You might also like

- Unit - 1 - Introduction Management AccountingDocument18 pagesUnit - 1 - Introduction Management AccountingKetan GuptaNo ratings yet

- Management Accounting WorkingDocument6 pagesManagement Accounting WorkingmohitNo ratings yet

- Management AccountingDocument30 pagesManagement AccountingDORAEMON MY JAANNo ratings yet

- Management Accounting - Unit1Document15 pagesManagement Accounting - Unit1anil gondNo ratings yet

- Management Versus Cost AccountingDocument1 pageManagement Versus Cost Accountingdebaditya_hit326634No ratings yet

- Name: Reg Number: Date of Submission: Lecturer in ChargeDocument2 pagesName: Reg Number: Date of Submission: Lecturer in ChargeIshmeal Nathaniel koromaNo ratings yet

- ch1 Managerial AccDocument4 pagesch1 Managerial AccAsad RehmanNo ratings yet

- 1&2 Lecture Fundamentals of AccountingDocument5 pages1&2 Lecture Fundamentals of Accountingzukhrufeman64No ratings yet

- Management Accounting Unit No 1st BBA 5th SemesterDocument4 pagesManagement Accounting Unit No 1st BBA 5th SemesterDrVivek SansonNo ratings yet

- 01 Fundamentals of Managerial Accounting and Ethical StandardsDocument10 pages01 Fundamentals of Managerial Accounting and Ethical StandardsXtian AmahanNo ratings yet

- Financial and Managerial AccountingDocument4 pagesFinancial and Managerial Accountingsonam agrawalNo ratings yet

- Management AccountingDocument11 pagesManagement AccountingGabriel BelmonteNo ratings yet

- 2 Zapya StatiscDocument10 pages2 Zapya StatiscLOND SONNo ratings yet

- Adv. Accountancy Paper-2Document17 pagesAdv. Accountancy Paper-2Avadhut PaymalleNo ratings yet

- Introduction FADocument28 pagesIntroduction FAShrestha MohantyNo ratings yet

- Management Accounting NotesDocument72 pagesManagement Accounting NotesALLU SRISAINo ratings yet

- Management AccountingDocument9 pagesManagement AccountingAman ChaudharyNo ratings yet

- 01 IntroductionDocument16 pages01 Introductionsushmita1999522No ratings yet

- L2 Management AccountingDocument23 pagesL2 Management Accountingvidisha sharmaNo ratings yet

- Managerial AccountingDocument5 pagesManagerial Accountingjaninemaeserpa14No ratings yet

- Management AccountingDocument108 pagesManagement AccountingBATUL ABBAS DEVASWALANo ratings yet

- Management Accounting - Notes.Document47 pagesManagement Accounting - Notes.mar231775No ratings yet

- Introduction Financial ManagementDocument21 pagesIntroduction Financial Managementabhijit prasadNo ratings yet

- Manonmaniam Sundaranar University: For More Information Visit: HTTP://WWW - Msuniv.ac - inDocument204 pagesManonmaniam Sundaranar University: For More Information Visit: HTTP://WWW - Msuniv.ac - inDhirendra Singh patwalNo ratings yet

- Management AccountingDocument20 pagesManagement AccountingAman ChaudharyNo ratings yet

- Introduction To Management Accounting: Learning ObjectivesDocument7 pagesIntroduction To Management Accounting: Learning ObjectivesMumbaiNo ratings yet

- Intro To MA Aug 2013Document14 pagesIntro To MA Aug 2013Nakul AnandNo ratings yet

- Financial AccountingDocument4 pagesFinancial AccountingnileshkambleNo ratings yet

- Financial Accounting and Cost AccountingDocument6 pagesFinancial Accounting and Cost AccountingdranilshindeNo ratings yet

- Projects Ma 1Document16 pagesProjects Ma 1nikkiNo ratings yet

- Management Accounting: S.K. Gupta Guest LecturerDocument37 pagesManagement Accounting: S.K. Gupta Guest LecturersantNo ratings yet

- Management Accounting: MBA First Year CR23Document28 pagesManagement Accounting: MBA First Year CR23Ajinkya NaikNo ratings yet

- Types of AccountingDocument6 pagesTypes of Accountingkhushnuma20No ratings yet

- Business Finance NewDocument7 pagesBusiness Finance NewFarhan Ashraf SaadNo ratings yet

- Accounts BDocument13 pagesAccounts Bzabi ullah MohammadiNo ratings yet

- Accounting and Financial Management Unit 1Document16 pagesAccounting and Financial Management Unit 1Palak JainNo ratings yet

- Financial Accounting (Notes)Document31 pagesFinancial Accounting (Notes)Riti Khandelwal100% (1)

- Management Accounting (MA)Document114 pagesManagement Accounting (MA)Shivangi Patel100% (1)

- Ica Afm 2022Document64 pagesIca Afm 2022Muhammed FayisNo ratings yet

- Accounts BDocument13 pagesAccounts Bzabi ullah MohammadiNo ratings yet

- Functions of Management AccountingDocument8 pagesFunctions of Management AccountingAbhishek Kumar100% (1)

- Financial AccountingDocument13 pagesFinancial AccountingSajad Ahmed Shah100% (1)

- Unit 1Document16 pagesUnit 1Rahul kumar100% (1)

- Management AccountingDocument135 pagesManagement Accountingdibakardas10017100% (1)

- Intro in Management AccountingDocument10 pagesIntro in Management AccountingGilvi Anne MaghopoyNo ratings yet

- Unit 3 Basant Kumar 22gsob2010021 AccountingDocument24 pagesUnit 3 Basant Kumar 22gsob2010021 AccountingRavi guptaNo ratings yet

- Financial AnalysisDocument30 pagesFinancial AnalysissrinivasanscribdNo ratings yet

- MC4104 - Unit 1Document13 pagesMC4104 - Unit 1Senthil KumarNo ratings yet

- New Microsoft Office Word Document-1Document73 pagesNew Microsoft Office Word Document-1Toshar JindalNo ratings yet

- Management Accounting OverviewDocument9 pagesManagement Accounting OverviewKanak ThackerNo ratings yet

- Name Kausar HanifDocument43 pagesName Kausar HanifIqra HanifNo ratings yet

- MBA-405 - Topic 4 - Management AccountantDocument4 pagesMBA-405 - Topic 4 - Management AccountantHanna Vi B. PolidoNo ratings yet

- Management AccountingDocument14 pagesManagement AccountingBristi SonowalNo ratings yet

- Management AccountingDocument13 pagesManagement AccountingPravin TejasNo ratings yet

- Introudction To Management Accounting RevisedDocument27 pagesIntroudction To Management Accounting RevisedraghbendrashahNo ratings yet

- Management Accounting Unit 1Document6 pagesManagement Accounting Unit 1Jay MehtaNo ratings yet

- Unit 1.introduction To Cost AccountingDocument2 pagesUnit 1.introduction To Cost AccountingClark Jamiel Luangco MartijaNo ratings yet

- Fa Class Notes UplodedDocument252 pagesFa Class Notes UplodedDurvas Karmarkar100% (1)

- MGM SyllabusDocument7 pagesMGM Syllabusస్వామియే శరణం అయ్యప్పNo ratings yet

- Project Profile & Estimated Cost of Pickle Unit Small Scale UnitDocument3 pagesProject Profile & Estimated Cost of Pickle Unit Small Scale Unitస్వామియే శరణం అయ్యప్పNo ratings yet

- Mango Pickles Manufacturing Business-842405 PDFDocument67 pagesMango Pickles Manufacturing Business-842405 PDFvellekat100% (1)

- MSMEDocument1 pageMSMEస్వామియే శరణం అయ్యప్పNo ratings yet

- AadarDocument2 pagesAadarస్వామియే శరణం అయ్యప్పNo ratings yet

- r16 Integrated Mba III SemesterDocument6 pagesr16 Integrated Mba III Semesterస్వామియే శరణం అయ్యప్పNo ratings yet

- Strategic Management 2010 NotesDocument15 pagesStrategic Management 2010 Notesస్వామియే శరణం అయ్యప్పNo ratings yet

- This Is To Certify That DRDocument1 pageThis Is To Certify That DRస్వామియే శరణం అయ్యప్పNo ratings yet

- Biz QuizDocument8 pagesBiz Quizస్వామియే శరణం అయ్యప్పNo ratings yet

- Unit 2 MSDocument8 pagesUnit 2 MSస్వామియే శరణం అయ్యప్పNo ratings yet

- Strategic ManagementDocument20 pagesStrategic Managementస్వామియే శరణం అయ్యప్పNo ratings yet

- Appsc GS Physics1Document3 pagesAppsc GS Physics1స్వామియే శరణం అయ్యప్పNo ratings yet

- Management Day 2013Document1 pageManagement Day 2013స్వామియే శరణం అయ్యప్పNo ratings yet

- Professional Ethics and Human ValuesDocument2 pagesProfessional Ethics and Human Valuesస్వామియే శరణం అయ్యప్పNo ratings yet

- Business EnvironmentDocument74 pagesBusiness EnvironmentPrashant Krishnan60% (5)

- Company Permission LetterDocument1 pageCompany Permission Letterస్వామియే శరణం అయ్యప్పNo ratings yet

- Capital and Revenue ExpenditureDocument17 pagesCapital and Revenue Expenditureస్వామియే శరణం అయ్యప్పNo ratings yet

- Ker61035 Appd Case01Document3 pagesKer61035 Appd Case01GeeSungNo ratings yet

- Name - Rounak Jain ROLL NO - 20194442 Business Law Assignment - 1Document2 pagesName - Rounak Jain ROLL NO - 20194442 Business Law Assignment - 1NAMAN PRAKASHNo ratings yet

- Business Viability CalculatorDocument3 pagesBusiness Viability CalculatorKiyo AiNo ratings yet

- BEGovSoc323 CSR 4Document24 pagesBEGovSoc323 CSR 4Romeo DupaNo ratings yet

- MBA Result 2014 16Document7 pagesMBA Result 2014 16SanaNo ratings yet

- Harga Poslaju Malaysia Domestic Commercial Non CommercialDocument2 pagesHarga Poslaju Malaysia Domestic Commercial Non CommercialZacke EsmaNo ratings yet

- Xavier University - Ateneo de Cagayan School of Business AdministrationDocument4 pagesXavier University - Ateneo de Cagayan School of Business AdministrationApril Mae DensingNo ratings yet

- Bbap2103 Akaun PengurusanDocument10 pagesBbap2103 Akaun PengurusanEima AbdullahNo ratings yet

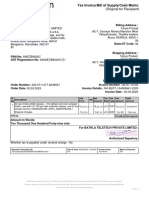

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Ganesh PrabuNo ratings yet

- Network Infrastructure PresentationDocument13 pagesNetwork Infrastructure PresentationonyinowNo ratings yet

- Form Restoran Sederhana Masakan PadangDocument30 pagesForm Restoran Sederhana Masakan PadangLuthfi's Mzakki'sNo ratings yet

- Strategic Management ModelsDocument24 pagesStrategic Management ModelsAnubhav DubeyNo ratings yet

- Case 15 Pacific Healthcare - B - Student - 6th EditionDocument1 pageCase 15 Pacific Healthcare - B - Student - 6th EditionAhmed MahmoudNo ratings yet

- Students Satisfaction On The Services Provided by The School Canteens in Catanduanes State UniversityDocument31 pagesStudents Satisfaction On The Services Provided by The School Canteens in Catanduanes State UniversityAnthony HeartNo ratings yet

- Poliform Kitchens Aust (855KB) PDFDocument12 pagesPoliform Kitchens Aust (855KB) PDFsage_9290% (1)

- CASESTUDYDocument21 pagesCASESTUDYLouise Lopez AlbisNo ratings yet

- Braytron Catalogue 2019 PDFDocument174 pagesBraytron Catalogue 2019 PDFLiviu Cioroianu0% (1)

- Business Basics Test: Please Complete This Puzzle by Finding The Hidden WordsDocument1 pageBusiness Basics Test: Please Complete This Puzzle by Finding The Hidden WordsCavene ScottNo ratings yet

- What Are Key Performance IndicatorsDocument13 pagesWhat Are Key Performance IndicatorsKharieh Comb's100% (1)

- De Guzman V de DiosDocument4 pagesDe Guzman V de DiosJulius Carmona GregoNo ratings yet

- HBX 6516DS VTMDocument2 pagesHBX 6516DS VTMRoma Zurita100% (1)

- 1 Zong Net Package PDFDocument8 pages1 Zong Net Package PDFHafiz Abid Malik0% (1)

- Threat and Risk Assessment TemplateDocument30 pagesThreat and Risk Assessment TemplateMarija PetkovicNo ratings yet

- Mid Term Exam 1 - Fall 2018-799Document3 pagesMid Term Exam 1 - Fall 2018-799abdirahmanNo ratings yet

- InvoiceDocument1 pageInvoicetanya.prasadNo ratings yet

- Betterworks Goal Setting Ebook PDFDocument13 pagesBetterworks Goal Setting Ebook PDFArtur Furtado100% (3)

- Sap DMSDocument17 pagesSap DMSRahul Gaikwad100% (1)

- RPT Case DigestsDocument71 pagesRPT Case Digestscarlota ann lafuenteNo ratings yet

- Exercise Books EthiopiaDocument23 pagesExercise Books EthiopiaDilip Kumar Ladwa100% (3)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageFrom EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageRating: 4.5 out of 5 stars4.5/5 (109)

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)From EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Rating: 4.5 out of 5 stars4.5/5 (24)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 5 out of 5 stars5/5 (13)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet