You might also like

- Quantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskFrom EverandQuantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskRating: 3.5 out of 5 stars3.5/5 (1)

- LifeInsRetirementValuation M06 Profit 181205Document57 pagesLifeInsRetirementValuation M06 Profit 181205Jeff Jones100% (1)

- LifeInsRetirementValuation M15 AppraisalValues 181205Document46 pagesLifeInsRetirementValuation M15 AppraisalValues 181205Jeff JonesNo ratings yet

- LifeInsRetirementValuation M05 LifeValuation 181205Document83 pagesLifeInsRetirementValuation M05 LifeValuation 181205Jeff JonesNo ratings yet

- LI&R Valuation 2020 S1 Tutorial 8Document6 pagesLI&R Valuation 2020 S1 Tutorial 8Jeff GundyNo ratings yet

- LI&R Valuation 2020 S1 Tutorial 5 - Exercise & SolutionsDocument24 pagesLI&R Valuation 2020 S1 Tutorial 5 - Exercise & SolutionsJeff GundyNo ratings yet

- LI&R LI&R Val S1 2020 Asset Share and ParDocument13 pagesLI&R LI&R Val S1 2020 Asset Share and ParJeff GundyNo ratings yet

- LI&R Valuation 2020 S1 Tutorial 6 - ExerciseDocument7 pagesLI&R Valuation 2020 S1 Tutorial 6 - ExerciseJeff GundyNo ratings yet

- LI&R Valuation 2020 S1 Tutorial 8-1Document9 pagesLI&R Valuation 2020 S1 Tutorial 8-1Jeff GundyNo ratings yet

- LI&R Val S1 2020 M01 Introduction PDFDocument25 pagesLI&R Val S1 2020 M01 Introduction PDFJeff GundyNo ratings yet

- LI&R Val S1 2020 Tutorial 4 Q&A PDFDocument16 pagesLI&R Val S1 2020 Tutorial 4 Q&A PDFJeff GundyNo ratings yet

- LIaR Module 12 Q and ADocument3 pagesLIaR Module 12 Q and AJeff JonesNo ratings yet

- LifeInsRetirementValuation M11 Assets 181205Document36 pagesLifeInsRetirementValuation M11 Assets 181205Jeff JonesNo ratings yet

- LIaR Module 11 Q and ADocument3 pagesLIaR Module 11 Q and AJeff JonesNo ratings yet

- LI&R Val S1 2020 M14 Capital PDFDocument99 pagesLI&R Val S1 2020 M14 Capital PDFJeff GundyNo ratings yet

- LIaR Module 8 Q and ADocument5 pagesLIaR Module 8 Q and AJeff JonesNo ratings yet

- LI&R Valuation 2020 S1 Tutorial 6 - Exercise & Solutions - No NotesDocument21 pagesLI&R Valuation 2020 S1 Tutorial 6 - Exercise & Solutions - No NotesJeff GundyNo ratings yet

- Book An Introduction To The Math of Financial Derivatives Neftci S.N. SOLUTIONDocument90 pagesBook An Introduction To The Math of Financial Derivatives Neftci S.N. SOLUTIONAtiqur KhanNo ratings yet

- LI&R Val S1 2020 Tutorial 1Document27 pagesLI&R Val S1 2020 Tutorial 1Jeff GundyNo ratings yet

- LifeInsRetirementValuation M05 LifeValuation 181205Document83 pagesLifeInsRetirementValuation M05 LifeValuation 181205Jeff JonesNo ratings yet

- Institute of Actuaries of India: Subject ST4 - Pensions and Other Employee BenefitsDocument4 pagesInstitute of Actuaries of India: Subject ST4 - Pensions and Other Employee BenefitsVignesh SrinivasanNo ratings yet

- Benifit Pension ObligationDocument20 pagesBenifit Pension ObligationTouseefNo ratings yet

- LI&R Val S1 2020 M08 Exercise 8.5Document2 pagesLI&R Val S1 2020 M08 Exercise 8.5Jeff GundyNo ratings yet

- Claims Reserving ManualDocument229 pagesClaims Reserving ManualThato HollaufNo ratings yet

- Basel II Risk Weight FunctionsDocument31 pagesBasel II Risk Weight FunctionsmargusroseNo ratings yet

- SA3 General Insurance PDFDocument4 pagesSA3 General Insurance PDFVignesh Srinivasan100% (1)

- Time Value of MoneyDocument30 pagesTime Value of MoneyAshia12No ratings yet

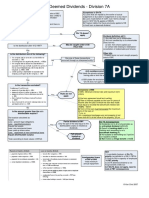

- 3-3 Div 7A Deemed Divs - VLDocument1 page3-3 Div 7A Deemed Divs - VLoddsey0713No ratings yet

- Ca3 Pu 15 PDFDocument10 pagesCa3 Pu 15 PDFPolelarNo ratings yet

- GARP FRM Practice Exam 2011 Level2Document63 pagesGARP FRM Practice Exam 2011 Level2Kelvin TanNo ratings yet

- ACCA F9 Lecture 2Document37 pagesACCA F9 Lecture 2Fathimath Azmath AliNo ratings yet

- Business Finance Peirson 11e CH 3Document24 pagesBusiness Finance Peirson 11e CH 3RitaNo ratings yet

- Asset SampleDocument30 pagesAsset SampleDilakshini VjKumarNo ratings yet

- Claims Reserving Using GAMLSSDocument15 pagesClaims Reserving Using GAMLSSGiorgio SpedicatoNo ratings yet

- Week07 Workshop AnswersDocument10 pagesWeek07 Workshop Answersneok30% (1)

- 2007 FRM Practice ExamDocument116 pages2007 FRM Practice Examabhishekriyer100% (1)

- Embedded Value Calculation For A Life Insurance CompanyDocument27 pagesEmbedded Value Calculation For A Life Insurance CompanyJoin RiotNo ratings yet

- B Pension Risk TransferDocument7 pagesB Pension Risk TransferMikhail FrancisNo ratings yet

- Module 2Document12 pagesModule 2zoyaNo ratings yet

- Understanding Actuarial ValuationDocument56 pagesUnderstanding Actuarial Valuationkកុសល67% (3)

- Chapter 07 Solutions ManualDocument12 pagesChapter 07 Solutions ManualImroz MahmudNo ratings yet

- CLexcel ACT2040Document81 pagesCLexcel ACT2040irsadNo ratings yet

- If1 Syllabus 2016 20160107 115441Document5 pagesIf1 Syllabus 2016 20160107 115441Mohamed ArafaNo ratings yet

- QA Chapter 1 2 3 4 5Document145 pagesQA Chapter 1 2 3 4 5Rajvi Sampat100% (2)

- Sa2 Pu 14 PDFDocument150 pagesSa2 Pu 14 PDFPolelarNo ratings yet

- R36 The Arbitrage Free Valuation Model Slides PDFDocument22 pagesR36 The Arbitrage Free Valuation Model Slides PDFPawan Rathi0% (1)

- Practice Midterm SolutionsDocument18 pagesPractice Midterm SolutionsGNo ratings yet

- A Summary of Actuarial Formulae and Tables: Curtin Student Actuarial Society Last Updated: February 20, 2019Document55 pagesA Summary of Actuarial Formulae and Tables: Curtin Student Actuarial Society Last Updated: February 20, 2019DENISONNo ratings yet

- III.B.6 Credit Risk Capital CalculationDocument28 pagesIII.B.6 Credit Risk Capital CalculationvladimirpopovicNo ratings yet

- Basel I II IIIDocument20 pagesBasel I II IIISachin TodurNo ratings yet

- Bonds With Embedded OptionsDocument9 pagesBonds With Embedded OptionsSajib KarNo ratings yet

- Chapter 8 Insurance PricingDocument17 pagesChapter 8 Insurance Pricingticen100% (1)

- Refinancing Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SevenDocument6 pagesRefinancing Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SevenJeffNo ratings yet

- Pension Revolution: A Solution to the Pensions CrisisFrom EverandPension Revolution: A Solution to the Pensions CrisisNo ratings yet

- Debt ManagementDocument5 pagesDebt Managementminhdoworking1811No ratings yet

- SLM Unit 07 Mbf201Document17 pagesSLM Unit 07 Mbf201Pankaj Kumar100% (1)

- Chapter 1: Literature Review On The Financial Ratios AnalysisDocument19 pagesChapter 1: Literature Review On The Financial Ratios AnalysisAnh Hà Thị TrâmNo ratings yet

- LifeInsRetirementValuation M05 LifeValuation 181205Document83 pagesLifeInsRetirementValuation M05 LifeValuation 181205Jeff JonesNo ratings yet

- LIaR Module 11 Q and ADocument3 pagesLIaR Module 11 Q and AJeff JonesNo ratings yet

- LIaR Module 8 Q and ADocument5 pagesLIaR Module 8 Q and AJeff JonesNo ratings yet

- 17 Ferris An Introduction To Analysis of SurplusDocument15 pages17 Ferris An Introduction To Analysis of SurplusJeff JonesNo ratings yet

- LifeInsRetirementValuation M11 Assets 181205Document36 pagesLifeInsRetirementValuation M11 Assets 181205Jeff JonesNo ratings yet

- LIaR Module 12 Q and ADocument3 pagesLIaR Module 12 Q and AJeff JonesNo ratings yet

- Bulletin 1 - WSC Futsal 2023 PDFDocument24 pagesBulletin 1 - WSC Futsal 2023 PDFMaks BrunovićNo ratings yet

- LIFEB305Document209 pagesLIFEB305PriyalPatel0% (1)

- MRIDUPABAN DUTTA - AS01AP7729 HONDA ACTIVA 2024-01-16 2025-01-15 Digit Two-Wheeler Liabilty Only PolicyDocument2 pagesMRIDUPABAN DUTTA - AS01AP7729 HONDA ACTIVA 2024-01-16 2025-01-15 Digit Two-Wheeler Liabilty Only PolicyMridupaban DuttaNo ratings yet

- Insurance ReviewerDocument25 pagesInsurance ReviewerJohnCarrasco100% (1)

- Insurance Broker Business PlanDocument21 pagesInsurance Broker Business PlanChristwolf00760% (10)

- Life Insurance Module Chap 1 - 3 StudentsDocument53 pagesLife Insurance Module Chap 1 - 3 StudentsGabriel GarciaNo ratings yet

- Design and Implementation of An Online Insurance Management System For eDocument12 pagesDesign and Implementation of An Online Insurance Management System For eJohnny WolfNo ratings yet

- Principles and Practices of ManagementDocument188 pagesPrinciples and Practices of Managementhiteshkumarpanchani100% (1)

- Qua Chee Gan Vs Law Union G.R. No. L-4611 December 17, 1955Document2 pagesQua Chee Gan Vs Law Union G.R. No. L-4611 December 17, 1955Emrico CabahugNo ratings yet

- http:// rgiclservices.reliancegeneral.co.in/ PDFDownload/ViewPDF.aspx? PolicyNo=1104262348016357 &| PolicyNo:1104262348016357 | CustName:RAJESH HARISHCHANDRA MHASHELKAR | Prod:2348 | RSD:19-Jul-2016 | RED:18-Jul-2017Document2 pageshttp:// rgiclservices.reliancegeneral.co.in/ PDFDownload/ViewPDF.aspx? PolicyNo=1104262348016357 &| PolicyNo:1104262348016357 | CustName:RAJESH HARISHCHANDRA MHASHELKAR | Prod:2348 | RSD:19-Jul-2016 | RED:18-Jul-2017RGILNo ratings yet

- Memorandum Respondent RollNo 15-16-17 PDFDocument20 pagesMemorandum Respondent RollNo 15-16-17 PDFPratik Thaker67% (3)

- Sprinklers in Schools PDFDocument48 pagesSprinklers in Schools PDFGabetsos KaraflidisNo ratings yet

- Assessment Written 2020 21Document10 pagesAssessment Written 2020 21dyna ruzethNo ratings yet

- Misca 2013 Faq'S: Student QuestionsDocument5 pagesMisca 2013 Faq'S: Student QuestionsSteve KinleyNo ratings yet

- The Complete Guide To Financial PlanningDocument160 pagesThe Complete Guide To Financial PlanningVikas Acharya100% (2)

- Easy Health Insurance Claim FormDocument8 pagesEasy Health Insurance Claim FormDiwakar NaiduNo ratings yet

- Without Financial InstitutionsDocument2 pagesWithout Financial InstitutionsLevi Emmanuel Veloso BravoNo ratings yet

- BBSA 4103 Specialised Financial Accounting September Semester 2019Document8 pagesBBSA 4103 Specialised Financial Accounting September Semester 2019ananthan nadarajanNo ratings yet

- Infographics - TaxDocument12 pagesInfographics - TaxPablo InocencioNo ratings yet

- HW Questions Income TaxDocument34 pagesHW Questions Income TaxAina Niaz100% (1)

- Stockistagreement (Sample Adammaya)Document5 pagesStockistagreement (Sample Adammaya)Mohd Fadzly EnganNo ratings yet

- M.sc. in Actuarial Science and Quantitative FinanceDocument5 pagesM.sc. in Actuarial Science and Quantitative FinanceSahil ShethNo ratings yet

- Auto Claims Adjuster or Bodily Injury Claims Examiner or No FaulDocument2 pagesAuto Claims Adjuster or Bodily Injury Claims Examiner or No Faulapi-78946297No ratings yet

- Antitrust 24k Gavil 04Document63 pagesAntitrust 24k Gavil 04Brittany Tyrus100% (1)

- Chapter 8Document4 pagesChapter 8abebechmarkos7No ratings yet

- Efu Education PlanDocument4 pagesEfu Education PlanSoofi Bedil BekasNo ratings yet

- APGLIDocument7 pagesAPGLIskssahul59No ratings yet

- 1RR-SD-01 - New Subcontractor Details & Prequalification (Rainscreen Reso...Document8 pages1RR-SD-01 - New Subcontractor Details & Prequalification (Rainscreen Reso...Amalia PanaNo ratings yet

- Internship Report WWWDocument68 pagesInternship Report WWWWasim Imam100% (1)

- KA02 AG 1986 InsuranceDocument2 pagesKA02 AG 1986 Insurancecommission sompoNo ratings yet