You might also like

- Drawee, He Must Be NAMED ThereinDocument2 pagesDrawee, He Must Be NAMED ThereinGlo GanzonNo ratings yet

- Negotiable Instrument Law ReviewerDocument22 pagesNegotiable Instrument Law ReviewerChris Javier100% (1)

- Nego Reviewer From OnlineDocument35 pagesNego Reviewer From OnlineAK Fernandez100% (1)

- Negotiable InstrumentsDocument36 pagesNegotiable InstrumentsPammyNo ratings yet

- Law on Negotiable InstrumentsDocument7 pagesLaw on Negotiable InstrumentsAna Patricia Serrano100% (1)

- Law 3 PrelimsDocument6 pagesLaw 3 PrelimsRaña Marie Macaranas BobadillaNo ratings yet

- Negotiable Instruments Reviewer (Agbayani Villanueva Sundiang Aquino)Document88 pagesNegotiable Instruments Reviewer (Agbayani Villanueva Sundiang Aquino)Lee Anne Yabut100% (3)

- Negotiable Instruments: - MicaellagarciaDocument4 pagesNegotiable Instruments: - MicaellagarciaMicaella100% (1)

- Commercial Law – Key Points on Negotiable InstrumentsDocument9 pagesCommercial Law – Key Points on Negotiable InstrumentsMunchie MichieNo ratings yet

- Nego ReviewerDocument9 pagesNego Reviewernhizza dawn DaligdigNo ratings yet

- Nego Reviewer KweenDocument38 pagesNego Reviewer KweenRIZELLE BERNADINE MALANGENNo ratings yet

- Rfbt3 Negoin Lecture NotesDocument14 pagesRfbt3 Negoin Lecture NotesWilmar Abriol100% (1)

- Law On Negotiable InstrumentsDocument7 pagesLaw On Negotiable InstrumentsHannah Loren ComendadorNo ratings yet

- The Law on Negotiable Instruments: Promissory Notes vs Bills of ExchangeDocument10 pagesThe Law on Negotiable Instruments: Promissory Notes vs Bills of ExchangeClyde Ian Brett PeñaNo ratings yet

- Differences between Negotiable InstrumentsDocument33 pagesDifferences between Negotiable InstrumentsMary Grace Peralta ParagasNo ratings yet

- NegoDocument2 pagesNegoYasser AureadaNo ratings yet

- Negotiable Instruments CharacteristicsDocument34 pagesNegotiable Instruments CharacteristicsdreaNo ratings yet

- Negotin ReviewerDocument11 pagesNegotin ReviewerDanaNo ratings yet

- Negotiable Instruments Law NotesDocument16 pagesNegotiable Instruments Law NotesernestomalupetNo ratings yet

- Negotiable Instruments LawDocument16 pagesNegotiable Instruments LawgladsNo ratings yet

- Negotiable Instruments Law ExplainedDocument16 pagesNegotiable Instruments Law ExplainedLyka Mae Palarca IrangNo ratings yet

- Negotiable Instruments Reviewer Agbayani Villanueva Sundiang AquinoDocument84 pagesNegotiable Instruments Reviewer Agbayani Villanueva Sundiang AquinoXandae Mempin100% (1)

- Negotiable Instruments Law Notes Atty Zarah Villanueva CastroDocument16 pagesNegotiable Instruments Law Notes Atty Zarah Villanueva CastroMarcelino CasilNo ratings yet

- Negotiable Instruments Law Notes Atty Zarah Villanueva CastroDocument16 pagesNegotiable Instruments Law Notes Atty Zarah Villanueva CastroMadielyn Santarin MirandaNo ratings yet

- Nego Reviewer 1Document11 pagesNego Reviewer 1berrna badongenNo ratings yet

- Mercantile Law Notes PDFDocument34 pagesMercantile Law Notes PDFtoktor toktorNo ratings yet

- Negotiable Instruments Law Notes Atty Zarah Villanueva Castro PDFDocument16 pagesNegotiable Instruments Law Notes Atty Zarah Villanueva Castro PDFAenacia ReyeaNo ratings yet

- Reviewer in NegoDocument7 pagesReviewer in NegoJoan BartolomeNo ratings yet

- Negotiable InstrumentsDocument5 pagesNegotiable InstrumentsJinky MartinezNo ratings yet

- Negotiable Instruments Law Reviewer PDFDocument18 pagesNegotiable Instruments Law Reviewer PDFVenice Jamaila Dagcutan0% (1)

- Commercial Law Atty. RondezDocument108 pagesCommercial Law Atty. RondezJessyyyyy123No ratings yet

- Negotiable Instruments Reviewer YAPK (Until Sec125 Only)Document39 pagesNegotiable Instruments Reviewer YAPK (Until Sec125 Only)Krystoffer YapNo ratings yet

- Negotiable Instruments Non-Negotiable InstrumentsDocument31 pagesNegotiable Instruments Non-Negotiable InstrumentspyriadNo ratings yet

- Negotiable Inctruments LawDocument15 pagesNegotiable Inctruments LawAr Di SagamlaNo ratings yet

- Dishonor by Non-Payment NoticeDocument23 pagesDishonor by Non-Payment NoticeChrissy SabellaNo ratings yet

- Negotiable Instruments Law (Sec1-23)Document11 pagesNegotiable Instruments Law (Sec1-23)Julienne GayondatoNo ratings yet

- Negotiable Instruments ExplainedDocument10 pagesNegotiable Instruments ExplainedAbby Gail TiongsonNo ratings yet

- The Negotiable Instruments LawDocument10 pagesThe Negotiable Instruments LawhanzohatoriNo ratings yet

- Negotiable Instruments GuideDocument30 pagesNegotiable Instruments GuideBea EchiverriNo ratings yet

- Atty. D Old Topics in RFBTDocument51 pagesAtty. D Old Topics in RFBTKathleen MirallesNo ratings yet

- RFBT-08 (Negotiable Instruments)Document22 pagesRFBT-08 (Negotiable Instruments)Erlinda MolinaNo ratings yet

- Philippine Law Reviewers: Commercial Law - Negotiable Instruments LawDocument47 pagesPhilippine Law Reviewers: Commercial Law - Negotiable Instruments Lawlebron JamesNo ratings yet

- Negotiable Instruments Law GuideDocument49 pagesNegotiable Instruments Law GuideGigiRuizTicarNo ratings yet

- Negotiable Instruments GuideDocument38 pagesNegotiable Instruments GuideNasrollah Magayoong NuskaNo ratings yet

- Negotiable Instruments Non-Negotiable InstrumentsDocument3 pagesNegotiable Instruments Non-Negotiable InstrumentsJi YuNo ratings yet

- Negotiable InstrumentDocument4 pagesNegotiable InstrumentOCAMPO Aubrey HeartNo ratings yet

- Negotiable Instruments Reviewer - 3EDocument150 pagesNegotiable Instruments Reviewer - 3ERebecca TatadNo ratings yet

- NEGODocument24 pagesNEGOTj AllasNo ratings yet

- Negotiable Instruments LawDocument2 pagesNegotiable Instruments LawkrstnkyslNo ratings yet

- Negotiable Instruments Law Reviewer PDFDocument51 pagesNegotiable Instruments Law Reviewer PDFKarla Mae RicardeNo ratings yet

- Negotiable Instruments Laws Carlos Hilado Memorial State University Submitted By: Atty. Jul Davi P. SaezDocument26 pagesNegotiable Instruments Laws Carlos Hilado Memorial State University Submitted By: Atty. Jul Davi P. SaezJellie ElmerNo ratings yet

- Nego-Bar Rev Memo Aid 2019 PDFDocument15 pagesNego-Bar Rev Memo Aid 2019 PDFSofia DavidNo ratings yet

- Negotiable Instruments Non-Negotiable InstrumentsDocument41 pagesNegotiable Instruments Non-Negotiable InstrumentsPrincess Aiza MaulanaNo ratings yet

- What is a Negotiable Instrument? Characteristics, Features and TypesDocument14 pagesWhat is a Negotiable Instrument? Characteristics, Features and Typesbright rainNo ratings yet

- Negotiable Instruments Non-Negotiable InstrumentsDocument31 pagesNegotiable Instruments Non-Negotiable InstrumentsMychie Lynne MayugaNo ratings yet

- Negotiable Instruments Law essentialsDocument15 pagesNegotiable Instruments Law essentialsCorneliaAmarraBruhildaOlea-VolterraNo ratings yet

- Law 108 Notes CH 1Document16 pagesLaw 108 Notes CH 1SGTNo ratings yet

- Commercial Law - Negotiable Instruments LawDocument32 pagesCommercial Law - Negotiable Instruments LawGlenda PambagoNo ratings yet

- Negotiable Instruments Law Reviewer PDFDocument55 pagesNegotiable Instruments Law Reviewer PDFJoshua MesinaNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Aarti Jankar Roll No-9611Document54 pagesAarti Jankar Roll No-9611FIN 9611 Aarti JankarNo ratings yet

- JaiibDocument105 pagesJaiibManikantha PattugaralaNo ratings yet

- LK UNIT 3 Memproses Transaksi KeuanganDocument3 pagesLK UNIT 3 Memproses Transaksi KeuanganYudya Dhanny Syah Permana Arvai100% (1)

- CREDIT TRANSACTIONS - Escarez Reviewer - Part IDocument30 pagesCREDIT TRANSACTIONS - Escarez Reviewer - Part IPaul Aaron Esguerra EscarezNo ratings yet

- Liquidity Management PolicyDocument15 pagesLiquidity Management PolicyMazen AlbsharaNo ratings yet

- CM TreasuryDocument12 pagesCM TreasuryChinh Le DinhNo ratings yet

- End Chapter Solutions 2 and 3Document18 pagesEnd Chapter Solutions 2 and 3JpzelleNo ratings yet

- FIM Tutorial 5 (Week 6)Document4 pagesFIM Tutorial 5 (Week 6)Cindy LewNo ratings yet

- Evaluation of Customer Satisfaction On Personal Loan (HDFC& ICICI)Document32 pagesEvaluation of Customer Satisfaction On Personal Loan (HDFC& ICICI)Suresh Babu Reddy50% (2)

- Meezan Bank Report FinalDocument61 pagesMeezan Bank Report FinalMuhammad JamilNo ratings yet

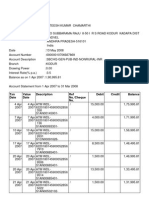

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesTXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancesatishapexNo ratings yet

- INSPECTIONDocument43 pagesINSPECTIONdharampurhaNo ratings yet

- Bachelor of Management With Honours (Bim)Document18 pagesBachelor of Management With Honours (Bim)Aizat AhmadNo ratings yet

- RBI MasterCircular IRACDocument101 pagesRBI MasterCircular IRACneeteesh_nautiyalNo ratings yet

- HSBC Premier Savings Terms & Charges Disclosure: EligibilityDocument3 pagesHSBC Premier Savings Terms & Charges Disclosure: EligibilityAndi PrabowoNo ratings yet

- How to Achieve Success Through Faith and Hard WorkDocument39 pagesHow to Achieve Success Through Faith and Hard WorkMian AdnanNo ratings yet

- Date Mm/dd/yyyy Name of Customer Bank Check # AmountDocument2 pagesDate Mm/dd/yyyy Name of Customer Bank Check # AmountDerick DalisayNo ratings yet

- FM3 Module 3Document33 pagesFM3 Module 3Jay OntuaNo ratings yet

- Facilities With Tally 1Document5 pagesFacilities With Tally 1s_balvantNo ratings yet

- Notes Receivable: Valix, C. T. Et Al. Intermediate Accounting Volume 1. (2019) - Manila: GIC Enterprises & Co. IncDocument9 pagesNotes Receivable: Valix, C. T. Et Al. Intermediate Accounting Volume 1. (2019) - Manila: GIC Enterprises & Co. IncShergie GozumNo ratings yet

- Metrobank Business Account SummaryDocument3 pagesMetrobank Business Account SummaryJack ChardwoodNo ratings yet

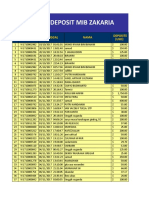

- DEPOSIT LISTDocument284 pagesDEPOSIT LISTIbrahim100% (1)

- Punjab National Bank - Wikipedia, The Free EncyclopediaDocument8 pagesPunjab National Bank - Wikipedia, The Free EncyclopediaPurushotam SharmaNo ratings yet

- Multi-Purpose Loan (MPL) Application FormDocument16 pagesMulti-Purpose Loan (MPL) Application FormPablito BeringNo ratings yet

- PayU Recurring Integration V4Document49 pagesPayU Recurring Integration V4Tamal SenNo ratings yet

- Introduction to Banking and Cooperative Banking in IndiaDocument57 pagesIntroduction to Banking and Cooperative Banking in IndiaRubikaNo ratings yet

- 62198bos50436 cp9Document90 pages62198bos50436 cp9GabbarNo ratings yet

- Fee Book For Classes 1 To 5Document3 pagesFee Book For Classes 1 To 5ankitbasisNo ratings yet

- Everyday English 3: Direct Speech / Reported Speech, Reporting VerbsDocument5 pagesEveryday English 3: Direct Speech / Reported Speech, Reporting Verbsadriana884No ratings yet

- SLBCDocument1 pageSLBCyogesh shingareNo ratings yet