You might also like

- 5 Mercantile Law Bar Questions and Answers (2007-2017) PDFDocument146 pages5 Mercantile Law Bar Questions and Answers (2007-2017) PDFAngelica Fojas Rañola100% (6)

- 2019 Ateneo Pre Week Commercial LawDocument87 pages2019 Ateneo Pre Week Commercial Lawfreegalado100% (5)

- UP Legal Ethics Pre WeekDocument16 pagesUP Legal Ethics Pre WeekWorstWitch TalaNo ratings yet

- 2009-2019 Mercantile Bar Questions OnlyDocument143 pages2009-2019 Mercantile Bar Questions OnlyMeg VillaricaNo ratings yet

- 2019 Ateneo Pre Week Labor PDFDocument88 pages2019 Ateneo Pre Week Labor PDFDiding BorromeoNo ratings yet

- Final Part2 2019 Abad Labor Pre-Week Notes 100319Document57 pagesFinal Part2 2019 Abad Labor Pre-Week Notes 100319Liavel Badillo75% (4)

- Manual de Generadores de Gas SolarDocument49 pagesManual de Generadores de Gas SolarJuvenal Segundo Chavez Acosta100% (7)

- Enercalc ManualDocument608 pagesEnercalc Manualrekstrom0% (1)

- Batch ManagementDocument166 pagesBatch ManagementMalik ImtiyazNo ratings yet

- Quamto Taxation Law 2017Document34 pagesQuamto Taxation Law 2017Anonymous MCsSDJ100% (6)

- ESTATE TAX PLANNINGDocument50 pagesESTATE TAX PLANNINGCedric VanguardiaNo ratings yet

- 2019 Ateneo Pre Week Taxation PDFDocument60 pages2019 Ateneo Pre Week Taxation PDFfreegalado100% (4)

- 2019 Ust Pre Week Taxation LawDocument36 pages2019 Ust Pre Week Taxation Lawdublin80% (20)

- UST Mercantile Law Reviewer 2016Document413 pagesUST Mercantile Law Reviewer 2016mc.rockz1475% (4)

- Ethics QuamtoDocument33 pagesEthics QuamtoSan Tabugan100% (3)

- Beda TaxDocument287 pagesBeda TaxJul A.100% (1)

- Criminal Law Jurisprudence 2019 by Prof. Modesto Ticman, Jr.Document45 pagesCriminal Law Jurisprudence 2019 by Prof. Modesto Ticman, Jr.Nashiba Dida-AgunNo ratings yet

- Taxation Law Bar Questions & Answers: Submitted By: BALUYUT, Maria Corazon de Leon, Dino GADOR, Ken Reyes SUCGANG, JustinDocument8 pagesTaxation Law Bar Questions & Answers: Submitted By: BALUYUT, Maria Corazon de Leon, Dino GADOR, Ken Reyes SUCGANG, JustinKen Reyes GadorNo ratings yet

- Preweek - Labor Law - Atty Benedict G. Kato - REDUCED BAR COVERAGEDocument53 pagesPreweek - Labor Law - Atty Benedict G. Kato - REDUCED BAR COVERAGEYsa Tabbu100% (1)

- 2021bar Bqas Not Affected by Amended Rule On Civil Procedure and EvidenceDocument66 pages2021bar Bqas Not Affected by Amended Rule On Civil Procedure and EvidenceRaz SabulaoNo ratings yet

- Mercantile Law Bar Questions (1990-2013)Document61 pagesMercantile Law Bar Questions (1990-2013)Frances Anne Gamboa100% (4)

- Bar Civil Nptes 2022Document10 pagesBar Civil Nptes 2022Tin Tin0% (1)

- Mockbar Civillaw CruzDocument20 pagesMockbar Civillaw CruzCarlo CastilloNo ratings yet

- 01 Legal Edge 2018 PreWeek - PoliticalDocument27 pages01 Legal Edge 2018 PreWeek - PoliticalJustin ParasNo ratings yet

- Commercial Law Bar Q - A (2017-2019) (4D1920)Document51 pagesCommercial Law Bar Q - A (2017-2019) (4D1920)Sage Lingatong50% (2)

- MEMORANDUM CIRCULARS MUST REMAIN CONSISTENT WITH LAWDocument16 pagesMEMORANDUM CIRCULARS MUST REMAIN CONSISTENT WITH LAWperlitainocencioNo ratings yet

- CRALaw - Labor Law PreWeek (2017)Document157 pagesCRALaw - Labor Law PreWeek (2017)freegalado91% (22)

- 2019 Mercantile ReviewerDocument203 pages2019 Mercantile Reviewerrobertoii_suarez100% (2)

- UST Mercantile Law QuAMTO 2017Document112 pagesUST Mercantile Law QuAMTO 2017mtabcao86% (7)

- Taxation Principles Review ProblemsDocument79 pagesTaxation Principles Review ProblemsArya CollinNo ratings yet

- Commercial Law Review Justice DimaampaoDocument19 pagesCommercial Law Review Justice DimaampaoMegan MateoNo ratings yet

- Philippine Civil Law Bar Exam QuestionsDocument14 pagesPhilippine Civil Law Bar Exam QuestionsDanilo Magallanes SampagaNo ratings yet

- Preweek HO No 7 Remedial Law PDFDocument32 pagesPreweek HO No 7 Remedial Law PDFRishel TubogNo ratings yet

- Red Notes: Mercantile LawDocument36 pagesRed Notes: Mercantile Lawjojitus100% (2)

- Taxation TaxDocument89 pagesTaxation TaxTonifranz SarenoNo ratings yet

- Tax Updates by Atty. Riza LumberaDocument75 pagesTax Updates by Atty. Riza Lumberadmad_shayne50% (2)

- Sandoval Political Review Notes EditedDocument134 pagesSandoval Political Review Notes EditedPearl Angeli Quisido CanadaNo ratings yet

- Criminal Law Review Notes - Dean Carlos OrtegaDocument121 pagesCriminal Law Review Notes - Dean Carlos OrtegaLex Talionis Fraternitas100% (1)

- 4 - Taxation Law - Green Notes PDFDocument104 pages4 - Taxation Law - Green Notes PDFshhhgNo ratings yet

- Political Law Reviewer Bar 2019 Part 1 V 20 by Atty. Alexis Medina ACADEMICUSDocument27 pagesPolitical Law Reviewer Bar 2019 Part 1 V 20 by Atty. Alexis Medina ACADEMICUSalyamarrabeNo ratings yet

- Discussion On Conflict of LAws by AgpaloDocument186 pagesDiscussion On Conflict of LAws by AgpaloJurilBrokaPatiñoNo ratings yet

- Civ QuamtoDocument72 pagesCiv QuamtoSan Tabugan100% (4)

- Bar Exam Preparations STeM 2nd Edition May 11 2020Document28 pagesBar Exam Preparations STeM 2nd Edition May 11 2020Agui S. T. Pad100% (1)

- 2018 Mercantile Law Suggested Answer (Incomplete)Document10 pages2018 Mercantile Law Suggested Answer (Incomplete)Victoria Denise Monte80% (5)

- UST QuAMTO Mercantile Law 2017Document112 pagesUST QuAMTO Mercantile Law 2017Gepcars FlouramieNo ratings yet

- Labor Quamto 2016Document63 pagesLabor Quamto 2016Ann HopeloveNo ratings yet

- Taxation Law 2: Case DigestDocument155 pagesTaxation Law 2: Case DigestLala ManzanoNo ratings yet

- 2022 Leb Bar Bulletin No. 31, S. 2022 TaxationDocument296 pages2022 Leb Bar Bulletin No. 31, S. 2022 TaxationCzarina Joy Pena75% (4)

- Tax2 Bar Qs CompiledDocument10 pagesTax2 Bar Qs CompiledDaisyKeith VinesNo ratings yet

- AssignmentDocument2 pagesAssignmentLois JoseNo ratings yet

- Tax 1 Mock BarDocument8 pagesTax 1 Mock BarMarco RvsNo ratings yet

- Taxation Law Mock BarDocument8 pagesTaxation Law Mock BarKC ManglapusNo ratings yet

- Commercial Property Tax AdviceDocument4 pagesCommercial Property Tax AdviceTom BinfieldNo ratings yet

- 2016-2017 TAX 1 Quiz 2Document5 pages2016-2017 TAX 1 Quiz 2Miko TabandaNo ratings yet

- Western Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Document2 pagesWestern Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Marc William SorianoNo ratings yet

- 3)Document4 pages3)Tom BinfieldNo ratings yet

- 1)Document2 pages1)Tom BinfieldNo ratings yet

- Final Exam in Tax I (2020-2021) QuestionnaireDocument4 pagesFinal Exam in Tax I (2020-2021) QuestionnaireMarc William SorianoNo ratings yet

- Tax Review Take Home Quiz Considered RecitationDocument9 pagesTax Review Take Home Quiz Considered RecitationAlgen S. GomezNo ratings yet

- Income Tax Bar QuestionsDocument19 pagesIncome Tax Bar QuestionsBuddy Brylle YbanezNo ratings yet

- Taxation Law Bar 2007-2013Document215 pagesTaxation Law Bar 2007-2013kent_009No ratings yet

- TAX BAR Qs With AnswersDocument10 pagesTAX BAR Qs With AnswersJanila BajuyoNo ratings yet

- Years Ago at P 500, 000 With FMV at Date of Donation Equal To P 600, 000 But With Unpaid Mortgage of P 50, 000 Assumed by The Donee?Document4 pagesYears Ago at P 500, 000 With FMV at Date of Donation Equal To P 600, 000 But With Unpaid Mortgage of P 50, 000 Assumed by The Donee?Prince PierreNo ratings yet

- Aznar Vs GarciaDocument1 pageAznar Vs Garciamar corNo ratings yet

- Case DigestsDocument8 pagesCase DigestsVanessa May GaNo ratings yet

- Why I Want To Be A LawyerDocument2 pagesWhy I Want To Be A LawyerVanessa May GaNo ratings yet

- Saudi Airlines vs CA: Philippines Law Governs Flight Attendant's LawsuitDocument1 pageSaudi Airlines vs CA: Philippines Law Governs Flight Attendant's LawsuitVanessa May GaNo ratings yet

- AssignmentDocument1 pageAssignmentVanessa May GaNo ratings yet

- Partnership 2020 SyllabusDocument6 pagesPartnership 2020 SyllabusVanessa May GaNo ratings yet

- B and HDocument3 pagesB and HVanessa May GaNo ratings yet

- Liability of Partnership To Third Persons For Acts of PartnersDocument1 pageLiability of Partnership To Third Persons For Acts of PartnersVanessa May GaNo ratings yet

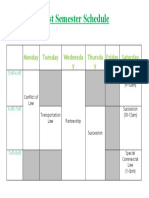

- First Semester ScheduleDocument1 pageFirst Semester ScheduleVanessa May GaNo ratings yet

- Beneficiality-Te ChiDocument1 pageBeneficiality-Te ChiVanessa May GaNo ratings yet

- Rules On ManagementDocument2 pagesRules On ManagementVanessa May GaNo ratings yet

- Syllabus SuccessionDocument1 pageSyllabus SuccessionVanessa May GaNo ratings yet

- ScratchDocument2 pagesScratchVanessa May GaNo ratings yet

- Liability of Partnership To Third Persons For Acts of PartnersDocument1 pageLiability of Partnership To Third Persons For Acts of PartnersVanessa May GaNo ratings yet

- Necessity InterpellationDocument1 pageNecessity InterpellationVanessa May GaNo ratings yet

- FAQsDocument2 pagesFAQsVanessa May GaNo ratings yet

- Rules on Distribution of Profits & LossesDocument2 pagesRules on Distribution of Profits & LossesVanessa May GaNo ratings yet

- LIBRT: Online Lending Should Be Regulated by The Bangko Sentral NG Pilipinas Governing LawsDocument2 pagesLIBRT: Online Lending Should Be Regulated by The Bangko Sentral NG Pilipinas Governing LawsVanessa May GaNo ratings yet

- LIBRTDocument1 pageLIBRTVanessa May GaNo ratings yet

- LAVANDocument1 pageLAVANVanessa May GaNo ratings yet

- After Mock Debate PointsDocument1 pageAfter Mock Debate PointsVanessa May GaNo ratings yet

- Semester TitleDocument1 pageSemester TitleVanessa May GaNo ratings yet

- Necessity InterpellationDocument1 pageNecessity InterpellationVanessa May GaNo ratings yet

- Crim Pro - FE (2019)Document4 pagesCrim Pro - FE (2019)Vanessa May GaNo ratings yet

- Civ Pro - Last CaseDocument10 pagesCiv Pro - Last CaseVanessa May GaNo ratings yet

- Banks On Second-Endorsed Checks Accept or Not?Document3 pagesBanks On Second-Endorsed Checks Accept or Not?Vanessa May GaNo ratings yet

- Labor Relations Final Exam 2020Document9 pagesLabor Relations Final Exam 2020Vanessa May GaNo ratings yet

- November 11Document1 pageNovember 11Vanessa May GaNo ratings yet

- November 12Document1 pageNovember 12Vanessa May GaNo ratings yet

- Civ Pro - Case DigestsDocument8 pagesCiv Pro - Case DigestsVanessa May GaNo ratings yet

- Fall 22-23 COA Lecture-5 Processor Status & FLAGS RegisterDocument25 pagesFall 22-23 COA Lecture-5 Processor Status & FLAGS RegisterFaysal Ahmed SarkarNo ratings yet

- Accenture The Long View of The Chip ShortageDocument20 pagesAccenture The Long View of The Chip ShortageOso genialNo ratings yet

- STIPULATION To Stay ProceedingsDocument7 pagesSTIPULATION To Stay Proceedingsjamesosborne77-1No ratings yet

- Pri Dlbt1201182enDocument2 pagesPri Dlbt1201182enzaheerNo ratings yet

- Five ForcesDocument2 pagesFive ForcesJavaid NasirNo ratings yet

- CS3352 - Digital Principles and Computer Organization LaboratoryDocument55 pagesCS3352 - Digital Principles and Computer Organization Laboratoryakshaya vijay100% (6)

- Document Name: A.5 Information Security PoliciesDocument3 pagesDocument Name: A.5 Information Security PoliciesBhavana certvalueNo ratings yet

- De La Salle University College of Business Course Checklist: Basirec SystandDocument2 pagesDe La Salle University College of Business Course Checklist: Basirec SystandncllpdllNo ratings yet

- Isolating Antagonistic BacteriaDocument12 pagesIsolating Antagonistic BacteriaDesy rianitaNo ratings yet

- ToshibaDocument38 pagesToshibadvishal77No ratings yet

- PPT 06Document15 pagesPPT 06Diaz Hesron Deo SimorangkirNo ratings yet

- Laporan Tahunan 2009Document179 pagesLaporan Tahunan 2009zalifahshafieNo ratings yet

- Perspective View: This SiteDocument1 pagePerspective View: This SiteRose Lind TubogNo ratings yet

- Sirius-4 4 29-Manual PDFDocument49 pagesSirius-4 4 29-Manual PDFJovanderson JacksonNo ratings yet

- Refregeration & Airconditioning 2011-2012Document29 pagesRefregeration & Airconditioning 2011-2012erastus shipaNo ratings yet

- Write Your Own Song with SameDiffDocument2 pagesWrite Your Own Song with SameDiffSyed A H AndrabiNo ratings yet

- 5.1.2.8 Lab - Viewing Network Device MAC AddressesDocument5 pages5.1.2.8 Lab - Viewing Network Device MAC Addresseschristian hallNo ratings yet

- BSI ISOIEC27001 Assessment Checklist UK enDocument3 pagesBSI ISOIEC27001 Assessment Checklist UK enDanushkaPereraNo ratings yet

- Multi-User Collaboration With Revit WorksetsDocument10 pagesMulti-User Collaboration With Revit WorksetsRafael Rafael CastilloNo ratings yet

- Checklist Whitepaper EDocument3 pagesChecklist Whitepaper EMaria FachiridouNo ratings yet

- 341 Examples of Addressing ModesDocument8 pages341 Examples of Addressing ModesdurvasikiranNo ratings yet

- Silo - Tips Chapter 12 Sonic Logs Lecture Notes For Pet 370 Spring 2012 Prepared by Thomas W Engler PHD PeDocument21 pagesSilo - Tips Chapter 12 Sonic Logs Lecture Notes For Pet 370 Spring 2012 Prepared by Thomas W Engler PHD PeIntanNurDaniaNo ratings yet

- A320 LTS Rev 6 13 02 26Document2 pagesA320 LTS Rev 6 13 02 26Peps Peps PepsNo ratings yet

- Managerial Accounting Decision Making and Motivating Performance 1st Edition Datar Rajan Test BankDocument46 pagesManagerial Accounting Decision Making and Motivating Performance 1st Edition Datar Rajan Test Bankmable100% (18)

- Advantages and Disadvantages of NanotechnologyDocument31 pagesAdvantages and Disadvantages of NanotechnologyMaribel Tan-Losloso Nayad100% (4)

- Company Profile: Our BeginningDocument1 pageCompany Profile: Our BeginningSantoshPaul CleanlandNo ratings yet

- Dan Fue Leung v. IACDocument2 pagesDan Fue Leung v. IACCedricNo ratings yet