You might also like

- Samsung GalaxyDocument1 pageSamsung Galaxykumar gaurav100% (2)

- MGMT 11th Edition Williams Test BankDocument22 pagesMGMT 11th Edition Williams Test Bankjamesmartinezstzejixmcg100% (16)

- Shipping Policies: Sherry - Lehmann SDocument7 pagesShipping Policies: Sherry - Lehmann Sjake_aviNo ratings yet

- 14.54 International Economics Handout 4: 1 The Current AccountDocument6 pages14.54 International Economics Handout 4: 1 The Current AccountMartin ZapataNo ratings yet

- Economics 202A Lecture Outline #6 (Version 1.1)Document15 pagesEconomics 202A Lecture Outline #6 (Version 1.1)Machaca Alvaro MamaniNo ratings yet

- International Monetary Theory and PolicyDocument2 pagesInternational Monetary Theory and PolicyRicky AbichandaniNo ratings yet

- International Monetary Theory and PolicyDocument2 pagesInternational Monetary Theory and PolicyhappystoneNo ratings yet

- (N. Gregory Mankiw) Macroeconomics (9th Edition) (BookFi) - Pages-176-182-DikompresiDocument7 pages(N. Gregory Mankiw) Macroeconomics (9th Edition) (BookFi) - Pages-176-182-DikompresiNoveliaNo ratings yet

- International Macroeconomics: Slides For Chapter 3: Theory of Current Account DeterminationDocument41 pagesInternational Macroeconomics: Slides For Chapter 3: Theory of Current Account DeterminationM Kaderi KibriaNo ratings yet

- Balance of PaymentsDocument40 pagesBalance of PaymentsKamal KantNo ratings yet

- Multinational Financial ManagementDocument37 pagesMultinational Financial ManagementjadudhahNo ratings yet

- Topic1 NewDocument19 pagesTopic1 NewCh AhNo ratings yet

- Final 2014Document12 pagesFinal 2014laurice wongNo ratings yet

- Obstfeld, Rogoff (1996) - Foundations of International Macroeconomics - 3Document20 pagesObstfeld, Rogoff (1996) - Foundations of International Macroeconomics - 3Martin Elias DionicioNo ratings yet

- International Economics - Intertemporal Trade and Current Account BalanceDocument17 pagesInternational Economics - Intertemporal Trade and Current Account BalanceMaxime KirpachNo ratings yet

- International Macroeconomics 4th Edition Feenstra Solutions ManualDocument19 pagesInternational Macroeconomics 4th Edition Feenstra Solutions Manualclitusarielbeehax100% (25)

- A Model of The Current Account: Costas Arkolakis Teaching Assistant: Yijia LuDocument21 pagesA Model of The Current Account: Costas Arkolakis Teaching Assistant: Yijia LuhappystoneNo ratings yet

- Bernanke Book Chapter 1. Saving and Investment in The Open EconomyDocument3 pagesBernanke Book Chapter 1. Saving and Investment in The Open Economykhan babaNo ratings yet

- The Balance of Payments and International Economic LinkagesDocument28 pagesThe Balance of Payments and International Economic LinkagesRajnikant PatelNo ratings yet

- International Monetary Theory and Policy: T 1 T 2 N 1 N 2 0Document2 pagesInternational Monetary Theory and Policy: T 1 T 2 N 1 N 2 0happystoneNo ratings yet

- Harms Int Macro Excercises Solutions PhH040417Document66 pagesHarms Int Macro Excercises Solutions PhH040417Brenda CardosoNo ratings yet

- Chap 06Document76 pagesChap 06Yiğit KocamanNo ratings yet

- Balance of Payment and International Economic LinkagesDocument35 pagesBalance of Payment and International Economic LinkagesAnil PatelNo ratings yet

- Chapter 5: Saving and Investment in The Open Economy: Yulei LuoDocument43 pagesChapter 5: Saving and Investment in The Open Economy: Yulei LuoAkash HedaNo ratings yet

- Multinational Financial Management: Alan Shapiro 7 Edition J.Wiley & SonsDocument37 pagesMultinational Financial Management: Alan Shapiro 7 Edition J.Wiley & SonsNafisha RaihanNo ratings yet

- Chapter 5Document26 pagesChapter 5nigusNo ratings yet

- Essay 2 Inter Temporal Approach To Current Account DynamicsDocument18 pagesEssay 2 Inter Temporal Approach To Current Account DynamicspnewyorkNo ratings yet

- Balance of PaymentsDocument26 pagesBalance of PaymentsRajesh Chandra MouryaNo ratings yet

- Econ 442 Problem Set 2 (Umuc)Document2 pagesEcon 442 Problem Set 2 (Umuc)OmarNiemczykNo ratings yet

- 11 - International FinanceDocument41 pages11 - International Financethaihanguyen2005No ratings yet

- Open Economy BoPDocument41 pagesOpen Economy BoPAnaNo ratings yet

- The Balance of Payments and International Economic LinkagesDocument28 pagesThe Balance of Payments and International Economic LinkagesAfsar MondalNo ratings yet

- Session 4 Open EconomyDocument55 pagesSession 4 Open Economyshivam kumarNo ratings yet

- University of Zurich, Dept. of Economics Prof. Dr. Mathias Hoffmann Exam For Spring 2015 LectureDocument4 pagesUniversity of Zurich, Dept. of Economics Prof. Dr. Mathias Hoffmann Exam For Spring 2015 LectureMatthias LeuthardNo ratings yet

- Chap 05Document55 pagesChap 05Iftikhar AhmedNo ratings yet

- Open Economy1Document64 pagesOpen Economy1Mariam JahanzebNo ratings yet

- Brochure C I AnglaisDocument10 pagesBrochure C I AnglaisHa Nguyen Pham HaiNo ratings yet

- The Balance of Payments and International Economic LinkagesDocument28 pagesThe Balance of Payments and International Economic Linkagesbahram_yaktaparastNo ratings yet

- Xii - Economics - Sample Paper - Answer KeyDocument10 pagesXii - Economics - Sample Paper - Answer KeyMishti GhoshNo ratings yet

- Langdana, F. Macroeconomic Policy Demystifying Monetary and Fiscal Policy. Cap. 3Document30 pagesLangdana, F. Macroeconomic Policy Demystifying Monetary and Fiscal Policy. Cap. 3Flor MartinezNo ratings yet

- Rhizopus SP HardDocument57 pagesRhizopus SP HardRizta RinindaNo ratings yet

- CH 22Document5 pagesCH 22Ahmad AlatasNo ratings yet

- Pontijicia Universidade Catolica Do Rio de Janeiro, Rio de Janeiro, BrazilDocument18 pagesPontijicia Universidade Catolica Do Rio de Janeiro, Rio de Janeiro, BrazilyaredNo ratings yet

- 10 - Macro For Open EconomyDocument39 pages10 - Macro For Open Economyxyz abcNo ratings yet

- Macroeconomics For An Open Economy: Nguynvithng Ễ Ệ ƯDocument39 pagesMacroeconomics For An Open Economy: Nguynvithng Ễ Ệ ƯKhanh3787 BacNo ratings yet

- The Open Economy: AcroeconomicsDocument64 pagesThe Open Economy: AcroeconomicsRamesh vatsNo ratings yet

- Economic Brief: Should We Worry About Trade Imbalances?Document6 pagesEconomic Brief: Should We Worry About Trade Imbalances?TBP_Think_Tank100% (2)

- Ch. 5 - The Open EconomyDocument35 pagesCh. 5 - The Open EconomyaritjahjaNo ratings yet

- The Open Economy: AcroeconomicsDocument60 pagesThe Open Economy: AcroeconomicsVaibhav AroraNo ratings yet

- Ifm - 3Document12 pagesIfm - 3Tường LinhNo ratings yet

- International FinanceDocument37 pagesInternational FinanceJenell FonsecaNo ratings yet

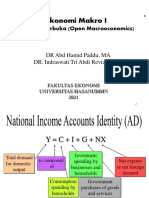

- Ekonomi Makro I: Ekonomi Terbuka (Open Macroeconomics)Document16 pagesEkonomi Makro I: Ekonomi Terbuka (Open Macroeconomics)Reyna ArellanoNo ratings yet

- National Income Accounting and The Balance of Payments The National Income AccountsDocument7 pagesNational Income Accounting and The Balance of Payments The National Income AccountsRitesh SinghaiNo ratings yet

- Macroeconomics: The Open Economy IDocument57 pagesMacroeconomics: The Open Economy IVaibhav AroraNo ratings yet

- Topic 12: The Balance of PaymentsDocument34 pagesTopic 12: The Balance of PaymentsaaharisNo ratings yet

- UGmacro19b NotesDocument51 pagesUGmacro19b NotesHo Chi SinNo ratings yet

- Bai 2 - Chu Chuyen Von Quoc Te (Autosaved) (Compatibility Mode)Document33 pagesBai 2 - Chu Chuyen Von Quoc Te (Autosaved) (Compatibility Mode)pham nguyetNo ratings yet

- The Open Economy: MACROECONOMICS, 8th EditionDocument31 pagesThe Open Economy: MACROECONOMICS, 8th EditionFahriNo ratings yet

- Balance of PaymentDocument17 pagesBalance of PaymentLucky Verma- 3:33No ratings yet

- Macroeconomics & The Global EconomyDocument23 pagesMacroeconomics & The Global Economysubash thapaNo ratings yet

- International Flow of Funds & Engines of GrowthDocument82 pagesInternational Flow of Funds & Engines of GrowthPanashe MachekepfuNo ratings yet

- Copia Di International Economics 1Document56 pagesCopia Di International Economics 1eleniko khurtsilavaNo ratings yet

- International Macroeconomics: Slides For Chapter 6: External Adjustment in Small and Large EconomiesDocument34 pagesInternational Macroeconomics: Slides For Chapter 6: External Adjustment in Small and Large EconomiesM Kaderi KibriaNo ratings yet

- International Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountDocument5 pagesInternational Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountM Kaderi KibriaNo ratings yet

- International Macroeconomics: Slides For Chapter 11: Exchange Rate Policy and UnemploymentDocument47 pagesInternational Macroeconomics: Slides For Chapter 11: Exchange Rate Policy and UnemploymentM Kaderi KibriaNo ratings yet

- International Macroeconomics: Slides For Chapter 10Document37 pagesInternational Macroeconomics: Slides For Chapter 10M Kaderi KibriaNo ratings yet

- International Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationDocument54 pagesInternational Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationM Kaderi KibriaNo ratings yet

- TeachingRatings DescriptionDocument1 pageTeachingRatings DescriptionJesse SeSeNo ratings yet

- International Macroeconomics: Slides For Chapter 3: Theory of Current Account DeterminationDocument41 pagesInternational Macroeconomics: Slides For Chapter 3: Theory of Current Account DeterminationM Kaderi KibriaNo ratings yet

- International Macroeconomics: Slides For Chapter 7: Twin Deficits: Fiscal Deficits and Current Account ImbalancesDocument74 pagesInternational Macroeconomics: Slides For Chapter 7: Twin Deficits: Fiscal Deficits and Current Account ImbalancesM Kaderi KibriaNo ratings yet

- International Macroeconomics: Slides For Chapter 1: Global ImbalancesDocument54 pagesInternational Macroeconomics: Slides For Chapter 1: Global ImbalancesM Kaderi KibriaNo ratings yet

- International Macroeconomics: Slides For Chapter 9: Determinants of The Real Exchange RateDocument55 pagesInternational Macroeconomics: Slides For Chapter 9: Determinants of The Real Exchange RateM Kaderi KibriaNo ratings yet

- Why Bangladesh: PharmaceuticalDocument2 pagesWhy Bangladesh: PharmaceuticalM Kaderi KibriaNo ratings yet

- National Australia Bank AR 2002Document200 pagesNational Australia Bank AR 2002M Kaderi KibriaNo ratings yet

- BB Gudline Forex Transaction Vol - 2Document145 pagesBB Gudline Forex Transaction Vol - 2M Kaderi Kibria0% (1)

- Foreign Investment in Bangladesh: Section - IDocument3 pagesForeign Investment in Bangladesh: Section - IM Kaderi KibriaNo ratings yet

- Assignment 1 - ACCT20071 - T1 2016 1Document2 pagesAssignment 1 - ACCT20071 - T1 2016 1M Kaderi KibriaNo ratings yet

- Anwar HossainDocument29 pagesAnwar HossainM Kaderi KibriaNo ratings yet

- Sanchez RoblesDocument19 pagesSanchez RoblesM Kaderi KibriaNo ratings yet

- Cocacola Case Bus 401Document8 pagesCocacola Case Bus 401M Kaderi KibriaNo ratings yet

- Mcbride p3 Exercises and AnswersDocument55 pagesMcbride p3 Exercises and Answersapi-260512563No ratings yet

- The Lawyer and The ClientDocument2 pagesThe Lawyer and The ClientlalaNo ratings yet

- 2 LESSON - Spoiled, Defective, Scrap, WasteDocument3 pages2 LESSON - Spoiled, Defective, Scrap, WasteMaureen Kaye PaloNo ratings yet

- Pestel Analysis of Airtel in NigeriaDocument10 pagesPestel Analysis of Airtel in NigeriaSam Rehman100% (1)

- Project Summary: AENG 527 Project Feasibility Study Department of Aeronautical Engineering PATTS College of AeronauticsDocument3 pagesProject Summary: AENG 527 Project Feasibility Study Department of Aeronautical Engineering PATTS College of AeronauticsAlanNo ratings yet

- Effects of Inventory Management System On Performance of Petroleum Stations in Kitale Town, KenyaDocument66 pagesEffects of Inventory Management System On Performance of Petroleum Stations in Kitale Town, KenyaJablack Angola MugabeNo ratings yet

- Series Four 12 Cylinder GSI/LT Repair & Overhaul ManualDocument1 pageSeries Four 12 Cylinder GSI/LT Repair & Overhaul ManuallouatiNo ratings yet

- Memorandum and Articles of Association of A MFBDocument18 pagesMemorandum and Articles of Association of A MFBWandooE.AtsenNo ratings yet

- Industrial Engineering ProjectsDocument316 pagesIndustrial Engineering ProjectsbonostoreNo ratings yet

- 170-Article Text-2032-1-10-20221130Document7 pages170-Article Text-2032-1-10-20221130HdtnovNo ratings yet

- PDP 5 29Document1 pagePDP 5 29api-686105315No ratings yet

- How To Pick Intraday Market Direction - The 80% RuleDocument7 pagesHow To Pick Intraday Market Direction - The 80% RulecontactrnNo ratings yet

- Manual VishwakarmaDocument9 pagesManual VishwakarmaJagadish KumarNo ratings yet

- How To Write A Business Plan, Sales Plan - QuocDocument40 pagesHow To Write A Business Plan, Sales Plan - Quoctlq1mpoNo ratings yet

- Introduction To The Airline Planning Process: MIT IcatDocument23 pagesIntroduction To The Airline Planning Process: MIT IcatTalha HussainNo ratings yet

- Examen de Time Value - Cash Flows - Financial StatementsDocument9 pagesExamen de Time Value - Cash Flows - Financial Statementsecrescy66No ratings yet

- Maritime Agenda 2010-2020Document450 pagesMaritime Agenda 2010-2020Venkateswaran PathaiNo ratings yet

- List of ExhibitorsDocument48 pagesList of ExhibitorsAditya SureshNo ratings yet

- CV and Cover Letter - Sharaf InnovationDocument4 pagesCV and Cover Letter - Sharaf InnovationTuly gomesNo ratings yet

- Piper Alpha: Lessons Learnt, 2008Document5 pagesPiper Alpha: Lessons Learnt, 2008tomarpansingNo ratings yet

- Jsa Breaking Down Bop Into Handling SkidDocument4 pagesJsa Breaking Down Bop Into Handling SkidPaulNo ratings yet

- Smart WatchDocument1 pageSmart WatchHarishNo ratings yet

- Module 1Document53 pagesModule 1RekhsNo ratings yet

- EDP 3 Product DevelopmentDocument15 pagesEDP 3 Product DevelopmentatulkirarNo ratings yet

- Salcon Berhad PDFDocument9 pagesSalcon Berhad PDFRachmatt RossNo ratings yet

- DIAGNOSTIC TEST-IN-ORG-.-MGT-with-Answer-KeyDocument6 pagesDIAGNOSTIC TEST-IN-ORG-.-MGT-with-Answer-KeyFRANCESNo ratings yet

- Clarius Film Financing OverviewDocument4 pagesClarius Film Financing OverviewPropertywizzNo ratings yet