You might also like

- Typical Account Titles UsedDocument3 pagesTypical Account Titles Usedwenna janeNo ratings yet

- Vanity Mirror with Drawers for StudentsDocument13 pagesVanity Mirror with Drawers for StudentsMa. Katrina ComediaNo ratings yet

- Ethical Issues in Business Case StudyDocument11 pagesEthical Issues in Business Case Studyclarisse villegas100% (2)

- Basic Acctg 4th SatDocument11 pagesBasic Acctg 4th SatJerome Eziekel Posada PanaliganNo ratings yet

- Module 1 Introduction To AccountingDocument8 pagesModule 1 Introduction To AccountingShårmāinë Iniégø DimâänōNo ratings yet

- Liabilities Amount CalculationDocument6 pagesLiabilities Amount CalculationRoel Cababao50% (2)

- 03 Quiz 1 AubDocument3 pages03 Quiz 1 Aubken dahunanNo ratings yet

- Walmart Mexico's Renewable Energy InvestmentsDocument4 pagesWalmart Mexico's Renewable Energy InvestmentsLizcel CastillaNo ratings yet

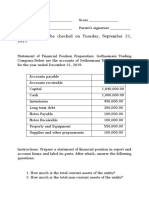

- Answer This To Be Checked On Tuesday, September 21, 2021Document2 pagesAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNo ratings yet

- Chapter 1Document19 pagesChapter 1Krissa Mae LongosNo ratings yet

- Chapter 3 - Effect of Omitting Adjusting Journal Entries: Examples: Type Effect of Not Making The Adjustment DEDocument3 pagesChapter 3 - Effect of Omitting Adjusting Journal Entries: Examples: Type Effect of Not Making The Adjustment DEGelle PascualNo ratings yet

- ACC 205 Complete Class HomeworkDocument41 pagesACC 205 Complete Class HomeworkAvicciNo ratings yet

- Accounting Concepts and PrinciplesDocument4 pagesAccounting Concepts and Principlesdane alvarezNo ratings yet

- Financial Statements AnalysisDocument35 pagesFinancial Statements AnalysisKiarra Nicel De TorresNo ratings yet

- ActivityDocument4 pagesActivityRain Vicente100% (1)

- Well" - A New Way of Saying - "Do Well by Doing Good."Document3 pagesWell" - A New Way of Saying - "Do Well by Doing Good."Rinna Lynn FraniNo ratings yet

- Puregold CompanyDocument7 pagesPuregold CompanyChristineAmielGuirreNo ratings yet

- The Accounting CycleDocument3 pagesThe Accounting Cycleliesly buticNo ratings yet

- Acctg 1Document3 pagesAcctg 1HoneyzelOmandamPonceNo ratings yet

- Bank Reconciliation AssessmentDocument14 pagesBank Reconciliation AssessmentDaisy Ann Cariaga SaccuanNo ratings yet

- Chap 6 Notes AFMDocument30 pagesChap 6 Notes AFMAngel RubiosNo ratings yet

- Mira's School Supplies Store Financial AnalysisDocument1 pageMira's School Supplies Store Financial AnalysisMiguel Lulab100% (1)

- SAP B1 Fundamentals AccountingDocument33 pagesSAP B1 Fundamentals AccountingJosef SamoranosNo ratings yet

- The Circular Flow of Economic Activity (Autosaved)Document19 pagesThe Circular Flow of Economic Activity (Autosaved)LittleagleNo ratings yet

- Castro-Merchandising 20211124 0001Document2 pagesCastro-Merchandising 20211124 0001Chelsea TengcoNo ratings yet

- Business Math Quarter 3 Week 2Document8 pagesBusiness Math Quarter 3 Week 2Gladys Angela ValdemoroNo ratings yet

- Accounting Perpetual & Periodic ComparisonDocument1 pageAccounting Perpetual & Periodic ComparisonAbbey LiNo ratings yet

- General Ledger - Adrianne, Mendoza-BSBA-1 BLK BDocument6 pagesGeneral Ledger - Adrianne, Mendoza-BSBA-1 BLK BJaks ExplorerNo ratings yet

- How the Five Forces Model Reveals Agriculture as a Better Investment than a Sari-Sari StoreDocument6 pagesHow the Five Forces Model Reveals Agriculture as a Better Investment than a Sari-Sari StoreJoshua Eric Velasco DandalNo ratings yet

- Chapter 3Document21 pagesChapter 3Dafhny Guinto PasionNo ratings yet

- ACEFIAR Quiz No. 1Document3 pagesACEFIAR Quiz No. 1Marriel Fate CullanoNo ratings yet

- Record Business Transactions for Shin Consulting ServiceDocument12 pagesRecord Business Transactions for Shin Consulting ServiceAsh imoNo ratings yet

- Math 1100 - Chapter 9-12Document42 pagesMath 1100 - Chapter 9-12tangwanlu91770% (1)

- Managerial Costs KeyDocument7 pagesManagerial Costs KeyJane VillanuevaNo ratings yet

- 10 Segismundo, Ma. Isabella 12 Gilead Apolaki Week 5 Textbook ExercisesDocument2 pages10 Segismundo, Ma. Isabella 12 Gilead Apolaki Week 5 Textbook ExercisesMaria IsabellaNo ratings yet

- Research: Defining Key Terms and ObjectivesDocument5 pagesResearch: Defining Key Terms and Objectivesvarun v sNo ratings yet

- Quiz. For Ten (10) Points Each, Answer The Following Questions BrieflyDocument2 pagesQuiz. For Ten (10) Points Each, Answer The Following Questions BrieflyJohn Phil PecadizoNo ratings yet

- 2 CHAPTER Lesson 2 1 AssetsDocument6 pages2 CHAPTER Lesson 2 1 AssetsRegine BaterisnaNo ratings yet

- CH 03Document7 pagesCH 03Bind Prozt100% (1)

- Conceptual Framework Guides Financial Reporting StandardsDocument3 pagesConceptual Framework Guides Financial Reporting StandardsJynilou PinoteNo ratings yet

- Quiz 2 Cost AccountingDocument1 pageQuiz 2 Cost AccountingRocel DomingoNo ratings yet

- Account Titles and Its ElementsDocument3 pagesAccount Titles and Its ElementsJeb PampliegaNo ratings yet

- FABM 2 Guide Mid Term ALL LearnersDocument8 pagesFABM 2 Guide Mid Term ALL LearnersYnahNo ratings yet

- AccountingDocument5 pagesAccountingAbe Loran PelandianaNo ratings yet

- Analysis and Interpretation of FS 1Document13 pagesAnalysis and Interpretation of FS 1marissa casareno almueteNo ratings yet

- Journal Entry - Sample ActivityDocument16 pagesJournal Entry - Sample ActivityCyd BenitoNo ratings yet

- Handouts Acctg 1 - MerchandisingDocument13 pagesHandouts Acctg 1 - MerchandisingJoannah Marie OliverosNo ratings yet

- Financial Statement Analysis Part 2Document10 pagesFinancial Statement Analysis Part 2Kim Patrick VictoriaNo ratings yet

- Fabm2 Q1 M4Document23 pagesFabm2 Q1 M4Beverly ComamoNo ratings yet

- Quiz Adjusting Entries Multiple Choice WithoutDocument5 pagesQuiz Adjusting Entries Multiple Choice WithoutRakzMagaleNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument31 pagesAccounting Cycle of A Merchandising BusinessAresta, Novie Mae100% (1)

- Fundamental of Accounting, Business, and Management 2 PDFDocument15 pagesFundamental of Accounting, Business, and Management 2 PDFElijah AramburoNo ratings yet

- Seven Unidentified Philippine IndustriesDocument4 pagesSeven Unidentified Philippine Industriessi_roselynNo ratings yet

- CBMEC - Operations Management - PreMidDocument4 pagesCBMEC - Operations Management - PreMidjojie dadorNo ratings yet

- LIQUIDITY RATIOS EXPLAINEDDocument21 pagesLIQUIDITY RATIOS EXPLAINEDWynphap podiotanNo ratings yet

- Acceptability and Marketability of Laing SiopaoDocument6 pagesAcceptability and Marketability of Laing SiopaogjaymarNo ratings yet

- The Chart of Accounts: AssetsDocument8 pagesThe Chart of Accounts: AssetsSrinivasarao BendalamNo ratings yet

- Key financial reporting explainedDocument11 pagesKey financial reporting explainedhemanth727100% (1)

- Valuation: A Conceptual Overview: StreetofwallsDocument64 pagesValuation: A Conceptual Overview: StreetofwallsJeniferNo ratings yet

- FinMan Module 3 FS, Cash Flow and TaxesDocument10 pagesFinMan Module 3 FS, Cash Flow and Taxeserickson hernanNo ratings yet

- Capital Structure Ultratech Cement Sahithi Project 111111Document85 pagesCapital Structure Ultratech Cement Sahithi Project 111111Sahithi PNo ratings yet

- Fap CombinedDocument77 pagesFap CombinedKevin MehtaNo ratings yet

- Financial Accounting - Wiley (ch01)Document79 pagesFinancial Accounting - Wiley (ch01)Aji Sasio100% (4)

- Aop 2013 PDFDocument270 pagesAop 2013 PDFsanti105134025No ratings yet

- Mindanao State University - Marawi City College of Business Administration and Accountancy Accountancy Department 2 Semester, AY 2015-2016Document9 pagesMindanao State University - Marawi City College of Business Administration and Accountancy Accountancy Department 2 Semester, AY 2015-2016Sittie Ainna A. UnteNo ratings yet

- The Income Statement and Statement of Changes in EquityDocument40 pagesThe Income Statement and Statement of Changes in EquityXarreigh Dien VilladaresNo ratings yet

- Understanding Corporate FinanceDocument98 pagesUnderstanding Corporate FinanceJosh KrishaNo ratings yet

- Financial Management:: Financial Analysis - Sizing Up Firm PerformanceDocument104 pagesFinancial Management:: Financial Analysis - Sizing Up Firm PerformanceArgem Jay PorioNo ratings yet

- Tata Asset ManagementDocument18 pagesTata Asset ManagementManjunath ManuNo ratings yet

- Understanding dividend policies and their impact on corporations and shareholdersDocument32 pagesUnderstanding dividend policies and their impact on corporations and shareholdersJoselle Jan Claudio100% (1)

- BFSDocument208 pagesBFSk.purushothNo ratings yet

- Audit stockholders' equity problemsDocument7 pagesAudit stockholders' equity problemsLizette Oliva80% (5)

- Financial Reporting Conceptual Framework of Financial Accounting KeyDocument13 pagesFinancial Reporting Conceptual Framework of Financial Accounting KeySteffNo ratings yet

- Chapter 18 Shareholders Equity - Docx-1Document14 pagesChapter 18 Shareholders Equity - Docx-1kanroji1923No ratings yet

- PT Cemerlang - MYOB PDFDocument7 pagesPT Cemerlang - MYOB PDFAie MargiyantiNo ratings yet

- Fin 301 Final Assignment Group Name G 1Document26 pagesFin 301 Final Assignment Group Name G 1Avishake SahaNo ratings yet

- Financial System QuestionsDocument25 pagesFinancial System QuestionsJ. KNo ratings yet

- Developments in Business Simulation & Experiential Exercises, Volume 22, 1995Document7 pagesDevelopments in Business Simulation & Experiential Exercises, Volume 22, 1995Any thinkNo ratings yet

- ACC201 Financial AccountingDocument47 pagesACC201 Financial AccountingG JhaNo ratings yet

- Corporate Restructuring Strategies ExplainedDocument26 pagesCorporate Restructuring Strategies ExplainedAmar Singh SaudNo ratings yet

- Cash Flow StatementDocument22 pagesCash Flow StatementThe ONE GUYNo ratings yet

- Financial Statement PreparationDocument9 pagesFinancial Statement PreparationDELFIN, LORENA D.No ratings yet

- AOM NO. 01-Stale ChecksDocument3 pagesAOM NO. 01-Stale ChecksRagnar Lothbrok100% (2)

- Accounting and Business Reporting - PDFDocument30 pagesAccounting and Business Reporting - PDFAbhijeet SavantNo ratings yet

- Principles of Accounting Chapter 14Document43 pagesPrinciples of Accounting Chapter 14myrentistoodamnhighNo ratings yet

- Sample Subscription AgreementDocument19 pagesSample Subscription AgreementLonny Bernath100% (2)

- AUDIT MCQs-Arens, Elder, Beasley - FinalDocument13 pagesAUDIT MCQs-Arens, Elder, Beasley - FinalLeigh PilapilNo ratings yet

- Shark Loan Should Accept Wendy's 200B FinancialsDocument2 pagesShark Loan Should Accept Wendy's 200B FinancialsEva Mae Fernandez OcularNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Business Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsFrom EverandBusiness Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsNo ratings yet

- Emprender un Negocio: Paso a Paso Para PrincipiantesFrom EverandEmprender un Negocio: Paso a Paso Para PrincipiantesRating: 3 out of 5 stars3/5 (1)

- Basic Accounting: Service Business Study GuideFrom EverandBasic Accounting: Service Business Study GuideRating: 5 out of 5 stars5/5 (2)

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)

- Mysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungFrom EverandMysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungRating: 4 out of 5 stars4/5 (1)