You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Bank Letter For Fixed Deposit - SampleDocument1 pageBank Letter For Fixed Deposit - Sampletvaprasad67% (6)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- General AnnuitiesDocument141 pagesGeneral AnnuitiesJuanito71% (7)

- CH 10 - Making Capital Investment DecisionsDocument26 pagesCH 10 - Making Capital Investment Decisionsxiobnb0% (1)

- CONTRACT AssignmentDocument14 pagesCONTRACT AssignmentInjila ZaidiNo ratings yet

- Removal of Directors or Trustees: by The SEC - After Notice and Hearing and Only OnDocument2 pagesRemoval of Directors or Trustees: by The SEC - After Notice and Hearing and Only OnApple Ke-eNo ratings yet

- Economic Growth EssayDocument8 pagesEconomic Growth Essaycjawrknbf100% (2)

- Knowledge Sharing in Workplace: Motivators and DemotivatorsDocument14 pagesKnowledge Sharing in Workplace: Motivators and DemotivatorsijmitNo ratings yet

- Plant Design and Economics For Chemical Engineers Chapter 7Document57 pagesPlant Design and Economics For Chemical Engineers Chapter 7Wajahat SiddiqueNo ratings yet

- Income Tax AssignmentDocument7 pagesIncome Tax AssignmentDisha MohantyNo ratings yet

- A.L Tte: Lndustriat Lnfrastructur.. B.SC, ManaserDocument2 pagesA.L Tte: Lndustriat Lnfrastructur.. B.SC, ManaserRama Rao MajjiNo ratings yet

- Acctg 14 Absorption Variable CostingDocument2 pagesAcctg 14 Absorption Variable CostingSamantha ReromaNo ratings yet

- Study Guide 1Document5 pagesStudy Guide 1Wise MoonNo ratings yet

- Inter-Regional and Maritime TradeDocument24 pagesInter-Regional and Maritime TradeNIRAKAR PATRA100% (2)

- Consumer Protection in Choice of LawDocument34 pagesConsumer Protection in Choice of LawMeredith DaughertyNo ratings yet

- 08-Rozman-Can Confucianism Survive in Universalism and GlobalizationDocument28 pages08-Rozman-Can Confucianism Survive in Universalism and GlobalizationYong Jae KwonNo ratings yet

- Lesson Plan TabularDocument7 pagesLesson Plan TabularDanmar CamilotNo ratings yet

- Thrift Banks ActDocument25 pagesThrift Banks ActMadelle Pineda100% (1)

- Research Proposal For Research MethodologyDocument11 pagesResearch Proposal For Research MethodologyAnonymous sCQctClLYNo ratings yet

- Cat 320dDocument2 pagesCat 320dAlbert EmilyNo ratings yet

- Chapter 16 QuizDocument3 pagesChapter 16 Quizbeckkl05No ratings yet

- Bills 23 Jan 2021Document3 pagesBills 23 Jan 2021Justine RhodesNo ratings yet

- Economic Dev't, PDP SummaryDocument11 pagesEconomic Dev't, PDP SummaryJanell AgananNo ratings yet

- FOMAR-QTN-2019-20-117 Kamat PDFDocument1 pageFOMAR-QTN-2019-20-117 Kamat PDFPriyesh KamatNo ratings yet

- Bonus QuizDocument4 pagesBonus QuizDin Rose GonzalesNo ratings yet

- 20% Development Fund Utilization Report FY 2021Document2 pages20% Development Fund Utilization Report FY 2021edvince mickael bagunas sinonNo ratings yet

- HDFC PresentationDocument9 pagesHDFC Presentationkaran pahujaNo ratings yet

- Oil and Gas BookDocument41 pagesOil and Gas Bookramkumar_me0% (1)

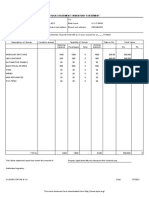

- Stock Statement Format For Bank LoanDocument1 pageStock Statement Format For Bank Loanpsycho Neha40% (5)

- First Name NCFM Id DOB (Dd/mm/yyyy) First Name Last NameDocument15 pagesFirst Name NCFM Id DOB (Dd/mm/yyyy) First Name Last NameTejas ChorageNo ratings yet

- MarshallDocument9 pagesMarshallSam CatlinNo ratings yet