument53 pagesNTPC - Cement Manufacturers Associationlaloo01No ratings yet

- Indian Cement IndustryDocument22 pagesIndian Cement IndustryBnaren NarenNo ratings yet

- Cement Industry Feasibility ReportDocument4 pagesCement Industry Feasibility Reportds ww100% (1)

- Harish Kumar Shree Cement ReportDocument87 pagesHarish Kumar Shree Cement Reportrahulsogani123No ratings yet

- Megharaja CBS01Document89 pagesMegharaja CBS01Naveen S GNo ratings yet

- Report On Cement Industry in India By: Shobhit ChandaDocument13 pagesReport On Cement Industry in India By: Shobhit ChandaPrasanta DebnathNo ratings yet

- Presented By: Pawan Kumar ShrivasDocument20 pagesPresented By: Pawan Kumar ShrivasPraveen PrabhakarNo ratings yet

- Group01 - End Term ProjectDocument35 pagesGroup01 - End Term ProjectSiddharth GuptaNo ratings yet

- Study of Indian MarketDocument5 pagesStudy of Indian Marketvipul099No ratings yet

- 7 CementDocument3 pages7 CementNitish KathaitNo ratings yet

- Cost Investment in Different Sectors in Any Cement Manufacturing IndustryDocument7 pagesCost Investment in Different Sectors in Any Cement Manufacturing Industry9098238509No ratings yet

- Binani Cement Research ReportDocument11 pagesBinani Cement Research ReportRinkesh25No ratings yet

- RBSA Indian Cement Industry AnalysisDocument18 pagesRBSA Indian Cement Industry AnalysisPuneet Mathur100% (1)

- PESTLE Analysis of Cement IndustryDocument1 pagePESTLE Analysis of Cement IndustryAniket DeokarNo ratings yet

- ChettinadDocument52 pagesChettinadVinodh KumarNo ratings yet

- The Cement Industry Is One of The Main Beneficiaries of The Infrastructure BoomDocument9 pagesThe Cement Industry Is One of The Main Beneficiaries of The Infrastructure BoomSyedFaisalHasanShahNo ratings yet

- Sport Obermeyer: Click To Edit Master Subtitle StyleDocument6 pagesSport Obermeyer: Click To Edit Master Subtitle Stylekumud_nishadNo ratings yet

- Mumbai Dabbawalla CaseDocument3 pagesMumbai Dabbawalla Casekumud_nishadNo ratings yet

- Planning Comision SummaryDocument11 pagesPlanning Comision Summarykumud_nishadNo ratings yet

- Project TitleDocument1 pageProject Titlekumud_nishadNo ratings yet

- Bindaas Andaaz 2011Document7 pagesBindaas Andaaz 2011kumud_nishadNo ratings yet

- Amazon - Ca - Order 702-5408379-2600263Document1 pageAmazon - Ca - Order 702-5408379-2600263Danny Ricard-LavergneNo ratings yet

- Ibe MCQDocument28 pagesIbe MCQDineshNo ratings yet

- Note 20 Mobile BillDocument1 pageNote 20 Mobile Billakshaybasal jainNo ratings yet

- Emailreceipt 20180208R5974808166Document2 pagesEmailreceipt 20180208R5974808166Ali HassanNo ratings yet

- Tally Prime Record BookDocument19 pagesTally Prime Record Bookmuneest19No ratings yet

- Taxation For Self-Employed Ver1.0Document23 pagesTaxation For Self-Employed Ver1.0Xeena HavenNo ratings yet

- Eticket MR Rathna Balaji Inderpaal SinghDocument3 pagesEticket MR Rathna Balaji Inderpaal SinghInderpaal SinghNo ratings yet

- Temporary: Your DetailsDocument2 pagesTemporary: Your Detailsmankumyad.05100% (1)

- Tax Research Basic NotesDocument8 pagesTax Research Basic NotesMark EdisonNo ratings yet

- Balance Outstanding 0.00: Meter Reading Information Meter Number: 6074294Document1 pageBalance Outstanding 0.00: Meter Reading Information Meter Number: 6074294ramchanduriNo ratings yet

- Monthly Sales Report Monthly Sales ReportDocument2 pagesMonthly Sales Report Monthly Sales ReportDato FolodashviliNo ratings yet

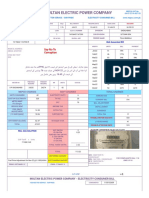

- Multan Electric Power Company: Say No To CorruptionDocument2 pagesMultan Electric Power Company: Say No To CorruptionMehran Ali KhanNo ratings yet

- Telephone Number Amount Payable Due Date: Bill Mail Service Tax InvoiceDocument3 pagesTelephone Number Amount Payable Due Date: Bill Mail Service Tax InvoiceSunnyVishwakarmaNo ratings yet

- Scope of TaxDocument13 pagesScope of Taxraja usamaNo ratings yet

- FAT Mubea Mexico - Seafreight - 27 - 10 - 22 - 000200411Document2 pagesFAT Mubea Mexico - Seafreight - 27 - 10 - 22 - 000200411helton cabralNo ratings yet

- Tax Invoice (Original For Recipient) : 06CEZPR0490G1ZX GstinDocument1 pageTax Invoice (Original For Recipient) : 06CEZPR0490G1ZX GstinKishore Kumar BoggulaNo ratings yet

- Top Ten States With The Lowest Tax BurdenDocument3 pagesTop Ten States With The Lowest Tax BurdenAndreea Anamaria WNo ratings yet

- Professional Fee Calculation: (CPI As A Supplier Gets 2% EWT)Document10 pagesProfessional Fee Calculation: (CPI As A Supplier Gets 2% EWT)Quinciano MorilloNo ratings yet

- Notification No F 10 31 2018 CT V 46 Chhattisgarh Section 68 of The Chhattisgarh GST ADocument2 pagesNotification No F 10 31 2018 CT V 46 Chhattisgarh Section 68 of The Chhattisgarh GST Asandip_agrawalNo ratings yet

- Confirmation ParisDocument2 pagesConfirmation Parissunny singhNo ratings yet

- Test Bank For International Trade 4th Edition Robert C FeenstraDocument28 pagesTest Bank For International Trade 4th Edition Robert C FeenstraJohn Thomas100% (40)

- Taxation in The PhilippinesDocument8 pagesTaxation in The PhilippinesDELA CRUZ, AILEEN M.No ratings yet

- Air Ticket Booking - Book Flight Tickets - Cheap Air Fare - LTC Fare - IRCTC AIRDocument1 pageAir Ticket Booking - Book Flight Tickets - Cheap Air Fare - LTC Fare - IRCTC AIRroomcontrol270No ratings yet

- How To Control MonopoliesDocument3 pagesHow To Control MonopoliesSharma GokhoolNo ratings yet

- Sample Clarification LetterDocument3 pagesSample Clarification LetterRakesh Kumar80% (5)

- Basics of Tariff CalculationDocument27 pagesBasics of Tariff Calculationpintu ramNo ratings yet

- GST Implementation Detailed Document For ConsultantDocument9 pagesGST Implementation Detailed Document For Consultantmahesh gaikwadNo ratings yet