You might also like

- Credit Risk Project PDFDocument104 pagesCredit Risk Project PDFDenish PatelNo ratings yet

- ANALYZING CREDIT APPRAISAL AND TRADE FINANCE AT BANK OF INDIADocument68 pagesANALYZING CREDIT APPRAISAL AND TRADE FINANCE AT BANK OF INDIAArisha ChoudharyNo ratings yet

- Main Project PDFDocument56 pagesMain Project PDFNaira Puneet BhatiaNo ratings yet

- Banking Credit Risk Analysis With Naive Bayes Approach and Cox Proportional HazardDocument6 pagesBanking Credit Risk Analysis With Naive Bayes Approach and Cox Proportional HazardIJAERS JOURNALNo ratings yet

- Strategic Credit Management - IntroductionDocument14 pagesStrategic Credit Management - IntroductionDr VIRUPAKSHA GOUD G50% (2)

- ICRRS Guidelines - BB - Version 2.0Document25 pagesICRRS Guidelines - BB - Version 2.0Optimistic EyeNo ratings yet

- Literature Review: Retail Credit Scoring: Context and IssuesDocument14 pagesLiterature Review: Retail Credit Scoring: Context and IssuesNedjma AchNo ratings yet

- Credit Risk ModelingDocument4 pagesCredit Risk ModelingmohamedciaNo ratings yet

- Banking Sector NPAs ReportDocument23 pagesBanking Sector NPAs ReportStuti Sharma GaurNo ratings yet

- Credit Risk ManagementDocument16 pagesCredit Risk Managementkrishnalohia9No ratings yet

- Fair Lending Compliance: Intelligence and Implications for Credit Risk ManagementFrom EverandFair Lending Compliance: Intelligence and Implications for Credit Risk ManagementNo ratings yet

- Credit ManagementDocument15 pagesCredit Managementb.mars100% (2)

- Financial markets, treasury functions, and risk management in banksDocument12 pagesFinancial markets, treasury functions, and risk management in banksDiwakar PasrichaNo ratings yet

- Credit Risk Grading-Apex TanneryDocument21 pagesCredit Risk Grading-Apex TanneryAbdullahAlNomunNo ratings yet

- Slide-19B-Capital Adequacy Framework For Banks & BASEl I, II & III Capital AccordDocument64 pagesSlide-19B-Capital Adequacy Framework For Banks & BASEl I, II & III Capital AccordRahul ParateNo ratings yet

- Default of Credit Card ClientsDocument27 pagesDefault of Credit Card ClientsdeepuNo ratings yet

- Measuring and Managing Operational Risk Under Basel IIDocument34 pagesMeasuring and Managing Operational Risk Under Basel IITammie HendersonNo ratings yet

- Capstone Project NBFC Loan Foreclosure PredictionDocument48 pagesCapstone Project NBFC Loan Foreclosure PredictionAbhay PoddarNo ratings yet

- IIBFDocument8 pagesIIBFSonia ChauhanNo ratings yet

- Analytics Center Of Excellence A Complete Guide - 2021 EditionFrom EverandAnalytics Center Of Excellence A Complete Guide - 2021 EditionNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Issues in Credit Scoring: Model Development and ValidationDocument22 pagesIssues in Credit Scoring: Model Development and ValidationbusywaghNo ratings yet

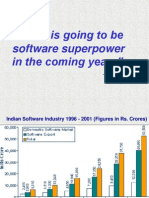

- India's Growing Software Industry and ExportsDocument57 pagesIndia's Growing Software Industry and ExportsMona LallNo ratings yet

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- Credit RiskDocument37 pagesCredit RiskWakas KhalidNo ratings yet

- Credit Worthiness: What Is A Corporate Credit RatingDocument23 pagesCredit Worthiness: What Is A Corporate Credit RatingSudarshan ChitlangiaNo ratings yet

- DICO-IfRS 9 Modelling and ImplementationDocument28 pagesDICO-IfRS 9 Modelling and ImplementationRadian Adhi100% (1)

- Credit Risk SiDocument90 pagesCredit Risk SiSampath SanguNo ratings yet

- CAIIB ABM Study Material MacMillanDocument239 pagesCAIIB ABM Study Material MacMillanSreejith BhattathiriNo ratings yet

- RSKMGT NIBM Module Operational Risk Under Basel IIIDocument6 pagesRSKMGT NIBM Module Operational Risk Under Basel IIIKumar SkandaNo ratings yet

- Credit Risk Mgmt. at ICICIDocument60 pagesCredit Risk Mgmt. at ICICIRikesh Daliya100% (1)

- Project On Credit Default Swaps in IndiaDocument102 pagesProject On Credit Default Swaps in IndiaPraveen Mishall100% (1)

- Financial Risk Analysis: Great Learning PGPBABI 2017Document25 pagesFinancial Risk Analysis: Great Learning PGPBABI 2017AbhishekNo ratings yet

- Credit Appraisal Process of Sbi: A Case Study of Branch of Sbi in HisarDocument1 pageCredit Appraisal Process of Sbi: A Case Study of Branch of Sbi in Hisarnbtamana4No ratings yet

- FINANCIAL INCLUSION DECISIONSDocument12 pagesFINANCIAL INCLUSION DECISIONSgurjit20No ratings yet

- Quantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskFrom EverandQuantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskRating: 3.5 out of 5 stars3.5/5 (1)

- Pradhanmantri Jan Dhan Yojana: Finatix Club IIM RaipurDocument10 pagesPradhanmantri Jan Dhan Yojana: Finatix Club IIM RaipurYadvendra YadavNo ratings yet

- Expert Banking Credit System for Intelligent DecisionsDocument32 pagesExpert Banking Credit System for Intelligent DecisionsBilal Ilyas100% (1)

- Credit Risk SasDocument152 pagesCredit Risk SasShreyas DalviNo ratings yet

- KMV - Ved PureshwarDocument45 pagesKMV - Ved PureshwarAmit KawleNo ratings yet

- Investment TemplateDocument86 pagesInvestment TemplateLeonard KendrickNo ratings yet

- Clustering Approaches For Financial Data Analysis PDFDocument7 pagesClustering Approaches For Financial Data Analysis PDFNewton LinchenNo ratings yet

- Retail Lending PrinciplesDocument22 pagesRetail Lending PrinciplesViji Ranga25% (4)

- To Study The Mergers and Acquisitions in Banking SectorDocument42 pagesTo Study The Mergers and Acquisitions in Banking SectorAayush UpadhyayNo ratings yet

- BASEL I, II, III-uDocument43 pagesBASEL I, II, III-uMomil FatimaNo ratings yet

- Credit Risk MGMTDocument4 pagesCredit Risk MGMTmail2ncNo ratings yet

- Canara BankDocument18 pagesCanara BankKripa Mary JosephNo ratings yet

- Transfer Pricing - Pitfalls in Using Multiple Benchmark Yield CurvesDocument6 pagesTransfer Pricing - Pitfalls in Using Multiple Benchmark Yield CurvesPoonsiri WongwiseskijNo ratings yet

- Data Mining and Credit ScoringDocument8 pagesData Mining and Credit ScoringHaniyaAngelNo ratings yet

- C-Kyc Frequently Asked Questions (Faq) : Section A: General FaqsDocument9 pagesC-Kyc Frequently Asked Questions (Faq) : Section A: General FaqsAnuj KumarNo ratings yet

- Types of Motivation in Language LearningDocument8 pagesTypes of Motivation in Language LearningAlya IrmasyahNo ratings yet

- A Cause For Our Times: Oxfam - The First 50 YearsDocument81 pagesA Cause For Our Times: Oxfam - The First 50 YearsOxfamNo ratings yet

- Packex IndiaDocument12 pagesPackex IndiaSam DanNo ratings yet

- Climate Bogeyman3 PDFDocument199 pagesClimate Bogeyman3 PDFIonel Leon100% (1)

- Teaching As Noble ProfessionDocument1 pageTeaching As Noble ProfessionJeric AcostaNo ratings yet

- g6 Sws ArgDocument5 pagesg6 Sws Argapi-202727113No ratings yet

- Sadie's Drawing Materials: Buy Your Supplies atDocument5 pagesSadie's Drawing Materials: Buy Your Supplies atAlison De Sando ManzoniNo ratings yet

- Architecture Floor Plan Abbreviations AnDocument11 pagesArchitecture Floor Plan Abbreviations AnGraphitti Koncepts and DesignsNo ratings yet

- ResMed Case Study AnalysisDocument12 pagesResMed Case Study Analysis徐芊芊No ratings yet

- SCM Software Selection and EvaluationDocument3 pagesSCM Software Selection and EvaluationBhuwneshwar PandayNo ratings yet

- SYLLABUS FYUP-PoliticalScience PDFDocument105 pagesSYLLABUS FYUP-PoliticalScience PDFIshta VohraNo ratings yet

- KluberDocument20 pagesKluberJako MishyNo ratings yet

- Application Registry Edits: Customize Windows Media Player Title BarDocument29 pagesApplication Registry Edits: Customize Windows Media Player Title BarSuseendran SomasundaramNo ratings yet

- The Merchant of Venice QuestionsDocument9 pagesThe Merchant of Venice QuestionsHaranath Babu50% (4)

- Update in Living Legal Ethics - Justice Dela CruzDocument13 pagesUpdate in Living Legal Ethics - Justice Dela CruzRobert F Catolico IINo ratings yet

- Postpaid Bill AugDocument2 pagesPostpaid Bill Augsiva vNo ratings yet

- Fishblade RPGDocument1 pageFishblade RPGthe_doom_dudeNo ratings yet

- TenorsDocument74 pagesTenorsaris100% (1)

- Criteria For Judging MR and Ms UNDocument9 pagesCriteria For Judging MR and Ms UNRexon ChanNo ratings yet

- In The Matter of The Adoption of Elizabeth MiraDocument2 pagesIn The Matter of The Adoption of Elizabeth MiradelayinggratificationNo ratings yet

- Proposal to Enhance Science InstructionDocument4 pagesProposal to Enhance Science InstructionAzzel ArietaNo ratings yet

- A. Pawnshops 4. B. Pawner 5. C. Pawnee D. Pawn 6. E. Pawn Ticket 7. F. Property G. Stock H. Bulky Pawns 8. I. Service Charge 9. 10Document18 pagesA. Pawnshops 4. B. Pawner 5. C. Pawnee D. Pawn 6. E. Pawn Ticket 7. F. Property G. Stock H. Bulky Pawns 8. I. Service Charge 9. 10Darwin SolanoyNo ratings yet

- Window On The Wetlands BrochureDocument2 pagesWindow On The Wetlands BrochureliquidityNo ratings yet

- MSDS Hygisoft Surface Disinfectant, Concentrate - PagesDocument5 pagesMSDS Hygisoft Surface Disinfectant, Concentrate - PagesDr. Omar Al-AbbasiNo ratings yet

- Marine Clastic Reservoir Examples and Analogues (Cant 1993) PDFDocument321 pagesMarine Clastic Reservoir Examples and Analogues (Cant 1993) PDFAlberto MysterioNo ratings yet

- Not Qualified (Spoken Word Poem) by JonJorgensonDocument3 pagesNot Qualified (Spoken Word Poem) by JonJorgensonKent Bryan Anderson100% (1)

- Warren BuffetDocument11 pagesWarren BuffetSopakirite Kuruye-AleleNo ratings yet

- What Is ReligionDocument15 pagesWhat Is ReligionMary Glou Melo PadilloNo ratings yet

- TNPSC Vas: NEW SyllabusDocument12 pagesTNPSC Vas: NEW Syllabuskarthivisu2009No ratings yet

- Landman Training ManualDocument34 pagesLandman Training Manualflashanon100% (2)