You might also like

- TAX 2 ExercisesDocument22 pagesTAX 2 ExercisesWinter Summer50% (4)

- VAT Tutorial Questions PDFDocument10 pagesVAT Tutorial Questions PDFPeter100% (1)

- Tax 1 C1,3Document10 pagesTax 1 C1,3Artjerjes Comendador PorrasNo ratings yet

- Quiz 1: Science, Technology and Society TestDocument4 pagesQuiz 1: Science, Technology and Society TestElaiza Lozano100% (3)

- Quiz 1: Science, Technology and Society TestDocument4 pagesQuiz 1: Science, Technology and Society TestElaiza Lozano100% (3)

- Sasy N Savy Pty LTD BusinessDocument6 pagesSasy N Savy Pty LTD BusinessMariana MillerNo ratings yet

- Account statement analysisDocument3 pagesAccount statement analysisJohn-EdwardNo ratings yet

- Chapter 9 Input VatDocument10 pagesChapter 9 Input VatHazel Jane EsclamadaNo ratings yet

- Cost Sheets Road Construction DUPADocument223 pagesCost Sheets Road Construction DUPAJames Cabrera67% (6)

- Income Taxation Chapter 1Document5 pagesIncome Taxation Chapter 1Princess Ivy PenaflorNo ratings yet

- Income Taxation01Document7 pagesIncome Taxation01Ailene MendozaNo ratings yet

- Understanding Taxation FundamentalsDocument34 pagesUnderstanding Taxation FundamentalsKaren DammogNo ratings yet

- Taxation - Day 01Document2 pagesTaxation - Day 01Joyce Sherly Ann LuceroNo ratings yet

- Taxation I Atty. Francisco Gonzalez General Principles of TaxationDocument45 pagesTaxation I Atty. Francisco Gonzalez General Principles of TaxationBea Czarina NavarroNo ratings yet

- Womens MonthDocument23 pagesWomens MonthShelene Cathlyn Borja Daga-asNo ratings yet

- Supreme Court reinstates lawyer after 15 years of disbarmentDocument25 pagesSupreme Court reinstates lawyer after 15 years of disbarmentMarivic EspiaNo ratings yet

- Income TaxationDocument124 pagesIncome TaxationGWENN JYTSY BAFLORNo ratings yet

- Permanent Total Disability BenefitsDocument28 pagesPermanent Total Disability BenefitsGel MaulionNo ratings yet

- Midterm Quiz 1 Gross IncomeDocument3 pagesMidterm Quiz 1 Gross IncomeMjhayeNo ratings yet

- Gen. Principles of TaxationDocument22 pagesGen. Principles of TaxationPageduesca RouelNo ratings yet

- HOMEWORK 1 Concept of TaxationDocument5 pagesHOMEWORK 1 Concept of Taxationfitz garlitosNo ratings yet

- Classification of TaxesDocument3 pagesClassification of TaxesRomela Jean OcarizaNo ratings yet

- Taxation: General PrinciplesDocument34 pagesTaxation: General PrinciplesKeziah A GicainNo ratings yet

- TAXATION OF CORPORATIONSDocument26 pagesTAXATION OF CORPORATIONSParticia CorveraNo ratings yet

- Victorias Milling v. Philippine Ports AuthorityDocument3 pagesVictorias Milling v. Philippine Ports Authoritybile_driven_opusNo ratings yet

- Module 6 FINP1 Financial ManagementDocument28 pagesModule 6 FINP1 Financial ManagementChristine Jane LumocsoNo ratings yet

- Comparative Analysis of Ra 8424 and 10963Document2 pagesComparative Analysis of Ra 8424 and 10963Daryl Dizon CabanzaNo ratings yet

- Vanishing DeductionsDocument3 pagesVanishing DeductionsCyrell AsidNo ratings yet

- Accrued Liabilities and Deferred Revenues ExplainedDocument22 pagesAccrued Liabilities and Deferred Revenues Explainedchesca marie penarandaNo ratings yet

- WWW Studocu Com en Au Document Queensland University of Technology Introduction To Taxation Law Lecture Notes Tax Law Exam Notes Final 195771 ViewDocument2 pagesWWW Studocu Com en Au Document Queensland University of Technology Introduction To Taxation Law Lecture Notes Tax Law Exam Notes Final 195771 ViewSudip AdhikariNo ratings yet

- Quizzes in Taxn 1000Document32 pagesQuizzes in Taxn 1000LAIJANIE CLAIRE ALVAREZNo ratings yet

- Tax Dec 3 (Pantawid Recit)Document7 pagesTax Dec 3 (Pantawid Recit)D Del SalNo ratings yet

- Tax Evasion and AviodanceDocument9 pagesTax Evasion and AviodancepoojaNo ratings yet

- OBLICON - Topic SyllabusDocument14 pagesOBLICON - Topic SyllabusKenneth Bryan Tegerero TegioNo ratings yet

- Oblicon CasesDocument12 pagesOblicon CasesAlyssa CornejoNo ratings yet

- Donor's Tax Rates and ExemptionsDocument5 pagesDonor's Tax Rates and ExemptionsKim EspinaNo ratings yet

- Taxation 2 : Introduction Transfer Taxes and Estate TaxDocument22 pagesTaxation 2 : Introduction Transfer Taxes and Estate TaxCharles John Palabrica CubarNo ratings yet

- The Regular Corporate Income TaxDocument4 pagesThe Regular Corporate Income TaxReniel Renz AterradoNo ratings yet

- Philippine Taxation Review QuestionsDocument4 pagesPhilippine Taxation Review QuestionsJane TuazonNo ratings yet

- General Principles of Taxation FundamentalsDocument43 pagesGeneral Principles of Taxation FundamentalsChristine Joy Rejas-TubianoNo ratings yet

- Roxas City Revenue CodeDocument107 pagesRoxas City Revenue CodeRichard Delos ReyesNo ratings yet

- BIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsDocument1 pageBIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsdreaNo ratings yet

- SA's 2013 National Budget focuses on fiscal disciplineDocument7 pagesSA's 2013 National Budget focuses on fiscal disciplineBrilliant MycriNo ratings yet

- PDIC Maximum Deposit Insurance CoverageDocument7 pagesPDIC Maximum Deposit Insurance CoverageChiemy Atienza YokogawaNo ratings yet

- Human Rights Sec 3 Article 9Document2 pagesHuman Rights Sec 3 Article 9Bryan Soriano PascualNo ratings yet

- 2007 Pre-Week Guide in TaxationDocument29 pages2007 Pre-Week Guide in TaxationcasieNo ratings yet

- Chapter 12 - Test BankDocument25 pagesChapter 12 - Test Bankgilli1tr100% (1)

- Income Taxation Handout No. 1-01 Complete TextDocument11 pagesIncome Taxation Handout No. 1-01 Complete TextTong WilsonNo ratings yet

- 1st Quiz in Business TaxationDocument2 pages1st Quiz in Business TaxationPo TekNo ratings yet

- Short Term Non Routine DecisionsDocument8 pagesShort Term Non Routine DecisionsAlthon JayNo ratings yet

- Frank Chavez For OmbudsmanDocument2 pagesFrank Chavez For OmbudsmanmelchizedekmoselNo ratings yet

- DAY 1 Part 1 Fundamental Principles of Taxation StudentsDocument5 pagesDAY 1 Part 1 Fundamental Principles of Taxation StudentsMary Chrisdel Obinque GarciaNo ratings yet

- National and Local Government RelationsDocument25 pagesNational and Local Government Relations미카엘NikothefilipinoguyNo ratings yet

- New Central Bank ActDocument15 pagesNew Central Bank ActLourleth Caraballa LluzNo ratings yet

- BA 127 Notes PDFDocument12 pagesBA 127 Notes PDFLorenz De Lemios NalicaNo ratings yet

- Corporate Governance, Business Ethics, Risk Management and Internal Control: Key ConceptsDocument12 pagesCorporate Governance, Business Ethics, Risk Management and Internal Control: Key ConceptsTuran, Jel Therese A.No ratings yet

- Written Report in INCOME TAXATION MODULE 4 GROSS INCOMEDocument39 pagesWritten Report in INCOME TAXATION MODULE 4 GROSS INCOMEMark Kevin Dimalanta SicatNo ratings yet

- Legal PhiloDocument3 pagesLegal PhiloAngel PeñaflorNo ratings yet

- Exclusion of Gross IncomeDocument14 pagesExclusion of Gross IncomeRnlynNo ratings yet

- Caltex Philippines, Inc. vs. Commission On AuditDocument41 pagesCaltex Philippines, Inc. vs. Commission On AuditJayson Francisco100% (1)

- Intro To Law NotesDocument3 pagesIntro To Law NotesRegieReyAgustinNo ratings yet

- Basics of taxation law in the PhilippinesDocument10 pagesBasics of taxation law in the Philippinesnewa944No ratings yet

- 26sept - Loc GovDocument9 pages26sept - Loc GovYvonne DolorosaNo ratings yet

- CHAPTER-TWO PUBLIC REVENUEDocument76 pagesCHAPTER-TWO PUBLIC REVENUEyebegashetNo ratings yet

- Income Taxation PDFDocument7 pagesIncome Taxation PDFSoahNo ratings yet

- Gains and Losses From Dealings in PropertiesDocument29 pagesGains and Losses From Dealings in PropertiesCj Garcia100% (1)

- TAXATION Flashcards (1.1 Principles of Taxation)Document6 pagesTAXATION Flashcards (1.1 Principles of Taxation)Lucille Rose MamburaoNo ratings yet

- DraftDocument6 pagesDraftJudy Ann AdanteNo ratings yet

- Air Waybill - JT Express - 1 1Document1 pageAir Waybill - JT Express - 1 1Elaiza LozanoNo ratings yet

- Accounting Research Proposal: Tarlac State UniversityDocument1 pageAccounting Research Proposal: Tarlac State UniversityElaiza LozanoNo ratings yet

- Your Name Here: On-The-Job Trainings Position HereDocument2 pagesYour Name Here: On-The-Job Trainings Position HereElaiza LozanoNo ratings yet

- Find The Circulatory System Words Below in The Grid To The LeftDocument1 pageFind The Circulatory System Words Below in The Grid To The LeftElaiza LozanoNo ratings yet

- EnvironmentalDocument1 pageEnvironmentalElaiza LozanoNo ratings yet

- Shira ProcessDocument3 pagesShira ProcessElaiza LozanoNo ratings yet

- Saving The Babies: Looking Upstream For Solutions: by Steven E. Mayer, PH.DDocument4 pagesSaving The Babies: Looking Upstream For Solutions: by Steven E. Mayer, PH.DElaiza LozanoNo ratings yet

- Closet Revolution: (Simple Business Plan)Document3 pagesCloset Revolution: (Simple Business Plan)Elaiza LozanoNo ratings yet

- Group2 Mas5Document12 pagesGroup2 Mas5Elaiza LozanoNo ratings yet

- Final RequirementDocument1 pageFinal RequirementElaiza LozanoNo ratings yet

- Afar 2 Module CH 9 & 10Document16 pagesAfar 2 Module CH 9 & 10Elaiza LozanoNo ratings yet

- Afar 2 Module CH 8 PDFDocument12 pagesAfar 2 Module CH 8 PDFRazmen Ramirez PintoNo ratings yet

- Global City Group 6 Contemporary WorldDocument61 pagesGlobal City Group 6 Contemporary WorldElaiza Lozano50% (2)

- Chapter 2: Science and Technology: Their Natures and RelationshipDocument5 pagesChapter 2: Science and Technology: Their Natures and RelationshipElaiza LozanoNo ratings yet

- ArtsDocument4 pagesArtsElaiza LozanoNo ratings yet

- Tax BulletinDocument72 pagesTax BulletinSamuel Mervin NathNo ratings yet

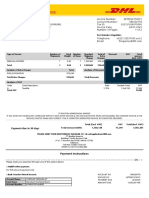

- DHL Express Medical Shipment InvoiceDocument3 pagesDHL Express Medical Shipment InvoiceTri Wahyuni100% (2)

- Contract of Security Services - Docx 2.docx3Document9 pagesContract of Security Services - Docx 2.docx3Michael Cleofas Asuten100% (1)

- CIR Vs CA, Gr. No. 119322, June 4, 1996 FactsDocument15 pagesCIR Vs CA, Gr. No. 119322, June 4, 1996 FactsJepoy Nisperos ReyesNo ratings yet

- CCTV CamerasDocument22 pagesCCTV CamerasKumarReddyNo ratings yet

- Reverse calculate total price and taxDocument7 pagesReverse calculate total price and taxKanishka Thomas Kain100% (1)

- Invoice 593770518Document1 pageInvoice 593770518umeshNo ratings yet

- GST Impact On E-CommerceDocument2 pagesGST Impact On E-CommercePAUL FREDERICK LLMNo ratings yet

- A-Life Joy - Brochure - 6th EditDocument12 pagesA-Life Joy - Brochure - 6th EditYF OngNo ratings yet

- MYOB GST Preparation Guide (Existing Users)Document18 pagesMYOB GST Preparation Guide (Existing Users)manimaran75No ratings yet

- Accounting Quiz BeeDocument83 pagesAccounting Quiz BeeMary Ingrid Arellano RabulanNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sharp CutsNo ratings yet

- VIETNAM INTERNATIONAL TAXATION Update1Document28 pagesVIETNAM INTERNATIONAL TAXATION Update1thaliaNo ratings yet

- Fort Bonifacio V CirDocument10 pagesFort Bonifacio V CirArwella GregorioNo ratings yet

- AT&T Communications Services Phils. Inc. v. CIRDocument8 pagesAT&T Communications Services Phils. Inc. v. CIRAnonymous 8liWSgmINo ratings yet

- Tridharma Vs CTADocument1 pageTridharma Vs CTAKaren Mae ServanNo ratings yet

- Unit 7Document2 pagesUnit 7Nguyễn NamNo ratings yet

- Productflyer - 978 0 387 28523 8Document1 pageProductflyer - 978 0 387 28523 8Swannie SwansonNo ratings yet

- ThesisDocument73 pagesThesisPhâni Räj Gürâgâin100% (2)

- Bir Form 2307 SampleDocument3 pagesBir Form 2307 SampleEliza Cortez Castro50% (2)

- Gems Jewellery Industry in China PDFDocument103 pagesGems Jewellery Industry in China PDFAnonymous M5v9mAUNo ratings yet

- OneOcean Terms ConditionsDocument25 pagesOneOcean Terms ConditionsVladNo ratings yet

- 5f5b86e1aa25c Mohamed Gamal - CVDocument2 pages5f5b86e1aa25c Mohamed Gamal - CVعبدالكريم حمدانNo ratings yet

- Understand Inventory ManagementDocument9 pagesUnderstand Inventory ManagementyelzNo ratings yet