You might also like

- Free Online Courses WebsitesDocument27 pagesFree Online Courses Websitespervez4356No ratings yet

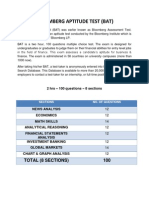

- Bloomberg Aptitude Test (BAT)Document10 pagesBloomberg Aptitude Test (BAT)Shivgan Joshi100% (1)

- Elliott Wave Timing Beyond Ordinary Fibonacci MethodsFrom EverandElliott Wave Timing Beyond Ordinary Fibonacci MethodsRating: 4 out of 5 stars4/5 (21)

- A New Method of Forecasting Trend Change DatesDocument8 pagesA New Method of Forecasting Trend Change DatesArc Angel M100% (1)

- Powerful Forecasting With MS Excel SampleDocument257 pagesPowerful Forecasting With MS Excel SampleHarsa WaraNo ratings yet

- SSRN Id1138782 PDFDocument45 pagesSSRN Id1138782 PDFmanojNo ratings yet

- IRAN Sleeping Giant at A Turning PointDocument58 pagesIRAN Sleeping Giant at A Turning PointmahdiseifNo ratings yet

- Jackel, Kawai - The Future Is Convex - Wilmott Magazine - Feb 2005Document12 pagesJackel, Kawai - The Future Is Convex - Wilmott Magazine - Feb 2005levine_simonNo ratings yet

- How To Be The Golden Egg in The Trading Game PrintDocument68 pagesHow To Be The Golden Egg in The Trading Game PrintNagy100% (1)

- Crude Oil Price and Stock Market MovementDocument27 pagesCrude Oil Price and Stock Market Movementdilip kumar gorai75% (4)

- Markov Switching Model ToolDocument39 pagesMarkov Switching Model ToolcristianmondacaNo ratings yet

- Leif Anderson - Volatility SkewsDocument39 pagesLeif Anderson - Volatility SkewsSubrat VermaNo ratings yet

- eFX October 2011Document196 pageseFX October 2011hquaoNo ratings yet

- 10 Steps To Building A Winning Trading Plan PDFDocument8 pages10 Steps To Building A Winning Trading Plan PDFscreen1 record100% (1)

- Econometrics - Final ProjectDocument11 pagesEconometrics - Final ProjectPelayo Esparza SolaNo ratings yet

- Leif Andersen - Extended Libor Market Models With Stochastic Volatility PDFDocument43 pagesLeif Andersen - Extended Libor Market Models With Stochastic Volatility PDFChun Ming Jeffy TamNo ratings yet

- From Implied To Spot Volatilities: Valdo DurrlemanDocument21 pagesFrom Implied To Spot Volatilities: Valdo DurrlemanginovainmonaNo ratings yet

- Investors Perception Towards Stock MarketDocument67 pagesInvestors Perception Towards Stock MarketHappy Singh36% (22)

- Powerful Forecasting With MS Excel SampleDocument257 pagesPowerful Forecasting With MS Excel SampleBiwesh NeupaneNo ratings yet

- An Empirical Study of Price-Volume Relation: Contemporaneous Correlation and Dynamics Between Price Volatility and Trading Volume in the Hong Kong Stock Market.From EverandAn Empirical Study of Price-Volume Relation: Contemporaneous Correlation and Dynamics Between Price Volatility and Trading Volume in the Hong Kong Stock Market.No ratings yet

- The Structure and Development of Ethiopia's Financial SectorDocument14 pagesThe Structure and Development of Ethiopia's Financial SectorHenry DunaNo ratings yet

- Foreign ExchnageDocument34 pagesForeign ExchnageNiranjan HnNo ratings yet

- Non-Linear Forecasting in High Frequency Time SeriesDocument17 pagesNon-Linear Forecasting in High Frequency Time SeriesDylan AdrianNo ratings yet

- Feweco 20030708115600Document16 pagesFeweco 20030708115600Aditya GuptaNo ratings yet

- Markets96 Momenta PDFDocument8 pagesMarkets96 Momenta PDFLester IngberNo ratings yet

- Garch ModelDocument3 pagesGarch ModelFaroq OmarNo ratings yet

- 09 Ba402Document22 pages09 Ba402shabaazkurmally.um1No ratings yet

- Garch XDocument9 pagesGarch XGiovanni AitaNo ratings yet

- Data Analysis: Theory DossierDocument51 pagesData Analysis: Theory DossierCarla MartinezNo ratings yet

- Statistical Inference For Time-InhomogeneousDocument27 pagesStatistical Inference For Time-InhomogeneousScott TreloarNo ratings yet

- Samy - Stochastic Volatility and Option Pricing in The BrazilianDocument41 pagesSamy - Stochastic Volatility and Option Pricing in The Brazilianajdcavalcante78No ratings yet

- Scenario Simulation: Theory and MethodologyDocument25 pagesScenario Simulation: Theory and Methodologyseth_tolevNo ratings yet

- MULTIVARIATE COINTEGRATION ANALYSIS AND THE LONG-RUN VALIDITY OF PPP - Peter Kugler and Carlos LenzDocument6 pagesMULTIVARIATE COINTEGRATION ANALYSIS AND THE LONG-RUN VALIDITY OF PPP - Peter Kugler and Carlos LenzovidorlimagabrielNo ratings yet

- About The MS Regress PackageDocument38 pagesAbout The MS Regress PackageDom DeSiciliaNo ratings yet

- Interest-Rate Models: Chapter SummaryDocument15 pagesInterest-Rate Models: Chapter SummaryasdasdNo ratings yet

- Multi-Variate Stochastic Volatility Modelling Using Wishart Autoregressive ProcessesDocument13 pagesMulti-Variate Stochastic Volatility Modelling Using Wishart Autoregressive ProcessesTommy AndersonNo ratings yet

- Lie Brooks Faff Modeling The Equity Beta Risk of Australian Financial Sector CompaniesDocument12 pagesLie Brooks Faff Modeling The Equity Beta Risk of Australian Financial Sector CompaniesAskar MulkubayevNo ratings yet

- An Investment Strategy Based On Stochastic Unit Root ModelsDocument8 pagesAn Investment Strategy Based On Stochastic Unit Root ModelsHusain SulemaniNo ratings yet

- Estimating Stock Market Volatility With Markov Regime-Switching GARCH ModelsDocument11 pagesEstimating Stock Market Volatility With Markov Regime-Switching GARCH ModelseduardohortaNo ratings yet

- Powerful Forecasting With MS Excel SampleDocument257 pagesPowerful Forecasting With MS Excel SamplelpachasmNo ratings yet

- SSRN Id1762118Document25 pagesSSRN Id1762118parkjoonsuuNo ratings yet

- Trend-Following Hedge Funds and Multi-Period Asset AllocationDocument16 pagesTrend-Following Hedge Funds and Multi-Period Asset Allocationb7567921No ratings yet

- About The MS Regress PackageDocument28 pagesAbout The MS Regress PackagegliptakNo ratings yet

- A Step-By-Step Procedure To The Numerical Solution For Time-Dependent Partial Derivative Equations in Three Spatial DimensionsDocument29 pagesA Step-By-Step Procedure To The Numerical Solution For Time-Dependent Partial Derivative Equations in Three Spatial Dimensionssportcar2000No ratings yet

- The Conditional Autoregressive Geometric Process Model For Range DataDocument35 pagesThe Conditional Autoregressive Geometric Process Model For Range Datajshew_jr_junkNo ratings yet

- 0053 Dynamics of Commodity Forward CurvesDocument25 pages0053 Dynamics of Commodity Forward Curvesamitnp7373No ratings yet

- A Discrete Time Model For Pricing Treasury Bills, Forward, and Futures ContractsDocument20 pagesA Discrete Time Model For Pricing Treasury Bills, Forward, and Futures ContractsbaxihNo ratings yet

- Applied Energy: Zhongfu Tan, Jinliang Zhang, Jianhui Wang, Jun XuDocument5 pagesApplied Energy: Zhongfu Tan, Jinliang Zhang, Jianhui Wang, Jun XuVamsi KajaNo ratings yet

- Forecasting InflationDocument106 pagesForecasting InflationNicolas BaroneNo ratings yet

- Using Machine Learning Models To Predict S&P500 Price Level and Spread DirectionDocument6 pagesUsing Machine Learning Models To Predict S&P500 Price Level and Spread DirectionjajabinksNo ratings yet

- ECOM031 Financial Econometrics Lecture 4: Extending GARCH Models and Stochastic Volatility ModelsDocument5 pagesECOM031 Financial Econometrics Lecture 4: Extending GARCH Models and Stochastic Volatility ModelsBelindennoluNo ratings yet

- Exchange Rate Forecasting JournalDocument13 pagesExchange Rate Forecasting JournalPrashant TejwaniNo ratings yet

- Ingles Filtro EcuadorDocument15 pagesIngles Filtro EcuadorHenry BautistaNo ratings yet

- JeanninIoriSamuels PinningDocument12 pagesJeanninIoriSamuels PinningginovainmonaNo ratings yet

- Extreme Moves in Daily Foreign Exchange Rates and Risk Limit SettingDocument12 pagesExtreme Moves in Daily Foreign Exchange Rates and Risk Limit SettingAqeela FatimaNo ratings yet

- Model of TheDocument9 pagesModel of ThequimkoNo ratings yet

- Testing The Unbiased Forward Exchange Rate Hypothesis Using A Markov Switching Model and Instrumental VariablesDocument18 pagesTesting The Unbiased Forward Exchange Rate Hypothesis Using A Markov Switching Model and Instrumental VariablesNishant ShahNo ratings yet

- Zima 2009-02-09 Stochastic Programming Gas ExampleDocument7 pagesZima 2009-02-09 Stochastic Programming Gas ExampleJayampathi SamarasingheNo ratings yet

- Uncovering The Trend Following StrategyDocument10 pagesUncovering The Trend Following StrategyRikers11No ratings yet

- Method of Moments Estimation of GO-GARCH Models: H. Peter Boswijk and Roy Van Der WeideDocument26 pagesMethod of Moments Estimation of GO-GARCH Models: H. Peter Boswijk and Roy Van Der Weiderutendo13No ratings yet

- Is Indonesia A High Inflation Country?: - A Markov Regime Switching Model ApproachDocument15 pagesIs Indonesia A High Inflation Country?: - A Markov Regime Switching Model ApproacheviewsNo ratings yet

- Jump-Diffusion Stock-Return Model With Weighted Fitting of Time-Dependent ParametersDocument6 pagesJump-Diffusion Stock-Return Model With Weighted Fitting of Time-Dependent ParametersG.D.M.MadushanthaNo ratings yet

- Whitepaper High Frequency October 21Document6 pagesWhitepaper High Frequency October 211q1q1q1q1q1q1q1qNo ratings yet

- Bloomberg Implied Volatility Method 2008 NewDocument5 pagesBloomberg Implied Volatility Method 2008 NewMrlichlam VoNo ratings yet

- Algorithmic Trading Strategy, Based On GARCH (1, 1) Volatility and Volume Weighted Average Price of AssetDocument6 pagesAlgorithmic Trading Strategy, Based On GARCH (1, 1) Volatility and Volume Weighted Average Price of AssetInternational Organization of Scientific Research (IOSR)No ratings yet

- PHD Convexity MartDocument18 pagesPHD Convexity Martswinki3No ratings yet

- Forecasting The Return Volatility of The Exchange RateDocument53 pagesForecasting The Return Volatility of The Exchange RateProdan IoanaNo ratings yet

- Calculation of Volatility in A Jump-Diffusion Model: Javier F. NavasDocument17 pagesCalculation of Volatility in A Jump-Diffusion Model: Javier F. Navasnikk09No ratings yet

- EncurtidosDocument7 pagesEncurtidosRoberto Tello UrreloNo ratings yet

- Ferreirasaraiva2016 PDFDocument34 pagesFerreirasaraiva2016 PDFRoberto Tello UrreloNo ratings yet

- Challenges in Industrial Fermentation Technology Research PDFDocument13 pagesChallenges in Industrial Fermentation Technology Research PDFRoberto Tello UrreloNo ratings yet

- Chemical Engineering Science: V. Kumaran, P. BandaruDocument13 pagesChemical Engineering Science: V. Kumaran, P. BandaruRoberto Tello UrreloNo ratings yet

- Accepted Manuscript: Chemical Engineering JournalDocument38 pagesAccepted Manuscript: Chemical Engineering JournalRoberto Tello UrreloNo ratings yet

- Rheological Properties of The Mucilage Gum (Opuntia Ficus Indica)Document8 pagesRheological Properties of The Mucilage Gum (Opuntia Ficus Indica)Roberto Tello UrreloNo ratings yet

- Vries Mann 2009Document6 pagesVries Mann 2009Roberto Tello UrreloNo ratings yet

- Liquidity Provision in The Overnight Foreign Exchange MarketDocument22 pagesLiquidity Provision in The Overnight Foreign Exchange MarketRoberto Tello UrreloNo ratings yet

- Articulo Alpaca-Meat ScienceDocument6 pagesArticulo Alpaca-Meat ScienceRoberto Tello UrreloNo ratings yet

- Securities Board of Nepal: Jawalakhel, Lalitpur, Nepal 9 October 2020Document132 pagesSecurities Board of Nepal: Jawalakhel, Lalitpur, Nepal 9 October 2020Max MysterioNo ratings yet

- Business Finance Slide PDFDocument430 pagesBusiness Finance Slide PDFElikem KokorokoNo ratings yet

- Demb 11: .Assignment Topics For - Business Policy and Strategic Management EXECUTIVE M.B.A, May, 2012Document9 pagesDemb 11: .Assignment Topics For - Business Policy and Strategic Management EXECUTIVE M.B.A, May, 2012pemmasanikrishnaNo ratings yet

- Em .226 - Raj Chauhan SybfmDocument17 pagesEm .226 - Raj Chauhan SybfmULTRA RAJNo ratings yet

- QUIZ-1 Monetary Theory and PolicyDocument1 pageQUIZ-1 Monetary Theory and PolicyAltaf HussainNo ratings yet

- In Primary MarketDocument3 pagesIn Primary MarketAshishNo ratings yet

- Universal BankingDocument24 pagesUniversal BankingShreya BhatiaNo ratings yet

- A Project Report On: "Online Vs Offline Trading"Document74 pagesA Project Report On: "Online Vs Offline Trading"Ashutosh SinghNo ratings yet

- XII - BST - ch-10 - Financial MarketDocument11 pagesXII - BST - ch-10 - Financial Marketneetu khemkaNo ratings yet

- Assignment On Banking ProductDocument6 pagesAssignment On Banking ProductTabaraAnannyaNo ratings yet

- Investor Guide BookDocument169 pagesInvestor Guide BooktonyvinayakNo ratings yet

- What Is Foreign ExchangeDocument4 pagesWhat Is Foreign ExchangevmktptNo ratings yet

- GSL 007Document52 pagesGSL 0072imediaNo ratings yet

- Underlying Security: Futures ContractDocument12 pagesUnderlying Security: Futures Contractjames bondddNo ratings yet

- một số câu hỏi bài tập tiếng anhDocument21 pagesmột số câu hỏi bài tập tiếng anhNam chính Chị củaNo ratings yet

- Securities Lending Market Guide 2009Document84 pagesSecurities Lending Market Guide 20092imediaNo ratings yet

- FMI7e ch25Document61 pagesFMI7e ch25lehoangthuchienNo ratings yet

- IQ Test Your Investment Quotient ExercisesDocument40 pagesIQ Test Your Investment Quotient ExercisesRahul100% (2)

- NISM Series VB Mutual Fund Foundation Dec 2017 PDFDocument141 pagesNISM Series VB Mutual Fund Foundation Dec 2017 PDFPurvaNo ratings yet