You might also like

- Competitive Strategy: Techniques for Analyzing Industries and CompetitorsFrom EverandCompetitive Strategy: Techniques for Analyzing Industries and CompetitorsRating: 4.5 out of 5 stars4.5/5 (31)

- KFC Case StudyDocument3 pagesKFC Case StudyAnkita shaw100% (2)

- Managerial Economics BasicsDocument31 pagesManagerial Economics Basicsपशुपति नाथ100% (1)

- Micro, Macro, and Managerial Economics RelationshipDocument6 pagesMicro, Macro, and Managerial Economics RelationshipJenz Alemana100% (6)

- CHAP 3 - Industry AnalysisDocument3 pagesCHAP 3 - Industry AnalysisSébastien Robert100% (1)

- Starbucks Coffee's Marketing Mix AnalysisDocument4 pagesStarbucks Coffee's Marketing Mix Analysisa11914212100% (1)

- Review For Chapter 18 and 19Document20 pagesReview For Chapter 18 and 19Steven HouNo ratings yet

- Apple Inc With Macro EnvironmentDocument16 pagesApple Inc With Macro EnvironmentGerhard Potgieter100% (1)

- Introduction To Managerial EconomicsDocument27 pagesIntroduction To Managerial EconomicsRAKIB HOWLADERNo ratings yet

- Asim Sir Notes Unit 1&2Document44 pagesAsim Sir Notes Unit 1&2Vishal kumar singhNo ratings yet

- Economics For Managers Module 1Document89 pagesEconomics For Managers Module 1Abhijit PaulNo ratings yet

- Managerial Economics - Module 1Document130 pagesManagerial Economics - Module 1Supriya JainNo ratings yet

- Introduction of Managerial EconomicsDocument12 pagesIntroduction of Managerial EconomicsS TMNo ratings yet

- Unit - One MEDocument13 pagesUnit - One MEsnreddy85No ratings yet

- Managerial EconomicsDocument104 pagesManagerial Economicskibebew shenkuteNo ratings yet

- Lecture - Salvatore Iare-Mefa-PptsDocument519 pagesLecture - Salvatore Iare-Mefa-PptsKahimbiNo ratings yet

- Managerial Economics Basics - GudDocument23 pagesManagerial Economics Basics - Gudaruna2707No ratings yet

- CH - 1 Managerial Economics Unit 1Document39 pagesCH - 1 Managerial Economics Unit 1Afzal AhmadNo ratings yet

- 1.3 Managerial Eco - Prof.ruchikaDocument69 pages1.3 Managerial Eco - Prof.ruchikaVipin Gupta100% (6)

- Mefa Unit 1 1 PDFDocument22 pagesMefa Unit 1 1 PDFbhuvana vuyyuruNo ratings yet

- 02 Introduction of Managerial EconomicsDocument21 pages02 Introduction of Managerial Economicssubroto36No ratings yet

- Part I: Nature and Scope of Managerial Economics DescriptionDocument8 pagesPart I: Nature and Scope of Managerial Economics DescriptionGamers PhilippinesNo ratings yet

- An Introduction To Managerial Economics: Rajesh KPDocument21 pagesAn Introduction To Managerial Economics: Rajesh KPAnoop CmNo ratings yet

- Introduction of Managerial EconomicsDocument21 pagesIntroduction of Managerial EconomicsSandesh ShettyNo ratings yet

- Managerial Ecnomics-1Document12 pagesManagerial Ecnomics-1Asrat Fikre HenokNo ratings yet

- Managerial EconomicsDocument7 pagesManagerial EconomicsPramodh RobbiNo ratings yet

- 01 - Introduction To Managerial EconomicsDocument23 pages01 - Introduction To Managerial Economicscdkalpita80% (5)

- PPTs ON NATURE AND SCOPE OF MANAGERIAL ECONOMICS-UNIT-IDocument39 pagesPPTs ON NATURE AND SCOPE OF MANAGERIAL ECONOMICS-UNIT-Ipujithavennam123No ratings yet

- Introduction To Managerial EconomicsDocument37 pagesIntroduction To Managerial Economicskishore.vadlamani86% (22)

- Managerial Economics Unit I: Session 1 - 9Document49 pagesManagerial Economics Unit I: Session 1 - 9Abesheik HalduraiNo ratings yet

- Lesson 1 Introduction To EconomicsDocument11 pagesLesson 1 Introduction To Economicsvirgo_17riteshNo ratings yet

- Manageria L Economics: Part 1 - IntroductionDocument16 pagesManageria L Economics: Part 1 - IntroductionAndrea FontiverosNo ratings yet

- Managerial Economics - 1Document36 pagesManagerial Economics - 1Deepi SinghNo ratings yet

- Managerial Economics - MBA I Semester NotesDocument13 pagesManagerial Economics - MBA I Semester NotesSaurabh shahiNo ratings yet

- Managerial Economics Unit IDocument48 pagesManagerial Economics Unit IAbesheik HalduraiNo ratings yet

- ME Version 1Document437 pagesME Version 1gvdshreeharshaNo ratings yet

- UNIT-1 Introduction To Managerial Economics and Demand AnalysisDocument35 pagesUNIT-1 Introduction To Managerial Economics and Demand AnalysisSyamnadh UppalapatiNo ratings yet

- Chapter 1 The Nature Scope and Practice of Managerial EconomicsDocument6 pagesChapter 1 The Nature Scope and Practice of Managerial EconomicsJoyce LagaoNo ratings yet

- Managerial EconomicsDocument227 pagesManagerial Economicssumitadhar05No ratings yet

- Module 1 Managerial EconomicsDocument14 pagesModule 1 Managerial EconomicsD'jeas Shy Smith FuentabellaNo ratings yet

- ME Unit - 1Document12 pagesME Unit - 1Nikhita MayuriNo ratings yet

- Notes Managerial EconomicsDocument34 pagesNotes Managerial EconomicsFaisal ArifNo ratings yet

- Managerial EconDocument20 pagesManagerial Econnatalie clyde matesNo ratings yet

- Notes Business Economics - NotesDocument33 pagesNotes Business Economics - Notestheirontemple03No ratings yet

- Unit - 1 Basics of Managerial Economics LESSON 1-Introduction To EconomicsDocument5 pagesUnit - 1 Basics of Managerial Economics LESSON 1-Introduction To EconomicspraneixNo ratings yet

- Unit 1 Introduction To Managerial EconomicsDocument8 pagesUnit 1 Introduction To Managerial EconomicsRahul GoyalNo ratings yet

- Managerial EconomicsDocument78 pagesManagerial EconomicsparveenajeemNo ratings yet

- Unit-I Mefa MaterialDocument41 pagesUnit-I Mefa MaterialTejaswini KarmakondaNo ratings yet

- Managerial EconomicsDocument36 pagesManagerial Economicskhan babaNo ratings yet

- Introduction of Managerial Economics1Document15 pagesIntroduction of Managerial Economics1ridhiNo ratings yet

- Assignment # 1Document5 pagesAssignment # 1Imtiaz SultanNo ratings yet

- Managerial EconomicsDocument238 pagesManagerial EconomicsRAMA RAJU PYDINo ratings yet

- Concept of Economics and Business EconomicsDocument12 pagesConcept of Economics and Business EconomicsSajib IslamNo ratings yet

- Introduction To Economics and Managerial EconomicsDocument16 pagesIntroduction To Economics and Managerial Economicsdj_rocs100% (3)

- Managerial EconomicsDocument9 pagesManagerial Economicsjlorajesminmg025No ratings yet

- Unit 1 Mefa Material-Word DocumentDocument33 pagesUnit 1 Mefa Material-Word DocumentrosieNo ratings yet

- Mefa 1 &2 UnitsDocument40 pagesMefa 1 &2 UnitsshivaniNo ratings yet

- Managerial ECONOMICS PPT 1 PDFDocument27 pagesManagerial ECONOMICS PPT 1 PDFJerwin FajardoNo ratings yet

- Chapter 1 Managerial Lecture 1Document34 pagesChapter 1 Managerial Lecture 1Bereket RegassaNo ratings yet

- Translating Strategy into Shareholder Value: A Company-Wide Approach to Value CreationFrom EverandTranslating Strategy into Shareholder Value: A Company-Wide Approach to Value CreationNo ratings yet

- Summer Training Report On Hero MotocorpDocument15 pagesSummer Training Report On Hero MotocorpSaurav093No ratings yet

- Final Report StarbucksDocument16 pagesFinal Report Starbucksmurary123100% (1)

- The Ten Types of Innovation (Doblin Inc.)Document1 pageThe Ten Types of Innovation (Doblin Inc.)Berry CheungNo ratings yet

- Abhra Bhattacharyya Kumar Gaurav Narendra Singh Rana Vishal Deep Sharma Vinay Kumar Singh Vivek KantDocument23 pagesAbhra Bhattacharyya Kumar Gaurav Narendra Singh Rana Vishal Deep Sharma Vinay Kumar Singh Vivek KantNavya AgarwalNo ratings yet

- Lesson 2 - Cost, Design Economics and Break-Even AnalysisDocument25 pagesLesson 2 - Cost, Design Economics and Break-Even AnalysisNeil Ivan Ballesta DimatulacNo ratings yet

- Premium TeaDocument24 pagesPremium TeaCurvex Ground100% (3)

- FairWild Industry Guidance Final FAQsDocument2 pagesFairWild Industry Guidance Final FAQsbvfgtgbkmkgmNo ratings yet

- Starting Up Your Own Poultry Farm (Configured) PDFDocument11 pagesStarting Up Your Own Poultry Farm (Configured) PDFallan variasNo ratings yet

- Managerial Economics Answer All QuestionsDocument8 pagesManagerial Economics Answer All Questionsajeet gautam67% (3)

- Journal #2, Nirvana AlcarazDocument2 pagesJournal #2, Nirvana AlcarazpooinmymoufhNo ratings yet

- Britania Case StudyDocument20 pagesBritania Case StudyWeevy Khernamnuai100% (1)

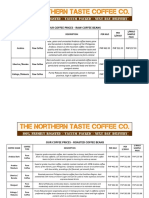

- The Northern Taste Coffee Co. Price ListDocument5 pagesThe Northern Taste Coffee Co. Price Listparing pilipinoNo ratings yet

- PDCA BimboDocument5 pagesPDCA BimboCesar De LeonNo ratings yet

- Assignment On US Trade HypocrisyDocument1 pageAssignment On US Trade HypocrisyacidreignNo ratings yet

- 22 Wang - Wen ChengDocument8 pages22 Wang - Wen Chengwahid_040No ratings yet

- Westside News: Westside Wins 'Most Admired Retailer of The Year' AwardDocument4 pagesWestside News: Westside Wins 'Most Admired Retailer of The Year' AwardTanvi DoshiNo ratings yet

- Customer Loyalty & Private Label Products: KPMG Global Consumer MarketsDocument36 pagesCustomer Loyalty & Private Label Products: KPMG Global Consumer Marketsramjee prasad jaiswalNo ratings yet

- Zespri Final AlternativeDocument46 pagesZespri Final Alternativeapi-58835638100% (1)

- Demand AnalysisDocument59 pagesDemand AnalysisAnonymous 39nG7JAWJI50% (2)

- AnwayDocument13 pagesAnwayRadhika MohataNo ratings yet

- Report ShikhaDocument8 pagesReport ShikhaVaibhav SinghNo ratings yet

- Scrap Scenarios Process HandlingDocument2 pagesScrap Scenarios Process HandlingRam Manohar100% (1)

- Managerial EconomicsDocument34 pagesManagerial EconomicsHashma KhanNo ratings yet

- Nishat Textile Mills (Strategic Management)Document5 pagesNishat Textile Mills (Strategic Management)flavia1286No ratings yet

- Demonstrate Understanding of The 4M's of OperationDocument9 pagesDemonstrate Understanding of The 4M's of OperationDyuli DyulsNo ratings yet