You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Hotel Accounting Standard Manual PDFDocument291 pagesHotel Accounting Standard Manual PDFAgustinus Agus Purwanto100% (3)

- UniqloDocument17 pagesUniqloUmar GondalNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Internal Audit TrainingDocument46 pagesInternal Audit TrainingCharlie Mendoza100% (11)

- (Group 7) Case 5 - Thieves in TexasDocument13 pages(Group 7) Case 5 - Thieves in TexasPintonov PutraNo ratings yet

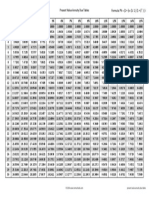

- Present Value Annuity Due TablesDocument1 pagePresent Value Annuity Due TablesDecereen Pineda Rodrigueza100% (2)

- Practical AccountingDocument13 pagesPractical AccountingDecereen Pineda RodriguezaNo ratings yet

- Extrinsic and Intrinsic Factors Influencing Employee Motivation: Lessons From AMREF Health Africa in KenyaDocument12 pagesExtrinsic and Intrinsic Factors Influencing Employee Motivation: Lessons From AMREF Health Africa in KenyaDecereen Pineda RodriguezaNo ratings yet

- Chapter 5 Accounting For Merchandising OperationsDocument15 pagesChapter 5 Accounting For Merchandising OperationsDecereen Pineda RodriguezaNo ratings yet

- Problems On Retained EarningsDocument2 pagesProblems On Retained EarningsDecereen Pineda RodriguezaNo ratings yet

- PPEDocument3 pagesPPEDecereen Pineda RodriguezaNo ratings yet

- Safe FoodDocument45 pagesSafe FoodDecereen Pineda RodriguezaNo ratings yet

- Sge Asf8 - LatviaDocument16 pagesSge Asf8 - LatviaDecereen Pineda RodriguezaNo ratings yet

- The Emergence of Consensus: A Primer: ReviewDocument13 pagesThe Emergence of Consensus: A Primer: ReviewDecereen Pineda RodriguezaNo ratings yet

- African Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryDocument52 pagesAfrican Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryDecereen Pineda Rodrigueza100% (1)

- Bersak CMS Thesis FINAL PDFDocument71 pagesBersak CMS Thesis FINAL PDFDecereen Pineda RodriguezaNo ratings yet

- AdjectivesDocument10 pagesAdjectivesDecereen Pineda RodriguezaNo ratings yet

- EHS Environmental Engineering Manager in Phoenix AZ Resume Frank SkocypecDocument1 pageEHS Environmental Engineering Manager in Phoenix AZ Resume Frank SkocypecFrankSkocypecNo ratings yet

- Framework For The Preparation and Presentation of Financial Statements (Teks Asli Bahasa Inggris Dari Iasc)Document3 pagesFramework For The Preparation and Presentation of Financial Statements (Teks Asli Bahasa Inggris Dari Iasc)Septiawan BhotNo ratings yet

- Acconting and Reporting Practice of Ngo's in The Case of Agoheld (A Case Study at Addis Abeba) - MikeleaksDocument14 pagesAcconting and Reporting Practice of Ngo's in The Case of Agoheld (A Case Study at Addis Abeba) - MikeleaksMohammed Demssie MohammedNo ratings yet

- BONIA-Page 26 To ProxyFormDocument189 pagesBONIA-Page 26 To ProxyFormameraizahNo ratings yet

- Ongc Tripura Power Company LimitedDocument8 pagesOngc Tripura Power Company LimitedKrishna SwamyNo ratings yet

- Feasibility Study For Wheat Flour Production Business Pan in Ethiopia - Haqiqa Investment Consultant in EthiopiaDocument1 pageFeasibility Study For Wheat Flour Production Business Pan in Ethiopia - Haqiqa Investment Consultant in EthiopiaSuleman82% (22)

- Auditing and Assurance Services A Systematic Approach 8th Edition Messier Solutions ManualDocument25 pagesAuditing and Assurance Services A Systematic Approach 8th Edition Messier Solutions ManualDebraPricemkw100% (49)

- GROUP 3 - Data Analytics and Financial ReportDocument3 pagesGROUP 3 - Data Analytics and Financial Reportmutia rasyaNo ratings yet

- Fraud Prevention & DetectionDocument15 pagesFraud Prevention & DetectionswathivishnuNo ratings yet

- Cost-1 Course OutlineDocument2 pagesCost-1 Course OutlineHussen AbdulkadirNo ratings yet

- Quiz Cash and ReceivablesDocument4 pagesQuiz Cash and Receivableserica insiongNo ratings yet

- F.2. Basic Bank Documents and Terminologies Related To BankDocument28 pagesF.2. Basic Bank Documents and Terminologies Related To BankSecret DeityNo ratings yet

- Board Member Tool Kit PDFDocument125 pagesBoard Member Tool Kit PDFJen AndalNo ratings yet

- Q4 Fabm1 ReviewerDocument7 pagesQ4 Fabm1 ReviewerAira MoscosaNo ratings yet

- Tutorial Letter 201/1/2017: Distinctive Financial ReportingDocument8 pagesTutorial Letter 201/1/2017: Distinctive Financial ReportingItumeleng KekanaNo ratings yet

- CM1 Overview of AccountingDocument14 pagesCM1 Overview of AccountingMark GerwinNo ratings yet

- Chapter 13 Auditing and Assurance ServicesDocument26 pagesChapter 13 Auditing and Assurance ServicesEdwin Gunawan100% (2)

- Zergaw ChemedaDocument109 pagesZergaw ChemedaeyaNo ratings yet

- Acc HelpfulDocument994 pagesAcc HelpfulMoksha JainNo ratings yet

- CV Shahzad Ali - 20220409 PDFDocument4 pagesCV Shahzad Ali - 20220409 PDFAli AyubNo ratings yet

- Internal Auditing and The FCPA - April 2010Document25 pagesInternal Auditing and The FCPA - April 2010The Russia MonitorNo ratings yet

- Module 3 Quiz AnswersDocument2 pagesModule 3 Quiz AnswersVon Andrei Medina100% (1)

- Case 5.4Document4 pagesCase 5.4Eloisa Joy MoredoNo ratings yet

- ACCA SBL Leadership UNITSDocument118 pagesACCA SBL Leadership UNITSQuensteen LimNo ratings yet

- HCLDocument22 pagesHCLMisbah JahanNo ratings yet

- Substantive Analytical ProceduresDocument2 pagesSubstantive Analytical ProceduresJuliefe EstigoyNo ratings yet