You might also like

- Inter Psak 25Document28 pagesInter Psak 25vincent alvinNo ratings yet

- Faktor yang Mempengaruhi Audit Delay pada Perusahaan Consumer GoodDocument17 pagesFaktor yang Mempengaruhi Audit Delay pada Perusahaan Consumer GoodandrianyuniNo ratings yet

- Identifying and Journalizing Transactions: Learning OutcomesDocument51 pagesIdentifying and Journalizing Transactions: Learning OutcomesTip Tap100% (1)

- Soal Myob PT DinamikaDocument5 pagesSoal Myob PT DinamikaRaden Andini AnggreaniNo ratings yet

- Beams11 ppt04Document49 pagesBeams11 ppt04Rika RieksNo ratings yet

- Week 3 - Chap 2-Collaboration, Interpersonal Communication and Business Etiquette Bovee - Ebc12 - Inppt - 02Document37 pagesWeek 3 - Chap 2-Collaboration, Interpersonal Communication and Business Etiquette Bovee - Ebc12 - Inppt - 02qwertyuiopNo ratings yet

- Analisis Rasio Keuangan: Rasio Profitabilitas Rasio SolvencyDocument11 pagesAnalisis Rasio Keuangan: Rasio Profitabilitas Rasio SolvencyFrans KristianNo ratings yet

- Chapter 2 - Understanding StrategiesDocument31 pagesChapter 2 - Understanding StrategiesSarah Laras WitaNo ratings yet

- Teori AkunDocument12 pagesTeori AkunErditama GeryNo ratings yet

- Beams11 Ppt10 EDITDocument46 pagesBeams11 Ppt10 EDITAgoeng Susanto BrajewoNo ratings yet

- Intermediate Accounting IFRS Edition: Kieso, Weygandt, WarfieldDocument29 pagesIntermediate Accounting IFRS Edition: Kieso, Weygandt, Warfielddystopian au.No ratings yet

- Beams10e - Ch08 Changes in Ownership InterestDocument42 pagesBeams10e - Ch08 Changes in Ownership InterestBayoe AjipNo ratings yet

- Kieso - Inter - Ch20 - IfRS (Pensions)Document47 pagesKieso - Inter - Ch20 - IfRS (Pensions)hidaNo ratings yet

- Laporan Keuangan Ace Hardware 2018 PDFDocument82 pagesLaporan Keuangan Ace Hardware 2018 PDFBang BegsNo ratings yet

- Case Study 1 v.3 PDFDocument21 pagesCase Study 1 v.3 PDFAce DesabilleNo ratings yet

- Advanced Acct PP CH08Document42 pagesAdvanced Acct PP CH08Jose TNo ratings yet

- Foreword: Financial Auditing 1 - 9 Edition - 1Document37 pagesForeword: Financial Auditing 1 - 9 Edition - 1meyyNo ratings yet

- Isa 300Document5 pagesIsa 300sabeen ansariNo ratings yet

- Reengineering Business Process To Improve Responsiveness: Accounting For TimeDocument17 pagesReengineering Business Process To Improve Responsiveness: Accounting For TimediahNo ratings yet

- Concise SEO-Optimized Title for a Document on Social and Cultural NormsDocument70 pagesConcise SEO-Optimized Title for a Document on Social and Cultural Normsmillie MutiaNo ratings yet

- Astra International: IndonesiaDocument7 pagesAstra International: Indonesiaalvin maulana.pNo ratings yet

- ALTO ALTO Annual ReportDocument120 pagesALTO ALTO Annual Reportputhreerhy100% (3)

- Case 15-5 Xerox Corporation RecommendationsDocument6 pagesCase 15-5 Xerox Corporation RecommendationsgabrielyangNo ratings yet

- Chapter 14Document19 pagesChapter 14Anonymous Yo03tioNo ratings yet

- Materi Bahasa Inggris BisnisDocument5 pagesMateri Bahasa Inggris BisnisIrma WatiNo ratings yet

- Chapter 3 - Behavior in OrganizationsDocument20 pagesChapter 3 - Behavior in OrganizationsSarah Laras Wita100% (2)

- 2017 Annual Report - PT Graha Layar Prima TBK PDFDocument220 pages2017 Annual Report - PT Graha Layar Prima TBK PDFKevin D'ShōnenNo ratings yet

- Record To Report (R2R) Best Practices: Report (R2R) Process Is Used To Collect, Organize, and Analyze Your Company'sDocument11 pagesRecord To Report (R2R) Best Practices: Report (R2R) Process Is Used To Collect, Organize, and Analyze Your Company'sManna MahadiNo ratings yet

- Case Study - Starbucks TeamworkDocument3 pagesCase Study - Starbucks TeamworkMateusz JuszczykowskiNo ratings yet

- EB Hall Sw11 ITAudit3 WMDocument657 pagesEB Hall Sw11 ITAudit3 WMRheaMaeBranzuelaNo ratings yet

- Case 6.2Document5 pagesCase 6.2Azhar KanedyNo ratings yet

- Hansen AISE IM Ch08Document54 pagesHansen AISE IM Ch08AimanNo ratings yet

- TUTORIAL SOLUTIONS (Week 4A)Document8 pagesTUTORIAL SOLUTIONS (Week 4A)Peter100% (1)

- Soal Siklus AkuntansiDocument10 pagesSoal Siklus AkuntansiAlfin Dwi SaptaNo ratings yet

- Agrs Annual Report 2016Document163 pagesAgrs Annual Report 2016Dzulfaqor Tanzil ArifinNo ratings yet

- Beams11 Ppt07 Obligasi NewDocument28 pagesBeams11 Ppt07 Obligasi Newarfian0% (1)

- Chapter 13: Foreign Currency Financial Statements: Advanced AccountingDocument42 pagesChapter 13: Foreign Currency Financial Statements: Advanced AccountingMad JayaNo ratings yet

- Arens14e ch07 PPTDocument43 pagesArens14e ch07 PPTNindya Harum SolichaNo ratings yet

- Akuntansi Keuangan 2: Pertemuan 1Document72 pagesAkuntansi Keuangan 2: Pertemuan 1Monita nababanNo ratings yet

- Reporting Standards Impact Company AssetsDocument8 pagesReporting Standards Impact Company AssetsAqsa ButtNo ratings yet

- Chapter 12: Derivatives and Foreign Currency Transactions: Advanced AccountingDocument52 pagesChapter 12: Derivatives and Foreign Currency Transactions: Advanced AccountingindahmuliasariNo ratings yet

- ADHI - Annual Report - 2017 PDFDocument222 pagesADHI - Annual Report - 2017 PDFYulia FitriNo ratings yet

- Arens Solution Manual Chapter 3Document37 pagesArens Solution Manual Chapter 3Rizal Pandu NugrohoNo ratings yet

- Overall Audit Plan and Audit Program: ©2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/BeasleyDocument36 pagesOverall Audit Plan and Audit Program: ©2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/BeasleydindaadaniNo ratings yet

- (PDF) Jawaban Kasus Bab 9Document26 pages(PDF) Jawaban Kasus Bab 9Shinning Nunaa45No ratings yet

- Chapter 1-Solution To ProblemsDocument7 pagesChapter 1-Solution To ProblemsawaisjinnahNo ratings yet

- MAGP Annual Report 2017Document86 pagesMAGP Annual Report 2017cindytantrianiNo ratings yet

- Budgeting and Ethics Delma Company Manufactures A Variety ofDocument1 pageBudgeting and Ethics Delma Company Manufactures A Variety oftrilocksp SinghNo ratings yet

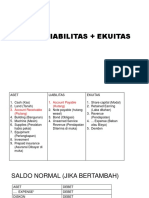

- Persamaan Dasar AkuntansiDocument10 pagesPersamaan Dasar Akuntansiapelina teresia100% (1)

- Tugas Kelompok - Corporate Financial Management.Document4 pagesTugas Kelompok - Corporate Financial Management.AgusSetiawanNo ratings yet

- Ch8 000Document83 pagesCh8 000khawarsherNo ratings yet

- PT Sepatu Bata Financial Analysis and 2008 Financial CrisisDocument6 pagesPT Sepatu Bata Financial Analysis and 2008 Financial CrisisOlim BariziNo ratings yet

- CH 03 Financial Statements ExercisesDocument39 pagesCH 03 Financial Statements ExercisesJocelyneKarolinaArriagaRangel100% (1)

- Perbandingan PSAK DGN IFRS Menurut DeloitteDocument0 pagesPerbandingan PSAK DGN IFRS Menurut Deloittete_menNo ratings yet

- Audit of The Capital Acquisition and Repayment CycleDocument30 pagesAudit of The Capital Acquisition and Repayment CycleLouis ValentinoNo ratings yet

- Kolom Inventory CardDocument1 pageKolom Inventory CardargarinirizqiayuNo ratings yet

- UTS SPM - Salman Hafidz Iriansyah - 120620170003Document13 pagesUTS SPM - Salman Hafidz Iriansyah - 120620170003Rizal AlfianNo ratings yet

- BSDE Annual Report 2018Document38 pagesBSDE Annual Report 2018Furqon MuhammadNo ratings yet

- Accounting CycleDocument4 pagesAccounting CycleAmitNo ratings yet

- Far - Nica TomitaDocument3 pagesFar - Nica TomitaMikayNo ratings yet

- Module 1 Engineering EconomicsDocument34 pagesModule 1 Engineering EconomicsSINGIAN, Alcein D.No ratings yet

- Joint Venture Between Tata and ZaraDocument4 pagesJoint Venture Between Tata and ZaraShrishti Agarwal100% (1)

- Opportunities Weight Rating Weighted Score: Chosen Opportunity: Chosen ThreatDocument8 pagesOpportunities Weight Rating Weighted Score: Chosen Opportunity: Chosen ThreatUmbertoNo ratings yet

- Consumer Awareness ProjectDocument3 pagesConsumer Awareness ProjectBincy CherianNo ratings yet

- Reaction Paper ADIDASDocument2 pagesReaction Paper ADIDASShin WalkerNo ratings yet

- Financial Literacy SACCO ManualDocument38 pagesFinancial Literacy SACCO ManualMukalele RogersNo ratings yet

- British Steel Interactive Stock Range GuideDocument86 pagesBritish Steel Interactive Stock Range GuideLee Hing WahNo ratings yet

- Understanding Rwanda Agribusiness and Manufacturing SeDocument258 pagesUnderstanding Rwanda Agribusiness and Manufacturing Seooty.pradeepNo ratings yet

- Tourism Policy of Malta 2007-2011: Francis Zammit Dimech Minister For Tourism and CultureDocument11 pagesTourism Policy of Malta 2007-2011: Francis Zammit Dimech Minister For Tourism and Cultureნინი მახარაძეNo ratings yet

- VAT Codal and RegulationsDocument6 pagesVAT Codal and RegulationsVictor LimNo ratings yet

- The Billabong CaseDocument14 pagesThe Billabong CaseRati Sinha100% (1)

- LE-TRA - Config Guide For Shipment & Shipment Cost Document - Part IIIDocument20 pagesLE-TRA - Config Guide For Shipment & Shipment Cost Document - Part IIIАвишек СенNo ratings yet

- Dsr April 2024Document10 pagesDsr April 2024vapatel767No ratings yet

- Jwi 530 Assignment 4Document3 pagesJwi 530 Assignment 4gadisika0% (1)

- Case Studies For Acc2Document2 pagesCase Studies For Acc2jtNo ratings yet

- 3 AlibabaDocument24 pages3 AlibabaADAM LOW0% (1)

- Syllabus B7345-001 Entrepreneurial FinanceDocument7 pagesSyllabus B7345-001 Entrepreneurial FinanceTrang TranNo ratings yet

- Exercises - Topic 3 (Impairment) (Eng)Document7 pagesExercises - Topic 3 (Impairment) (Eng)Thảo PhạmNo ratings yet

- Salary StructureDocument1 pageSalary Structureomer farooqNo ratings yet

- Barcelona PDFDocument165 pagesBarcelona PDFHector Alberto Garcia LopezNo ratings yet

- ProspectusDocument2 pagesProspectusJuliana Mae FradesNo ratings yet

- "Study of Different Loans Provided by SBI Bank": Project Report ONDocument55 pages"Study of Different Loans Provided by SBI Bank": Project Report ONAnonymous g7uPednINo ratings yet

- ACCT 434 Midterm Exam (Updated)Document4 pagesACCT 434 Midterm Exam (Updated)DeVryHelpNo ratings yet

- The Graduates of Bachelor of Science in Criminology of Collegio de Amore SY 2010 To 2018 A Tracer StudyDocument11 pagesThe Graduates of Bachelor of Science in Criminology of Collegio de Amore SY 2010 To 2018 A Tracer Studyjetlee estacionNo ratings yet

- Strategy - RBI Grade - B - Officer-2016 by RBI Topper Manojkumar EDocument23 pagesStrategy - RBI Grade - B - Officer-2016 by RBI Topper Manojkumar EAbhijit Konwar100% (1)

- MOSP Final Project - ITC - Group7 - SectionCDocument29 pagesMOSP Final Project - ITC - Group7 - SectionCArjun JainNo ratings yet

- CBMEC 1 - Assignment 3Document4 pagesCBMEC 1 - Assignment 3Tibay, Genevive Angel Anne A.No ratings yet

- Accounting For Income Taxes: About This Chapter!Document9 pagesAccounting For Income Taxes: About This Chapter!sabithpaulNo ratings yet

- Honda Balance SheetDocument2 pagesHonda Balance Sheetmeri4uNo ratings yet

- PDF To WordDocument17 pagesPDF To WordMehulsonariaNo ratings yet