You might also like

- Introduction to Cost and Management AccountingDocument19 pagesIntroduction to Cost and Management AccountingTilahun GirmaNo ratings yet

- Chapter 2Document17 pagesChapter 2Ngọc Minh Đỗ ChâuNo ratings yet

- Cost Terminology and Cost Behaviors: Learning ObjectivesDocument17 pagesCost Terminology and Cost Behaviors: Learning ObjectivesJonnah ArriolaNo ratings yet

- Cost Terminology and Cost Behaviors: Learning ObjectivesDocument17 pagesCost Terminology and Cost Behaviors: Learning ObjectivesRichard John EcalneNo ratings yet

- Unit Vi - Cost Theory and Estimation: C F (X, T, PF)Document10 pagesUnit Vi - Cost Theory and Estimation: C F (X, T, PF)Bai NiloNo ratings yet

- Chapter 2Document18 pagesChapter 2Hk100% (1)

- Null 2Document10 pagesNull 2siddharthsonar9604No ratings yet

- St. Mary's Cost Accounting Chapter 2 SummaryDocument10 pagesSt. Mary's Cost Accounting Chapter 2 SummaryalemayehuNo ratings yet

- Cost Accounting Concepts ExplainedDocument7 pagesCost Accounting Concepts ExplainedyebegashetNo ratings yet

- Theory of Cost-GoodDocument56 pagesTheory of Cost-Goodyonatan gizawNo ratings yet

- Introduction To Cost Accounting Final With PDFDocument19 pagesIntroduction To Cost Accounting Final With PDFLemon EnvoyNo ratings yet

- Cost Accounting and Control Lecture NotesDocument11 pagesCost Accounting and Control Lecture NotesAnalyn LafradezNo ratings yet

- Chapter 2Document10 pagesChapter 2Aklil TeganewNo ratings yet

- Cost AccountingDocument28 pagesCost Accountinglove_oct22100% (1)

- Cost Terminology and Classification ExplainedDocument8 pagesCost Terminology and Classification ExplainedKanbiro Orkaido100% (1)

- Cost AccountingDocument28 pagesCost Accountingrenjithrkn12No ratings yet

- DSFDFJM LLKDocument27 pagesDSFDFJM LLKDeepak R GoradNo ratings yet

- Cost Accounting and Control: Cagayan State UniversityDocument74 pagesCost Accounting and Control: Cagayan State UniversityAntonNo ratings yet

- Chapter 2Document9 pagesChapter 2Marites AmorsoloNo ratings yet

- Cost Concepts: Cost: Lecture Notes On Module-2Document18 pagesCost Concepts: Cost: Lecture Notes On Module-2ramanarao susarlaNo ratings yet

- CostDocument46 pagesCostsatya narayana100% (1)

- Understand Cost Terminology and BehaviorsDocument12 pagesUnderstand Cost Terminology and BehaviorsCharles Decripito FloresNo ratings yet

- Basic Cost Concepts ExplainedDocument28 pagesBasic Cost Concepts ExplainedCharles GalidoNo ratings yet

- Module 1 and Module 2Document32 pagesModule 1 and Module 2tygurNo ratings yet

- Term Associated With CostDocument6 pagesTerm Associated With Costaashir chNo ratings yet

- Cost ClassificationDocument27 pagesCost ClassificationPooja Gupta SinglaNo ratings yet

- Cost Concepts and Components ExplainedDocument11 pagesCost Concepts and Components ExplainedRaja SahaNo ratings yet

- Cost ClassificationDocument30 pagesCost ClassificationnehaNo ratings yet

- Kinney 8e - CH 02Document16 pagesKinney 8e - CH 02Ashik Uz ZamanNo ratings yet

- BTEC Level 4 HND Diploma in Business Management Accounting AssignmentDocument16 pagesBTEC Level 4 HND Diploma in Business Management Accounting AssignmentMinh Thi TrầnNo ratings yet

- Production and Operations Management Cost ConceptsDocument37 pagesProduction and Operations Management Cost ConceptsYash PathakNo ratings yet

- CostDocument73 pagesCostGada DugoNo ratings yet

- Cost Terms and Concepts-L2-UpdatedDocument23 pagesCost Terms and Concepts-L2-Updatedviony catelinaNo ratings yet

- Costing: Prepared By: Dr. B. K. MawandiyaDocument26 pagesCosting: Prepared By: Dr. B. K. MawandiyaNamanNo ratings yet

- Cost Accounting IntroductionDocument47 pagesCost Accounting IntroductionAkanksha GuptaNo ratings yet

- Theory of CostDocument13 pagesTheory of CostBLOODy aSSault100% (1)

- Costs - Concepts and Classification: JmcnncpaDocument37 pagesCosts - Concepts and Classification: JmcnncpaMari Mar100% (1)

- Cost Analysis: 1) Opportunity Costs and Outlay CostsDocument8 pagesCost Analysis: 1) Opportunity Costs and Outlay Costsakash creationNo ratings yet

- Managerial Accounting and Cost Concepts Cap. 1.: (Introducción y Tipos de Costos)Document15 pagesManagerial Accounting and Cost Concepts Cap. 1.: (Introducción y Tipos de Costos)Eugenio CamposNo ratings yet

- Chap 2 The-Manager-and-Management-AccountingDocument11 pagesChap 2 The-Manager-and-Management-Accountingqgminh7114No ratings yet

- Chapter 1: Cost Sheet (Unit Costing)Document102 pagesChapter 1: Cost Sheet (Unit Costing)Rimsha HanifNo ratings yet

- Accounting 2Document5 pagesAccounting 2jessicaong2403No ratings yet

- Cost and Management Accounting GlossaryDocument13 pagesCost and Management Accounting Glossaryssistece100% (1)

- Economics For Managers Course Cost Analysis ConceptsDocument34 pagesEconomics For Managers Course Cost Analysis Conceptsrifath rafiqNo ratings yet

- Chapter 2 Cost IDocument51 pagesChapter 2 Cost IheysemNo ratings yet

- Lecture 2 Cost Terms, Concepts and ClassificationDocument34 pagesLecture 2 Cost Terms, Concepts and ClassificationTgrh TgrhNo ratings yet

- Basic Cost Management ConceptsDocument7 pagesBasic Cost Management ConceptsImadNo ratings yet

- Group 8 - Chap 2 an Introduction to Cost Terms and PurposeseDocument39 pagesGroup 8 - Chap 2 an Introduction to Cost Terms and Purposeseqgminh7114No ratings yet

- Classifying Costs for Effective ManagementDocument8 pagesClassifying Costs for Effective ManagementMohamaad SihatthNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 2 CostingDocument15 pagesACCT3500 (Fall 20) Lecture and Tutorial 2 CostingMohammad ShabirNo ratings yet

- PDFenDocument68 pagesPDFenKawaii SevennNo ratings yet

- Managerial Accounting and Cost ConceptsDocument14 pagesManagerial Accounting and Cost ConceptsWaseem ChaudharyNo ratings yet

- Unit 2 - Classification of CostDocument4 pagesUnit 2 - Classification of Costavinal malikNo ratings yet

- Module-2: Cost and Revenue, Profit FunctionsDocument37 pagesModule-2: Cost and Revenue, Profit FunctionsArpitha KagdasNo ratings yet

- Cost Classification or Cost Flow in An OrgaizationDocument8 pagesCost Classification or Cost Flow in An OrgaizationvaloruroNo ratings yet

- Week 2 - Lesson 2 Costs in Managerial AccountingDocument7 pagesWeek 2 - Lesson 2 Costs in Managerial AccountingReynold Raquiño AdonisNo ratings yet

- Managerial Accounting Module: Costs in Managerial AccountingDocument7 pagesManagerial Accounting Module: Costs in Managerial AccountingReynold Raquiño AdonisNo ratings yet

- Lecture 1 Cost of ProductionDocument2 pagesLecture 1 Cost of ProductionSagnikNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Assignment AdvDocument4 pagesAssignment AdvTilahun GirmaNo ratings yet

- Short Note 4Document4 pagesShort Note 4Tilahun GirmaNo ratings yet

- Short Not2Document11 pagesShort Not2Tilahun GirmaNo ratings yet

- Comprehensive CostDocument8 pagesComprehensive CostTilahun GirmaNo ratings yet

- Short Note 3Document6 pagesShort Note 3Tilahun GirmaNo ratings yet

- Insurance Contract FundamentalsDocument40 pagesInsurance Contract FundamentalsTilahun GirmaNo ratings yet

- CH 2 CVP AnalysisDocument127 pagesCH 2 CVP AnalysisTilahun GirmaNo ratings yet

- Worksheet Budet Cost IIDocument2 pagesWorksheet Budet Cost IITilahun GirmaNo ratings yet

- Risk Managemennt Chapter 1Document35 pagesRisk Managemennt Chapter 1Tilahun GirmaNo ratings yet

- Chapter 4 Business CombinationsDocument8 pagesChapter 4 Business CombinationsTilahun GirmaNo ratings yet

- Risk Chap 1-3Document33 pagesRisk Chap 1-3Tilahun GirmaNo ratings yet

- Definition of Investment in 40 CharactersDocument11 pagesDefinition of Investment in 40 CharactersTilahun GirmaNo ratings yet

- CVP Analysis Unit 2 Cost Volume ProfitDocument16 pagesCVP Analysis Unit 2 Cost Volume ProfitTilahun GirmaNo ratings yet

- Optimal Use of Limited Resource: Make or Buy DecisionDocument3 pagesOptimal Use of Limited Resource: Make or Buy DecisionTilahun GirmaNo ratings yet

- Perpetual Inventory System. Equipment Used at The Branch Is Carried in The Home OfficeDocument1 pagePerpetual Inventory System. Equipment Used at The Branch Is Carried in The Home OfficeTilahun GirmaNo ratings yet

- Cost and Managerial Accounting IIDocument5 pagesCost and Managerial Accounting IITilahun GirmaNo ratings yet

- Percentage of Completion: Products Units Produced Unit Selling Price at Split-Off Point RequiredDocument1 pagePercentage of Completion: Products Units Produced Unit Selling Price at Split-Off Point RequiredTilahun GirmaNo ratings yet

- CHAPTER ONE InvestDocument12 pagesCHAPTER ONE InvestTilahun GirmaNo ratings yet

- Unit 3 Acct312-UnlockedDocument21 pagesUnit 3 Acct312-UnlockedTilahun GirmaNo ratings yet

- Joint Venture ADV CH1Document8 pagesJoint Venture ADV CH1Tilahun GirmaNo ratings yet

- Calculating VAT, Rental Income Tax, Foreign Income Tax, and Business Income Tax for Ethiopian CompaniesDocument2 pagesCalculating VAT, Rental Income Tax, Foreign Income Tax, and Business Income Tax for Ethiopian CompaniesTilahun GirmaNo ratings yet

- Chapter 1 Research 11Document4 pagesChapter 1 Research 11Tilahun GirmaNo ratings yet

- Chapter 18Document13 pagesChapter 18Kriza Sevilla Matro0% (1)

- Compre H in SiveDocument4 pagesCompre H in SiveTilahun GirmaNo ratings yet

- Ch1 UpdatedDocument10 pagesCh1 UpdatedTilahun GirmaNo ratings yet

- Information Sheet 1 Verify Validity and Accuracy of Payment RequestDocument18 pagesInformation Sheet 1 Verify Validity and Accuracy of Payment RequestTilahun GirmaNo ratings yet

- Kotebe Metropolitan UniversityDocument6 pagesKotebe Metropolitan UniversityTilahun GirmaNo ratings yet

- CH 2Document8 pagesCH 2Tilahun GirmaNo ratings yet

- Accural AccountingDocument15 pagesAccural AccountingTilahun GirmaNo ratings yet

- Fundamentals of Cost Accounting 4th Edition Lanen Test BankDocument33 pagesFundamentals of Cost Accounting 4th Edition Lanen Test Bankjeanbarnettxv9v100% (14)

- Week 11 Budgeting SystemsDocument12 pagesWeek 11 Budgeting SystemsDamien HewNo ratings yet

- DanialDocument56 pagesDanialAbdi Mucee TubeNo ratings yet

- Lecture 1& 2 - Cost Planning and ControlDocument13 pagesLecture 1& 2 - Cost Planning and ControlRans-Nana Kwame-Boateng0% (1)

- Cost Accounting B.Com III YearDocument4 pagesCost Accounting B.Com III Yeartadepalli patanjaliNo ratings yet

- Introduction to Cost and Management AccountingDocument12 pagesIntroduction to Cost and Management AccountingPRAJWALNo ratings yet

- Definition of CostingDocument22 pagesDefinition of CostingmichuttyNo ratings yet

- ERP Tips Validation and SubstitutionDocument34 pagesERP Tips Validation and Substitutionatul_bhatnagar5458100% (1)

- Accounting For Managers Unit IiiDocument10 pagesAccounting For Managers Unit IiiSoumendra RoyNo ratings yet

- Cost 140609031236 Phpapp01Document170 pagesCost 140609031236 Phpapp01Djuke Balks100% (1)

- Archit BBP CO-PA V1 30112010Document32 pagesArchit BBP CO-PA V1 30112010Subhash ReddyNo ratings yet

- Management Accounting 5th SemDocument24 pagesManagement Accounting 5th SemNeha firdoseNo ratings yet

- Flexible Budget and Performance AnalysisDocument22 pagesFlexible Budget and Performance AnalysisttzaxsanNo ratings yet

- Chapter 1: The Accountant'S Role in The Organization: True/FalseDocument9 pagesChapter 1: The Accountant'S Role in The Organization: True/FalseSittie Ainna A. UnteNo ratings yet

- Syllabus ACCO 20073 Cost Accounting and ControlDocument7 pagesSyllabus ACCO 20073 Cost Accounting and ControlCaia VelazquezNo ratings yet

- Academic Preparedness of The Second Year Students in Accountancy ProgramDocument17 pagesAcademic Preparedness of The Second Year Students in Accountancy ProgramHenry James Nepomuceno100% (1)

- Relevant Costs for Decision-MakingDocument43 pagesRelevant Costs for Decision-MakingAiko E. Lara93% (14)

- Labor Cost Control TechniquesDocument19 pagesLabor Cost Control Techniquesnikki abalos100% (1)

- Cost Accounting & Effectiveness For Nursing PracticeDocument6 pagesCost Accounting & Effectiveness For Nursing Practicemerin sunilNo ratings yet

- Module 09Document53 pagesModule 09samaanNo ratings yet

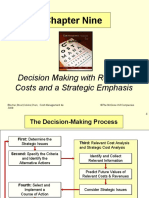

- Chapter Nine: Decision Making With Relevant Costs and A Strategic EmphasisDocument36 pagesChapter Nine: Decision Making With Relevant Costs and A Strategic EmphasisMade Ari HandayaniNo ratings yet

- Course Outline - MA - PGP - AY2023-24 - 28Document5 pagesCourse Outline - MA - PGP - AY2023-24 - 28Nitin JeendgarNo ratings yet

- LCM OPM 2016 Thrivikram PDFDocument39 pagesLCM OPM 2016 Thrivikram PDFsanjayid1980No ratings yet

- Session 5 - Activity-Based CostingDocument8 pagesSession 5 - Activity-Based CostingSong Quỳnh NguyễnNo ratings yet

- Job and Process IDocument19 pagesJob and Process IsajjadNo ratings yet

- Unit 5-Management Accounting-2018 Assignment 2 - Notes LO3Document25 pagesUnit 5-Management Accounting-2018 Assignment 2 - Notes LO3Vân AnnhNo ratings yet

- Fabm1 PPTDocument65 pagesFabm1 PPTBenjie Galicia AngelesNo ratings yet

- Question and Answer - 20Document31 pagesQuestion and Answer - 20acc-expertNo ratings yet

- Lesson 4 Cost and Variance Measures: ContentDocument22 pagesLesson 4 Cost and Variance Measures: ContentajithsubramanianNo ratings yet

- Assessment of Budgetary Performance-33Document10 pagesAssessment of Budgetary Performance-33nurye614No ratings yet