You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

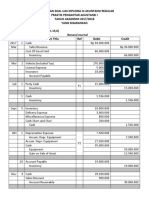

- Gripping GaapDocument1,295 pagesGripping GaapJACK VUMA86% (7)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- EPBCS Admin Guide PDFDocument174 pagesEPBCS Admin Guide PDFRosa Maria Moreno MartinNo ratings yet

- Knowledge Areas: Defining Process Group Aligning Process Group Authorizing & Controlling Process GroupDocument9 pagesKnowledge Areas: Defining Process Group Aligning Process Group Authorizing & Controlling Process Grouppromethuschow100% (2)

- Ais - Chapter 1Document54 pagesAis - Chapter 1LumongtadJoanMaeNo ratings yet

- Revaluation ModelDocument33 pagesRevaluation ModelLumongtadJoanMaeNo ratings yet

- IMPAIRMENT OF ASSET Acctg 211Document30 pagesIMPAIRMENT OF ASSET Acctg 211LumongtadJoanMaeNo ratings yet

- Impairment of Asset: Cash Generating UnitDocument28 pagesImpairment of Asset: Cash Generating UnitLumongtadJoanMaeNo ratings yet

- Chapter 10Document26 pagesChapter 10LumongtadJoanMaeNo ratings yet

- Impairment of Asset: Cash Generating UnitDocument28 pagesImpairment of Asset: Cash Generating UnitLumongtadJoanMaeNo ratings yet

- Impairment of Asset Acctg 211Document30 pagesImpairment of Asset Acctg 211LumongtadJoanMaeNo ratings yet

- Partnership LiquidationDocument6 pagesPartnership LiquidationEmzNo ratings yet

- Pfrs 13 Fair Value MeasurementDocument22 pagesPfrs 13 Fair Value MeasurementShane PasayloNo ratings yet

- Foreign Exchange Risk Management PDFDocument73 pagesForeign Exchange Risk Management PDFBhavya Mohan100% (1)

- Name: Shamal Vivek Singh ID: s11172656: Af314 AssignmentDocument8 pagesName: Shamal Vivek Singh ID: s11172656: Af314 AssignmentShamal SinghNo ratings yet

- Business Finance Week 2-3Document7 pagesBusiness Finance Week 2-3Luisa RadaNo ratings yet

- Kunjaw UasDocument11 pagesKunjaw UasIvan Katibul FaiziNo ratings yet

- Notes - FAR - InvestmentDocument7 pagesNotes - FAR - InvestmentElaineJrV-IgotNo ratings yet

- Chapter 11Document12 pagesChapter 11BharatSubramonyNo ratings yet

- Part 10 Foreign TranslationDocument3 pagesPart 10 Foreign TranslationKathlene BalicoNo ratings yet

- Across The Stars - Bridal EntranceDocument3 pagesAcross The Stars - Bridal EntrancehelenakbrittenNo ratings yet

- ACC 2024 Pre Board PDFDocument12 pagesACC 2024 Pre Board PDFKeshvi.No ratings yet

- 2010 - 2011 Marin Agricultural Land Trust Annual ReportDocument20 pages2010 - 2011 Marin Agricultural Land Trust Annual ReportMarin Agricultural Land TrustNo ratings yet

- Queueing Theory and Operations ManagementDocument11 pagesQueueing Theory and Operations ManagementMarthandeNo ratings yet

- Pakistan Gum and Chemicals Limited: Condensed Financial Statements For The 3rd 30, 201 Interim Quarter Ended September 7Document17 pagesPakistan Gum and Chemicals Limited: Condensed Financial Statements For The 3rd 30, 201 Interim Quarter Ended September 7Ameer Hamza ButtNo ratings yet

- FIN202 - Chap 3 - Selected ExercisesDocument2 pagesFIN202 - Chap 3 - Selected ExercisesThanh ThảoNo ratings yet

- Far Quiz 4Document6 pagesFar Quiz 4Shiela Jane CrismundoNo ratings yet

- Module 3Document22 pagesModule 3Noel S. De Juan Jr.No ratings yet

- Practice Exercise - Cairo - SolutionDocument3 pagesPractice Exercise - Cairo - SolutionfalconkudakwasheNo ratings yet

- Internal Control Affecting AssetsDocument27 pagesInternal Control Affecting AssetsJannefah Saglayan50% (2)

- Bahasa Inggris AkunDocument2 pagesBahasa Inggris AkunGaptek IDNo ratings yet

- Manson Incorporated Reported The Following Current Asset On ItsDocument1 pageManson Incorporated Reported The Following Current Asset On ItsCharlotteNo ratings yet

- What Is Goodwill?: Key TakeawaysDocument4 pagesWhat Is Goodwill?: Key TakeawaysTin PangilinanNo ratings yet

- Constellation Software Inc.: To Our ShareholdersDocument4 pagesConstellation Software Inc.: To Our ShareholdersrNo ratings yet

- Questions On Cash Flow StatementDocument5 pagesQuestions On Cash Flow StatementFaizSheikhNo ratings yet

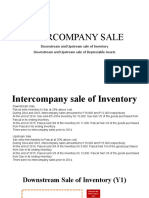

- Intercompany Sale: Downstream and Upstream Sale of Inventory Downstream and Upstream Sale of Depreciable AssetsDocument13 pagesIntercompany Sale: Downstream and Upstream Sale of Inventory Downstream and Upstream Sale of Depreciable AssetsShaina AragonNo ratings yet

- New FRA ASSIGNMENT 1Document3 pagesNew FRA ASSIGNMENT 1Suraj ApexNo ratings yet

- HOEC Investor Presentation 20 April 2017 Final ExecutiveDocument27 pagesHOEC Investor Presentation 20 April 2017 Final Executivedeba01234No ratings yet