You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- 8.) Republic V ManaloDocument3 pages8.) Republic V Manaloangela100% (1)

- Case Digest - City of Batangas v. Philippine Shell Petroleum CorporationDocument12 pagesCase Digest - City of Batangas v. Philippine Shell Petroleum CorporationKatrina ManluluNo ratings yet

- Batangas City vs. Pilipinas Shell Corp G.R. No. 195003Document11 pagesBatangas City vs. Pilipinas Shell Corp G.R. No. 195003Mike E DmNo ratings yet

- 6.) Corpuz V St. Tomas PDFDocument2 pages6.) Corpuz V St. Tomas PDFangelaNo ratings yet

- Sarmiento V IacDocument5 pagesSarmiento V IacangelaNo ratings yet

- Negative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsDocument5 pagesNegative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsangelaNo ratings yet

- Negative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsDocument5 pagesNegative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsangelaNo ratings yet

- Negative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsDocument5 pagesNegative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsangelaNo ratings yet

- Negative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsDocument5 pagesNegative Opposite Doctrine - What Is Expressed Puts An End To What Is Implied IsangelaNo ratings yet

- Property Case Digest Water CodeDocument11 pagesProperty Case Digest Water CodeMonica Morante100% (1)

- Rustia Vs Court of First InstanceDocument3 pagesRustia Vs Court of First InstanceangelaNo ratings yet

- PROHIBITIONSDocument8 pagesPROHIBITIONSangelaNo ratings yet

- Angeles Vs Lina-AcDocument3 pagesAngeles Vs Lina-AcangelaNo ratings yet

- Siochi V Gozon PDFDocument7 pagesSiochi V Gozon PDFangelaNo ratings yet

- Maxey V CaDocument7 pagesMaxey V CaangelaNo ratings yet

- Abing V Waeyan PDFDocument5 pagesAbing V Waeyan PDFangelaNo ratings yet

- Aro Vs NanawaDocument11 pagesAro Vs NanawaangelaNo ratings yet

- Constitutional Law II - CASESDocument21 pagesConstitutional Law II - CASESangelaNo ratings yet

- Petitioner Vs Vs Respondent: Second DivisionDocument5 pagesPetitioner Vs Vs Respondent: Second DivisionChristian VillarNo ratings yet

- Ayala V CaDocument8 pagesAyala V CaangelaNo ratings yet

- Ching Vs CADocument5 pagesChing Vs CARonnieEnggingNo ratings yet

- Tumlos V FernandezDocument9 pagesTumlos V FernandezangelaNo ratings yet

- Uy V CaDocument6 pagesUy V CaRose AnnNo ratings yet

- Petitioner Vs Vs Respondent: Second DivisionDocument5 pagesPetitioner Vs Vs Respondent: Second DivisionChristian VillarNo ratings yet

- Energy Investment Opportunities 2019Document51 pagesEnergy Investment Opportunities 2019Marce MangaoangNo ratings yet

- PDD03 MitubishiDocument68 pagesPDD03 MitubishiJose Maria GedaNo ratings yet

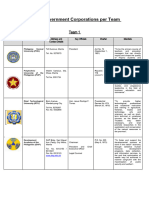

- List of GOCCsDocument3 pagesList of GOCCsvinz99No ratings yet

- Cases CivrevDocument473 pagesCases CivrevLady Lyn DinerosNo ratings yet

- Philippine National Oil CompanyDocument19 pagesPhilippine National Oil CompanyRonald Coracero RosadaNo ratings yet

- Case Digest - Week 5Document106 pagesCase Digest - Week 5Van John MagallanesNo ratings yet

- Case Study CSRDocument7 pagesCase Study CSRSherryNo ratings yet

- City of Batangas Vs Pilipinas ShellDocument10 pagesCity of Batangas Vs Pilipinas ShelllyrrehcNo ratings yet

- City of Batangas v. Philippine Shell Petroleum Corporation, 826 SCRA 297 (2017)Document17 pagesCity of Batangas v. Philippine Shell Petroleum Corporation, 826 SCRA 297 (2017)GWYNETH SANTOSNo ratings yet

- Formative Assessment 2 - EnumerationDocument18 pagesFormative Assessment 2 - EnumerationArgieshi GCNo ratings yet

- City of Batangas v. Philippine ShellDocument15 pagesCity of Batangas v. Philippine ShellKristelle TNo ratings yet

- Garcia vs. J.G. Summit Petrochemical Corporation, 516 SCRA 493, February 23, 2007Document3 pagesGarcia vs. J.G. Summit Petrochemical Corporation, 516 SCRA 493, February 23, 2007idolbondocNo ratings yet

- 2017-06-07 City of Batangas vs. Philippine Shell Petroleum Corp. (2017)Document15 pages2017-06-07 City of Batangas vs. Philippine Shell Petroleum Corp. (2017)a_vlaureNo ratings yet

- City of Batangas v. Philippine Shell Petroleum Corporation, 826 SCRA 297 (2017)Document12 pagesCity of Batangas v. Philippine Shell Petroleum Corporation, 826 SCRA 297 (2017)Henri Ana Sofia NicdaoNo ratings yet

- City of Batangas v. Shell G.R. No. 195003Document8 pagesCity of Batangas v. Shell G.R. No. 195003Lorille LeonesNo ratings yet

- Gocc List 2023Document24 pagesGocc List 2023api-665271692No ratings yet