You might also like

- Accounting Information System ReviewerDocument16 pagesAccounting Information System RevieweralabwalaNo ratings yet

- Benchmarking for Businesses: Measure and improve your company's performanceFrom EverandBenchmarking for Businesses: Measure and improve your company's performanceNo ratings yet

- VALLEJOS-ACCTG 301-Retail Inventoy Method-Hand OutDocument5 pagesVALLEJOS-ACCTG 301-Retail Inventoy Method-Hand OutEllah RahNo ratings yet

- MAS - 1416 Profit Planning - CVP AnalysisDocument24 pagesMAS - 1416 Profit Planning - CVP AnalysisAzureBlazeNo ratings yet

- FinMan Managerial 11e IM Ch24 (9) FinalDocument14 pagesFinMan Managerial 11e IM Ch24 (9) Finalppantin0430No ratings yet

- MGT 1 Cost Volume Profit RelationshipsDocument3 pagesMGT 1 Cost Volume Profit RelationshipsExequiel AdradaNo ratings yet

- Master in Managerial Advisory Services: Easy QuestionsDocument13 pagesMaster in Managerial Advisory Services: Easy QuestionsKervin Rey JacksonNo ratings yet

- Answers To 11 - 16 Assignment in ABC PDFDocument3 pagesAnswers To 11 - 16 Assignment in ABC PDFMubarrach MatabalaoNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument6 pagesManila Cavite Laguna Cebu Cagayan de Oro Davaovane rondinaNo ratings yet

- Ch4 Process CostingDocument270 pagesCh4 Process Costingmattymo22No ratings yet

- Managerial Economics QuestionnairesDocument26 pagesManagerial Economics QuestionnairesClyde SaladagaNo ratings yet

- MASDocument5 pagesMASMusic LastNo ratings yet

- Accounting For LaborDocument1 pageAccounting For LaborkwekwkNo ratings yet

- Contributed CapitalDocument3 pagesContributed CapitalCharize YebanNo ratings yet

- Total Cash Receipt From Issuance of BondsDocument11 pagesTotal Cash Receipt From Issuance of Bondskrisha milloNo ratings yet

- 1) Answer: Interest Expense 0 Solution:: Financial Statement AnalysisDocument3 pages1) Answer: Interest Expense 0 Solution:: Financial Statement AnalysisGA ZinNo ratings yet

- Acc 123 Week 45 1Document47 pagesAcc 123 Week 45 1slow dancerNo ratings yet

- Short-Term Financing - Extra CreditDocument7 pagesShort-Term Financing - Extra CreditEnola HolmesNo ratings yet

- 4a Standard Costs and Analysis of VariancesDocument3 pages4a Standard Costs and Analysis of VariancesGina TingdayNo ratings yet

- Handout 1.0 ACC 123 Practice Problems For Cost Concepts and Cost BehaviorDocument2 pagesHandout 1.0 ACC 123 Practice Problems For Cost Concepts and Cost BehaviorFrancine Thea M. LantayaNo ratings yet

- Construction ContractDocument17 pagesConstruction ContractYvonne Gam-oyNo ratings yet

- Gbermic 11-12Document13 pagesGbermic 11-12Paolo Niel ArenasNo ratings yet

- Chapter 9Document17 pagesChapter 9Flordeliza VidadNo ratings yet

- Process Costing: Assign Cost To Outputs in ManufacturingDocument7 pagesProcess Costing: Assign Cost To Outputs in ManufacturingJoanne TolentinoNo ratings yet

- ACCCOB3 CVP Analysis Case Problems Instructions:: Ryan - Roque@dlsu - Edu.phDocument2 pagesACCCOB3 CVP Analysis Case Problems Instructions:: Ryan - Roque@dlsu - Edu.phdanii yaahNo ratings yet

- Last QuizDocument5 pagesLast QuizMariah MacasNo ratings yet

- Quiz 2 Cost AccountingDocument1 pageQuiz 2 Cost AccountingRocel DomingoNo ratings yet

- Set A Leases Problem SERANADocument6 pagesSet A Leases Problem SERANASherri BonquinNo ratings yet

- Allocation of Joint Costs and Accounting For By-Product/ScrapDocument14 pagesAllocation of Joint Costs and Accounting For By-Product/ScrapMr. FoxNo ratings yet

- Financial RatiosDocument27 pagesFinancial RatiosVenz LacreNo ratings yet

- Service and Production Department Cost AllocationDocument58 pagesService and Production Department Cost AllocationLorena TudorascuNo ratings yet

- ParCor Corpo EQ Set ADocument3 pagesParCor Corpo EQ Set AMara LacsamanaNo ratings yet

- Lesson 4 Expenditure Cycle PDFDocument19 pagesLesson 4 Expenditure Cycle PDFJoshua JunsayNo ratings yet

- Requirements:: Intermediate Accounting 3Document7 pagesRequirements:: Intermediate Accounting 3happy240823No ratings yet

- Financial Management For Decision Making: Marian G. Magcalas Ishmael Y. ReyesDocument38 pagesFinancial Management For Decision Making: Marian G. Magcalas Ishmael Y. ReyesJordan Mathew Alcaide MalapayaNo ratings yet

- Lupisan-Baysa PDFDocument206 pagesLupisan-Baysa PDFRicart Von LauretaNo ratings yet

- BBDocument3 pagesBBJoshua WacanganNo ratings yet

- AIS Chap 8 NotesDocument7 pagesAIS Chap 8 NotesKrisshaNo ratings yet

- JakeDocument5 pagesJakeEvan JordanNo ratings yet

- DocxDocument40 pagesDocxJamaica DavidNo ratings yet

- Solution To Assignment 1Document3 pagesSolution To Assignment 1Khyla DivinagraciaNo ratings yet

- Mas QuestionsDocument2 pagesMas QuestionsEll VNo ratings yet

- Receipt and Disposition of InventoriesDocument5 pagesReceipt and Disposition of InventoriesWawex DavisNo ratings yet

- Chap 001Document56 pagesChap 001Louie De La TorreNo ratings yet

- Responsibility Accounting: Acctg 205: Management ScienceDocument34 pagesResponsibility Accounting: Acctg 205: Management ScienceEliseNo ratings yet

- Consolidating Balance SheetsDocument4 pagesConsolidating Balance Sheetsangel2199No ratings yet

- Break-Even Analysis: Cost-Volume-Profit AnalysisDocument64 pagesBreak-Even Analysis: Cost-Volume-Profit AnalysisKelvin LeongNo ratings yet

- Cost 2 - Quiz5 PDFDocument7 pagesCost 2 - Quiz5 PDFshengNo ratings yet

- Abc Costing IllustratedDocument2 pagesAbc Costing IllustratedBryan FloresNo ratings yet

- 2nd Week - The Master Budget ExercisesDocument5 pages2nd Week - The Master Budget ExercisesLuigi Enderez BalucanNo ratings yet

- Non-Routine DecisionsDocument5 pagesNon-Routine DecisionsVincent Lazaro0% (1)

- Cost Concept, Terminologies and BehaviorDocument8 pagesCost Concept, Terminologies and BehaviorANDREA NICOLE DE LEONNo ratings yet

- Transfer PricingDocument19 pagesTransfer PricingDhara BadianiNo ratings yet

- Residual Income (RI) Is The Difference Between Operating Income and The MinimumDocument8 pagesResidual Income (RI) Is The Difference Between Operating Income and The MinimumIndah SetyoriniNo ratings yet

- C.2. Transfer Pricing EssayDocument7 pagesC.2. Transfer Pricing EssayKondreddi SakuNo ratings yet

- Management Control SystemDocument25 pagesManagement Control SystemRitesh ShirsatNo ratings yet

- Basic Types of Responsibility CentersDocument5 pagesBasic Types of Responsibility CentersmeseleNo ratings yet

- Chapter 7cost IIDocument6 pagesChapter 7cost IITammy 27No ratings yet

- Transfer PricingDocument47 pagesTransfer PricingRhoselle Mae Genanda100% (1)

- CBMEC - Skilled Care PharmacyDocument3 pagesCBMEC - Skilled Care PharmacyNors Pataytay67% (3)

- Chapter 3 - Growth and The Asian ExperienceDocument55 pagesChapter 3 - Growth and The Asian ExperienceNors PataytayNo ratings yet

- Company BackgroundDocument2 pagesCompany BackgroundNors PataytayNo ratings yet

- Disposition of VariancesDocument12 pagesDisposition of VariancesNors PataytayNo ratings yet

- Ac2102 RaDocument9 pagesAc2102 RaNors PataytayNo ratings yet

- AC 2203 Economic Development SyllabusDocument2 pagesAC 2203 Economic Development SyllabusNors PataytayNo ratings yet

- History Og The Accommodation SectorDocument34 pagesHistory Og The Accommodation SectorNors PataytayNo ratings yet

- El FiliDocument125 pagesEl FiliNors Pataytay0% (1)

- 19 - Revaluation and ImpairmentDocument3 pages19 - Revaluation and Impairmentjaymark canayaNo ratings yet

- The Relationship of Science, Religion and Ethics: Ethical Significance From Laudato SiDocument3 pagesThe Relationship of Science, Religion and Ethics: Ethical Significance From Laudato SiNors PataytayNo ratings yet

- The Following Data For Karen Company Are Available For Your AnalysisDocument7 pagesThe Following Data For Karen Company Are Available For Your AnalysisNors PataytayNo ratings yet

- Bank Reconciliation EditedDocument1 pageBank Reconciliation EditedNors PataytayNo ratings yet

- Cebu Unemployment TrendDocument5 pagesCebu Unemployment TrendNors PataytayNo ratings yet

- DAY6 Freely English Translation LyricsDocument3 pagesDAY6 Freely English Translation LyricsNors PataytayNo ratings yet

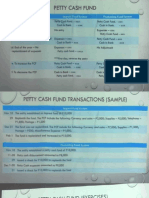

- Petty Cash Fund NotesDocument6 pagesPetty Cash Fund NotesNors Pataytay0% (1)

- The Standard Normal DistributionDocument23 pagesThe Standard Normal DistributionNors PataytayNo ratings yet

- Personal Financial ManagementDocument39 pagesPersonal Financial ManagementNors PataytayNo ratings yet

- Installment BuyingDocument33 pagesInstallment BuyingNors PataytayNo ratings yet

- Job Order CostingDocument25 pagesJob Order CostingNors PataytayNo ratings yet

- Chapter 1, Project Logistics PPDocument78 pagesChapter 1, Project Logistics PPwakzeleke2020No ratings yet

- Contemporary Issues in Accounting: Powerpoint Presentation by Matthew Tilling ©2012 John Wiley & Sons Australia LTDDocument41 pagesContemporary Issues in Accounting: Powerpoint Presentation by Matthew Tilling ©2012 John Wiley & Sons Australia LTDdhfbbbbbbbbbbbbbbbbbhNo ratings yet

- Asian Transmission Corporation vs. CIR (Full Text, Word Version)Document8 pagesAsian Transmission Corporation vs. CIR (Full Text, Word Version)Emir MendozaNo ratings yet

- DEMS SPZ Audit ReportDocument9 pagesDEMS SPZ Audit ReportSubhas MishraNo ratings yet

- 1mdb FinalDocument8 pages1mdb FinalMuadz Kamaruddin100% (1)

- Ca Rohit Chola: ProfileDocument2 pagesCa Rohit Chola: ProfileThe Cultural CommitteeNo ratings yet

- 07-Determining MaterialityDocument20 pages07-Determining Materialityfareha riazNo ratings yet

- Week 3 Discussion ProblemsDocument23 pagesWeek 3 Discussion ProblemsKiran JojiNo ratings yet

- Orgchart Web September 2023Document1 pageOrgchart Web September 2023rizal suheriNo ratings yet

- Module 3 Quiz With AnswersssDocument3 pagesModule 3 Quiz With AnswersssShahd Okasha100% (1)

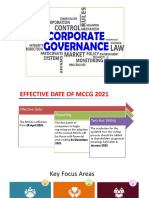

- Corporate Governance 2021Document63 pagesCorporate Governance 2021UKLead ServicesNo ratings yet

- The Matching Concept and The Adjusting ProcessDocument51 pagesThe Matching Concept and The Adjusting ProcesswarsimaNo ratings yet

- SS 2304 2019Document4 pagesSS 2304 2019lavnishNo ratings yet

- Audit of Banking IndustryDocument34 pagesAudit of Banking IndustryChristine Mae FelixNo ratings yet

- Chapter 9-AuditDocument45 pagesChapter 9-AuditMisshtaCNo ratings yet

- Solution 103-Basic Accounting Problem 103 - Recording - Business - TransactionsDocument15 pagesSolution 103-Basic Accounting Problem 103 - Recording - Business - TransactionsmeepxxxNo ratings yet

- CBDT Circular 19 2019 Income Tax DT 14 August 2019 Quote Din in It Notices CommunicationsDocument2 pagesCBDT Circular 19 2019 Income Tax DT 14 August 2019 Quote Din in It Notices CommunicationsLalit Mohan JindalNo ratings yet

- P7AAAInt Study Question Bank Sample D14 J15Document96 pagesP7AAAInt Study Question Bank Sample D14 J15Jing Yi Hui100% (1)

- ACCA F3 Introduction To The PaperDocument3 pagesACCA F3 Introduction To The PaperHopeson AgbenorxeviNo ratings yet

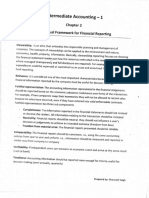

- Intermediate Accounting: Conceptual Framework For Financial ReportingDocument4 pagesIntermediate Accounting: Conceptual Framework For Financial ReportingKerby Gail RulonaNo ratings yet

- Idbi Stock Audit Format PDFDocument6 pagesIdbi Stock Audit Format PDFgokul ramananNo ratings yet

- 13 EdlDocument7 pages13 EdlEL GHARBAOUINo ratings yet

- Solution Manual For Accounting 9th Edition by HoggettDocument39 pagesSolution Manual For Accounting 9th Edition by Hoggetta23900595467% (3)

- InternalDocument8 pagesInternalJessnah GraceNo ratings yet

- Chapter 8 - Cash, Fraud, and Internal Control Internal Control SystemDocument5 pagesChapter 8 - Cash, Fraud, and Internal Control Internal Control SystemAngel Frankie RamosNo ratings yet

- Silang v. COA Persons Liable Solidary LiabilityDocument16 pagesSilang v. COA Persons Liable Solidary Liabilitymelchor1925No ratings yet

- Audit IndependenceDocument9 pagesAudit Independencerohitgupta_arsenalNo ratings yet

- Sample USA ResumeDocument2 pagesSample USA ResumeJutt JuttNo ratings yet

- Report On Corporate GovernanceDocument22 pagesReport On Corporate GovernanceMahek KhanNo ratings yet

- Messier 11e Chap13 PPT TBDocument31 pagesMessier 11e Chap13 PPT TBSamuel TwentyoneNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Your First CFO: The Accounting Cure for Small Business OwnersFrom EverandYour First CFO: The Accounting Cure for Small Business OwnersRating: 4 out of 5 stars4/5 (2)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!From EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Rating: 4.5 out of 5 stars4.5/5 (8)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingFrom EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingRating: 4.5 out of 5 stars4.5/5 (760)

- Radically Simple Accounting: A Way Out of the Dark and Into the ProfitFrom EverandRadically Simple Accounting: A Way Out of the Dark and Into the ProfitRating: 4.5 out of 5 stars4.5/5 (9)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackFrom EverandThe Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackRating: 1 out of 5 stars1/5 (1)

- Excel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsFrom EverandExcel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Project Control Methods and Best Practices: Achieving Project SuccessFrom EverandProject Control Methods and Best Practices: Achieving Project SuccessNo ratings yet

- Accounting All-in-One For Dummies, with Online PracticeFrom EverandAccounting All-in-One For Dummies, with Online PracticeRating: 3 out of 5 stars3/5 (1)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)