You might also like

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Theory Summary NotesDocument2 pagesTheory Summary NotesSuzy BaeNo ratings yet

- The Internal Controls of CashDocument3 pagesThe Internal Controls of CashbelliissiimmaaNo ratings yet

- Unit 3: Internal Control Over CashDocument10 pagesUnit 3: Internal Control Over CashBereket DesalegnNo ratings yet

- Audit of CashDocument23 pagesAudit of CashmeseleNo ratings yet

- Unit 2Document11 pagesUnit 2fekadegebretsadik478729No ratings yet

- CHAPTER 7Document16 pagesCHAPTER 7girmayadane7No ratings yet

- Chapter 6 ACCT 101 - NewDocument7 pagesChapter 6 ACCT 101 - NewXXXXXXXXXXXXXXXXXXNo ratings yet

- Fundamentals of Book Keeping and Office PracticeDocument34 pagesFundamentals of Book Keeping and Office PracticemuteyobarlinNo ratings yet

- ACC 106 Internal Control To Bank ReconciliationDocument3 pagesACC 106 Internal Control To Bank ReconciliationAriane Grace Hiteroza MargajayNo ratings yet

- Unit 2 Audit of Cash and Marketable SecuritiesDocument9 pagesUnit 2 Audit of Cash and Marketable Securitiessolomon adamuNo ratings yet

- Accounting Ch-5 Cash & ReceivablesDocument97 pagesAccounting Ch-5 Cash & ReceivablesFeda EtefaNo ratings yet

- Balance Cash HoldingDocument4 pagesBalance Cash HoldingTilahun S. KuraNo ratings yet

- FIN AC 1 - Module 3Document4 pagesFIN AC 1 - Module 3Ashley ManaliliNo ratings yet

- Cash and Cash Equivalents ContinuationDocument16 pagesCash and Cash Equivalents ContinuationCrystal NadalaNo ratings yet

- Module 1 CashDocument13 pagesModule 1 CashKim JisooNo ratings yet

- Cash and Cash Equivalents GuideDocument6 pagesCash and Cash Equivalents GuideKairo ZeviusNo ratings yet

- Chapter 5 DUTYDocument19 pagesChapter 5 DUTYtemedebereNo ratings yet

- 03 Audit of CashDocument14 pages03 Audit of CashJoyce Anne GarduqueNo ratings yet

- Fundamentals of Acct - I, Lecture Note - Chapter 5-1Document13 pagesFundamentals of Acct - I, Lecture Note - Chapter 5-1Kiya GeremewNo ratings yet

- Audit Cash ControlsDocument35 pagesAudit Cash ControlsJazzyNo ratings yet

- Module 1 CashDocument13 pagesModule 1 Cashtite ko'y malakeNo ratings yet

- Cash and Cash EquivalentsDocument27 pagesCash and Cash EquivalentsPatOcampoNo ratings yet

- CC Cash Over and ShortDocument3 pagesCC Cash Over and ShortDanica BalinasNo ratings yet

- Module 1 5 AnswersDocument111 pagesModule 1 5 AnswersryanNo ratings yet

- Cash and Cash EquivalentsDocument7 pagesCash and Cash EquivalentsHunNo ratings yet

- Balance Cash Holding Teaching MaterialDocument18 pagesBalance Cash Holding Teaching MaterialAbdi Mucee TubeNo ratings yet

- Cash and Cash Equivalents FundamentalsDocument10 pagesCash and Cash Equivalents FundamentalsGRACE ANN BERGONIONo ratings yet

- Errors & FraudsDocument27 pagesErrors & FraudsmostakNo ratings yet

- Audit CHAPTER TWODocument23 pagesAudit CHAPTER TWOTesfaye Megiso BegajoNo ratings yet

- BedhewbdjkewDocument16 pagesBedhewbdjkewMaica A.No ratings yet

- Iac1 C1 DalidaDocument6 pagesIac1 C1 DalidaEdith DalidaNo ratings yet

- Acc Cash and Cash Equivalent Continuation NotesDocument3 pagesAcc Cash and Cash Equivalent Continuation NotesShane QuintoNo ratings yet

- Chapter 3: Cash and ReceivablesDocument7 pagesChapter 3: Cash and ReceivablesZuber ZinabuNo ratings yet

- Acfn 3162 CH 2 Audit of Cash and Marketable Securities FCDocument44 pagesAcfn 3162 CH 2 Audit of Cash and Marketable Securities FCBethelhem100% (1)

- Lecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringDocument24 pagesLecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- Chapter 8 NotesDocument3 pagesChapter 8 NotesKhushboo BadayaNo ratings yet

- Cash & Cash Equivalents - Part 2Document9 pagesCash & Cash Equivalents - Part 2Chin DyNo ratings yet

- Cash and Liquidity ManagementDocument14 pagesCash and Liquidity ManagementAldrin ZolinaNo ratings yet

- Lecture Notes On Cash Book & Petty Cash BookDocument7 pagesLecture Notes On Cash Book & Petty Cash BookINSHAN IMRAN RAMSAROOPNo ratings yet

- AUDIT OF CashDocument24 pagesAUDIT OF CashMr.AccntngNo ratings yet

- Cash and Internal Control: Ani Wilujeng Suryani, PHDDocument47 pagesCash and Internal Control: Ani Wilujeng Suryani, PHDRoby RohmadNo ratings yet

- Accounting for Cash and Cash Equivalents GuideDocument4 pagesAccounting for Cash and Cash Equivalents GuideSecurity Bank Personal LoansNo ratings yet

- Unit-2 Audit of Cash and Marketable SecuritiesDocument6 pagesUnit-2 Audit of Cash and Marketable SecuritiesKiya AbdiNo ratings yet

- Intermediate financial accounting 1 chapter 3-7Document60 pagesIntermediate financial accounting 1 chapter 3-7mooyiboonnameeNo ratings yet

- L29.Phạm-Đức-MinhDocument6 pagesL29.Phạm-Đức-Minh09-Cao Thị Mỹ LệNo ratings yet

- Policy On Revolving Fund and Petty Cash FundDocument6 pagesPolicy On Revolving Fund and Petty Cash Fundmarvinceledio100% (3)

- Audit of Cash Chapter 1Document8 pagesAudit of Cash Chapter 1SAN FELIPE Maria Czarina MontereseNo ratings yet

- Cash and Cash EquivalentDocument5 pagesCash and Cash EquivalentMASIGLAT, CRIZEL JOY, Y.No ratings yet

- Cash and Cash Equivalents GuideDocument15 pagesCash and Cash Equivalents GuideSofia NadineNo ratings yet

- Control Over Cash - For LayoutDocument10 pagesControl Over Cash - For LayoutMariel RascoNo ratings yet

- Chapter Four The Audit of Accounting Information SystemsDocument20 pagesChapter Four The Audit of Accounting Information SystemsPrince Hiwot EthiopiaNo ratings yet

- Petty Cash Disbursements PolicyDocument3 pagesPetty Cash Disbursements PolicyAngelo Andro SuanNo ratings yet

- Financial Accounting 1 Unit 9Document23 pagesFinancial Accounting 1 Unit 9chuchuNo ratings yet

- Week04 PPT 2022 Before ClassDocument64 pagesWeek04 PPT 2022 Before Class罗上宗No ratings yet

- Financial Accounting - Study Guide Chapter 7: Internal Control and Cash Internal Control SystemDocument3 pagesFinancial Accounting - Study Guide Chapter 7: Internal Control and Cash Internal Control SystemMurtaza HussainNo ratings yet

- CashDocument15 pagesCashGizaw BelayNo ratings yet

- Audit of Cash and Cash EquivalentsDocument2 pagesAudit of Cash and Cash EquivalentsAngel Chane OstrazNo ratings yet

- PBL Session 1: Revenue Cycle: TREASURERDocument4 pagesPBL Session 1: Revenue Cycle: TREASURERSiti NorhanaNo ratings yet

- Chapter 7Document22 pagesChapter 7Genanew AbebeNo ratings yet

- Dit & OtcDocument2 pagesDit & OtcSuzy BaeNo ratings yet

- Adbi Dynamic Regional DevDocument36 pagesAdbi Dynamic Regional DevSuzy BaeNo ratings yet

- Witness SOC: Equitable Distribution of WealthDocument8 pagesWitness SOC: Equitable Distribution of WealthSuzy BaeNo ratings yet

- Building Design Green BuildingDocument4 pagesBuilding Design Green BuildingSuzy BaeNo ratings yet

- Auditing Canadian 7th Edition Smieliauskas Test Bank DownloadDocument16 pagesAuditing Canadian 7th Edition Smieliauskas Test Bank DownloadMargaret Narcisse100% (21)

- Faiyaj FICODocument4 pagesFaiyaj FICOAbdul RaheemNo ratings yet

- Regulation of Insurance Industry Act, No 43 of 2000 PDFDocument37 pagesRegulation of Insurance Industry Act, No 43 of 2000 PDFAnonymous q9HUEDJbHNo ratings yet

- AT QuizDocument15 pagesAT QuizClydeNo ratings yet

- SOP - Life CycleDocument5 pagesSOP - Life Cyclesachin smadhravalliNo ratings yet

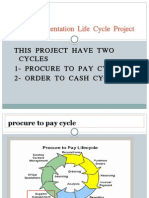

- Full Implementation Life Cycle ProjectDocument27 pagesFull Implementation Life Cycle ProjectSaif AhmedNo ratings yet

- Auditing The Financing/Investing Process: Cash and InvestmentsDocument22 pagesAuditing The Financing/Investing Process: Cash and InvestmentsasmaNo ratings yet

- DCS - Status of Account ModuleDocument6 pagesDCS - Status of Account ModuleTejas ThakorNo ratings yet

- UOB Risk Management 2Document10 pagesUOB Risk Management 2jariya.attNo ratings yet

- NMC GOLD FINANCE LIMITED - Forensic Report 1Document11 pagesNMC GOLD FINANCE LIMITED - Forensic Report 1Anand KhotNo ratings yet

- COA Obligation and Disbursement RecordsDocument7 pagesCOA Obligation and Disbursement RecordsAddy GuinalNo ratings yet

- ISO RegistrationDocument4 pagesISO RegistrationSweta MorNo ratings yet

- SEC authority and corporate governance provisionsDocument3 pagesSEC authority and corporate governance provisionsNavsNo ratings yet

- 2017 CMA CGM Annual ReportDocument81 pages2017 CMA CGM Annual Reportmiquel20No ratings yet

- RiskDocument5 pagesRiskAsfand Zubair MalikNo ratings yet

- Cost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Document35 pagesCost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Yonas BamlakuNo ratings yet

- Day 2 PresentationDocument6 pagesDay 2 PresentationIftekhar-Ul- IslamNo ratings yet

- Quality Control Plan (For Study) PDFDocument10 pagesQuality Control Plan (For Study) PDFRobin GuNo ratings yet

- Coursepack ESG 2020Document143 pagesCoursepack ESG 2020Vaibhav MehtaNo ratings yet

- Grant Thornton - Co-Op 3Document7 pagesGrant Thornton - Co-Op 3ConnieLowNo ratings yet

- LBMA Summary Report ANTAM-UBPP Logam Mulia 2015Document5 pagesLBMA Summary Report ANTAM-UBPP Logam Mulia 2015Hery RomansyahNo ratings yet

- Quality Plan for Oleohydraulic Systems ManufacturerDocument14 pagesQuality Plan for Oleohydraulic Systems Manufacturerneurolepsia379033% (3)

- Notes AccountingDocument9 pagesNotes AccountingRudyNo ratings yet

- Ghana Tracking Transparency & Accountability Report 2011Document20 pagesGhana Tracking Transparency & Accountability Report 2011tsar_philip2010No ratings yet

- May June 2020 FullDocument75 pagesMay June 2020 FullArif TusherNo ratings yet

- Fabm Second Quarter ExamDocument34 pagesFabm Second Quarter ExamLorelyn ApigoNo ratings yet

- SEAL Annual Report 2016 Highlights GrowthDocument98 pagesSEAL Annual Report 2016 Highlights GrowthBenjaminNo ratings yet

- Jaguar Land Rover LimitedDocument59 pagesJaguar Land Rover Limitedharsh shahNo ratings yet

- Corporate Governance McomDocument38 pagesCorporate Governance McomNimi100% (1)

- NISM MF Distributors Certification Exam PresentationDocument456 pagesNISM MF Distributors Certification Exam PresentationVetri M Konar100% (4)

- Molly's Game: The True Story of the 26-Year-Old Woman Behind the Most Exclusive, High-Stakes Underground Poker Game in the WorldFrom EverandMolly's Game: The True Story of the 26-Year-Old Woman Behind the Most Exclusive, High-Stakes Underground Poker Game in the WorldRating: 3.5 out of 5 stars3.5/5 (129)

- Phil Gordon's Little Green Book: Lessons and Teachings in No Limit Texas Hold'emFrom EverandPhil Gordon's Little Green Book: Lessons and Teachings in No Limit Texas Hold'emRating: 4 out of 5 stars4/5 (64)

- Poker: A Beginners Guide To No Limit Texas Holdem and Understand Poker Strategies in Order to Win the Games of PokerFrom EverandPoker: A Beginners Guide To No Limit Texas Holdem and Understand Poker Strategies in Order to Win the Games of PokerRating: 5 out of 5 stars5/5 (49)

- Alchemy Elementals: A Tool for Planetary Healing: An Immersive Audio Experience for Spiritual AwakeningFrom EverandAlchemy Elementals: A Tool for Planetary Healing: An Immersive Audio Experience for Spiritual AwakeningRating: 5 out of 5 stars5/5 (3)

- The Book of Card Games: The Complete Rules to the Classics, Family Favorites, and Forgotten GamesFrom EverandThe Book of Card Games: The Complete Rules to the Classics, Family Favorites, and Forgotten GamesNo ratings yet

- How to Be a Poker Player: The Philosophy of PokerFrom EverandHow to Be a Poker Player: The Philosophy of PokerRating: 4.5 out of 5 stars4.5/5 (4)

- Phil Gordon's Little Blue Book: More Lessons and Hand Analysis in No Limit Texas Hold'emFrom EverandPhil Gordon's Little Blue Book: More Lessons and Hand Analysis in No Limit Texas Hold'emRating: 4.5 out of 5 stars4.5/5 (7)

- Phil Gordon's Little Gold Book: Advanced Lessons for Mastering Poker 2.0From EverandPhil Gordon's Little Gold Book: Advanced Lessons for Mastering Poker 2.0Rating: 3.5 out of 5 stars3.5/5 (6)

- Mental Floss: Genius Instruction ManualFrom EverandMental Floss: Genius Instruction ManualRating: 4 out of 5 stars4/5 (27)

- The Everything Card Tricks Book: Over 100 Amazing Tricks to Impress Your Friends And Family!From EverandThe Everything Card Tricks Book: Over 100 Amazing Tricks to Impress Your Friends And Family!No ratings yet

- POKER MATH: Strategy and Tactics for Mastering Poker Mathematics and Improving Your Game (2022 Guide for Beginners)From EverandPOKER MATH: Strategy and Tactics for Mastering Poker Mathematics and Improving Your Game (2022 Guide for Beginners)No ratings yet

- Poker Satellite Strategy: How to qualify for the main events of high stakes live and online poker tournamentsFrom EverandPoker Satellite Strategy: How to qualify for the main events of high stakes live and online poker tournamentsRating: 4 out of 5 stars4/5 (7)

- The Biggest Bluff by Maria Konnikova: Key Takeaways, Summary & AnalysisFrom EverandThe Biggest Bluff by Maria Konnikova: Key Takeaways, Summary & AnalysisNo ratings yet

- Target: JackAce - Outsmart and Outplay the JackAce in No-Limit HoldemFrom EverandTarget: JackAce - Outsmart and Outplay the JackAce in No-Limit HoldemNo ratings yet

- The Everything Online Poker Book: An Insider's Guide to Playing-and Winning-the Hottest Games on the InternetFrom EverandThe Everything Online Poker Book: An Insider's Guide to Playing-and Winning-the Hottest Games on the InternetNo ratings yet