You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 1993 Toyota Vacuum DiagramsDocument22 pages1993 Toyota Vacuum Diagramsr4depositario100% (10)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- E51 Quick Reference GuideDocument52 pagesE51 Quick Reference Guidedsladden100% (1)

- Mercedes Tourismo Euro 6 Manual PDFDocument519 pagesMercedes Tourismo Euro 6 Manual PDFAshley Cardwell50% (2)

- Esurance Tow and Labor Program OverviewDocument29 pagesEsurance Tow and Labor Program OverviewCAROLL VANESSA VERGARA CELISNo ratings yet

- The Global Pharmaceutical IndustryDocument15 pagesThe Global Pharmaceutical IndustryKia LadnomNo ratings yet

- MGN 166 Passage Plan GuidanceDocument4 pagesMGN 166 Passage Plan GuidancePushkar Lamba100% (1)

- TCS Khamgaon-Tcs 1 PDFDocument1 pageTCS Khamgaon-Tcs 1 PDFFaraz hasan KhanNo ratings yet

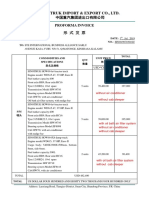

- Pro Forma Invoice For HOWO Tractor Truck and Dump Truck (CIF) CorrigéDocument2 pagesPro Forma Invoice For HOWO Tractor Truck and Dump Truck (CIF) CorrigéFAOUZI100% (1)

- Agriculture MarketingDocument16 pagesAgriculture MarketingLearner84100% (1)

- E132 Emanuel Ghioca Moraru Business Understanding and Leading ChangeDocument21 pagesE132 Emanuel Ghioca Moraru Business Understanding and Leading ChangeKia Ladnom100% (2)

- Janos Business StrategyDocument11 pagesJanos Business StrategyKia LadnomNo ratings yet

- E133 Cezar Ionescu Business Management AccountingDocument20 pagesE133 Cezar Ionescu Business Management AccountingKia LadnomNo ratings yet

- E133 Mihai Diaconu Business Human Resources ManagementDocument20 pagesE133 Mihai Diaconu Business Human Resources ManagementKia LadnomNo ratings yet

- Bogdan Soi Unit 20 Visitor Atraction ManagementDocument20 pagesBogdan Soi Unit 20 Visitor Atraction ManagementKia LadnomNo ratings yet

- Order Id 180210698013276Document8 pagesOrder Id 180210698013276Kia LadnomNo ratings yet

- System DevelopmentDocument14 pagesSystem DevelopmentKia LadnomNo ratings yet

- Kan 231018dis FinalDocument50 pagesKan 231018dis FinalKia LadnomNo ratings yet

- Macro & Micro EconomicsDocument10 pagesMacro & Micro EconomicsKia LadnomNo ratings yet

- KAN 231018DIS ProposalDocument4 pagesKAN 231018DIS ProposalKia LadnomNo ratings yet

- Augmented Services and Competitive Advantages of Singapore AirlinesDocument6 pagesAugmented Services and Competitive Advantages of Singapore AirlinesKia LadnomNo ratings yet

- 128926Document15 pages128926Kia LadnomNo ratings yet

- International FinanceDocument8 pagesInternational FinanceKia LadnomNo ratings yet

- VB 2038501 - 0.5Document5 pagesVB 2038501 - 0.5Kia LadnomNo ratings yet

- WS 60815 - 1.0Document7 pagesWS 60815 - 1.0Kia LadnomNo ratings yet

- Final Assessment For International Marketing and Business EnvironmentDocument1 pageFinal Assessment For International Marketing and Business EnvironmentKia LadnomNo ratings yet

- Ut1 - Edgu1003Document15 pagesUt1 - Edgu1003Kia LadnomNo ratings yet

- Packages That Are Difficult To OpenDocument33 pagesPackages That Are Difficult To OpenKia LadnomNo ratings yet

- Soal InggrisDocument3 pagesSoal InggrisCut MutiaNo ratings yet

- Vehicle Inspection FormDocument2 pagesVehicle Inspection Formarbab shafiqNo ratings yet

- BYD F3DM Owner's ManualDocument214 pagesBYD F3DM Owner's ManualAlfredo jose Medina revattaNo ratings yet

- Pallet Rack PDFDocument5 pagesPallet Rack PDFAngela SimoesNo ratings yet

- SafariDocument1 pageSafarijayNo ratings yet

- Advancement in Technology in Water TransportDocument8 pagesAdvancement in Technology in Water TransportAnkur BansalNo ratings yet

- Low-Pressure Tube SystemsDocument33 pagesLow-Pressure Tube SystemspranavNo ratings yet

- Fare Information: Route 33 & 33aDocument3 pagesFare Information: Route 33 & 33aLih PereiraNo ratings yet

- Grammar 1 Complete The Dialogues. Use The Verbs in Brackets in The Present Perfect Simple or The Past SimpleDocument4 pagesGrammar 1 Complete The Dialogues. Use The Verbs in Brackets in The Present Perfect Simple or The Past SimpleGiancarlo Edu HugoNo ratings yet

- Corporate Properties Study Benton Harbor/St. Joseph Part IIDocument112 pagesCorporate Properties Study Benton Harbor/St. Joseph Part IIProtectJKPNo ratings yet

- Cio NCRDocument16 pagesCio NCRVirender RawatNo ratings yet

- Steering SystemDocument12 pagesSteering Systemmayur_lanjewarNo ratings yet

- Mobile Cranes Approval Checklist FinalDocument1 pageMobile Cranes Approval Checklist Finalzelda1022No ratings yet

- MIL ON DTC P1364P1365 Camshaft Position Actuator Lexus Ls 460 2010Document5 pagesMIL ON DTC P1364P1365 Camshaft Position Actuator Lexus Ls 460 2010Sajjad HussainNo ratings yet

- 20 Mirage (Eng)Document230 pages20 Mirage (Eng)Ajendam 1 SimindiasahpraNo ratings yet

- GATIDocument25 pagesGATIAryan SarohaNo ratings yet

- 7.3L PCM Codes FamiliesDocument11 pages7.3L PCM Codes FamiliesHector JacoboNo ratings yet

- Hasnol (B.i)Document5 pagesHasnol (B.i)Mohd Nazri AwangNo ratings yet

- Neom The Line Fact Sheet EngDocument5 pagesNeom The Line Fact Sheet EngNinaNo ratings yet

- INFRASTRUCTUREDocument3 pagesINFRASTRUCTUREkerwin jayNo ratings yet

- Bell 505 VFR Helisas Autopilot & AugmentationDocument2 pagesBell 505 VFR Helisas Autopilot & AugmentationNickNo ratings yet

- 143 147 PDFDocument5 pages143 147 PDFDanielNo ratings yet