You might also like

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportFrom EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportNo ratings yet

- Thyssenkrupp Industries PDFDocument7 pagesThyssenkrupp Industries PDFBinoy MtNo ratings yet

- Benchmarking Best Practices for Maintenance, Reliability and Asset ManagementFrom EverandBenchmarking Best Practices for Maintenance, Reliability and Asset ManagementNo ratings yet

- Deepak Nitrite R 22082019Document7 pagesDeepak Nitrite R 22082019SalmanNo ratings yet

- Century Plyboards (India) Limited: Summary of Rated Instruments Instrument Rated Amount (In Crore) Rating ActionDocument8 pagesCentury Plyboards (India) Limited: Summary of Rated Instruments Instrument Rated Amount (In Crore) Rating ActionDeepakNo ratings yet

- Pricol Limited - Broker Research - 2017 PDFDocument25 pagesPricol Limited - Broker Research - 2017 PDFnishthaNo ratings yet

- Ace Designers-R-05042018 PDFDocument7 pagesAce Designers-R-05042018 PDFkachadaNo ratings yet

- Indo German Carbons - R - 22052018Document7 pagesIndo German Carbons - R - 22052018Vinu VaviNo ratings yet

- HindalcoDocument26 pagesHindalcoAbhinav PrakashNo ratings yet

- Godrej Industries LimitedDocument8 pagesGodrej Industries LimitedJigarNo ratings yet

- Gay Shut UmDocument7 pagesGay Shut Umsaaransh besoyaNo ratings yet

- Reliance Industries LimitedDocument21 pagesReliance Industries Limitedjaikumar608jainNo ratings yet

- Hikal ResearchNote 09oct2012Document15 pagesHikal ResearchNote 09oct2012equityanalystinvestorNo ratings yet

- Whirlpool of India LTD - Initiating CoverageDocument18 pagesWhirlpool of India LTD - Initiating CoverageBorn StarNo ratings yet

- Symphony LTD (SYMCOM) : Dominant Play in Air CoolingDocument23 pagesSymphony LTD (SYMCOM) : Dominant Play in Air CoolingrohitcoepNo ratings yet

- Reliance Industries Fundamental PDFDocument6 pagesReliance Industries Fundamental PDFsantosh kumariNo ratings yet

- Airvision India Private Limited - R - 25082020Document7 pagesAirvision India Private Limited - R - 25082020DarshanNo ratings yet

- Padget Electronics Pvt. LTDDocument9 pagesPadget Electronics Pvt. LTDvenkyniyerNo ratings yet

- Tube Investments of India LimitedDocument8 pagesTube Investments of India Limitedpraveen kumarNo ratings yet

- Section C - Group No 9 - FA ProjectDocument5 pagesSection C - Group No 9 - FA ProjectAnushka JindalNo ratings yet

- AVI Oil India Private LimitedDocument7 pagesAVI Oil India Private LimitedAkshay keerNo ratings yet

- Anupam Rasayan India Limited IPO Note-202103102014074255053Document12 pagesAnupam Rasayan India Limited IPO Note-202103102014074255053sureshvadNo ratings yet

- Patels Airtemp (India) LimitedDocument5 pagesPatels Airtemp (India) LimitedAnkit LohiyaNo ratings yet

- SJS Enterprises LimitedDocument7 pagesSJS Enterprises LimitedCA Ankur BariaNo ratings yet

- IOCL FinalDocument6 pagesIOCL FinalAnushka JindalNo ratings yet

- Signode India Financial ReportDocument5 pagesSignode India Financial Reportsaikiran reddyNo ratings yet

- Directors' Report: Financial ResultsDocument18 pagesDirectors' Report: Financial ResultskalaswamiNo ratings yet

- Northern Arc Capital - R-01072019Document10 pagesNorthern Arc Capital - R-01072019vaibhav khandelwalNo ratings yet

- Medreich LimitedDocument7 pagesMedreich LimitedAnishNo ratings yet

- Atul LTDDocument4 pagesAtul LTDFast SwiftNo ratings yet

- Chairman highlights challenges and opportunities in annual reportDocument68 pagesChairman highlights challenges and opportunities in annual reportMohan RajNo ratings yet

- Ar08052012rDocument220 pagesAr08052012rSneha DaswaniNo ratings yet

- Rane Engine Valve Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument7 pagesRane Engine Valve Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActiontomNo ratings yet

- Deepak Phenolics Limited: Summary of Rated InstrumentsDocument7 pagesDeepak Phenolics Limited: Summary of Rated Instrumentsvarun GarjeNo ratings yet

- Corporate Strategy Business Strategy: Types of StrategiesDocument34 pagesCorporate Strategy Business Strategy: Types of StrategiesSayed WahabNo ratings yet

- Acknit Industries Limited: Summary of Rating ActionDocument7 pagesAcknit Industries Limited: Summary of Rating ActionprasanthNo ratings yet

- India Ratings Places Dishman Carbogen Amics On RWE Withdraws CP RatingDocument4 pagesIndia Ratings Places Dishman Carbogen Amics On RWE Withdraws CP Ratingabu141No ratings yet

- SFM Cia 1Document13 pagesSFM Cia 1thememeswala7546No ratings yet

- Fine Organic Industries - R - 17012020Document8 pagesFine Organic Industries - R - 17012020Sameer NaikNo ratings yet

- Linde India 250917Document10 pagesLinde India 250917chhayaNo ratings yet

- Rating Rationale CRISILDocument10 pagesRating Rationale CRISILjagadeeshNo ratings yet

- Ril Ar 2011-12 - 07052012Document220 pagesRil Ar 2011-12 - 07052012Indrajit DattaNo ratings yet

- United Breweries Limited: Summary of Rated InstrumentsDocument8 pagesUnited Breweries Limited: Summary of Rated InstrumentsKaushikDasguptaNo ratings yet

- Triveni TurbineDocument6 pagesTriveni TurbinevikasNo ratings yet

- LNT AnalysisDocument7 pagesLNT AnalysisGagan KarwarNo ratings yet

- Anthem Biosciences-R-21052018Document7 pagesAnthem Biosciences-R-21052018swarnaNo ratings yet

- Epicenter Technologies Private - R - 11082020Document7 pagesEpicenter Technologies Private - R - 11082020Shawn BlazeNo ratings yet

- Apollo Tyres Ratings Reaffirmed Despite Large CapexDocument4 pagesApollo Tyres Ratings Reaffirmed Despite Large Capexragha_4544vNo ratings yet

- Electromech Material R 08022018Document8 pagesElectromech Material R 08022018amol_patil51429514No ratings yet

- Assignment On Annual ReportsDocument4 pagesAssignment On Annual ReportsPranay JainNo ratings yet

- Hikal Limited - R - 21122020Document8 pagesHikal Limited - R - 21122020CA.Chandra SekharNo ratings yet

- RIL Macquarie 10 July 06Document50 pagesRIL Macquarie 10 July 06alokkuma05No ratings yet

- Ajax Fiori-R-07092017Document7 pagesAjax Fiori-R-07092017parimal.rodeNo ratings yet

- LGB Q4FY12Update 05may2012Document4 pagesLGB Q4FY12Update 05may2012equityanalystinvestorNo ratings yet

- IKIO Lighting Limited IPO Note-202306061142401796772Document26 pagesIKIO Lighting Limited IPO Note-202306061142401796772HarshNo ratings yet

- RilDocument220 pagesRiljainsasaNo ratings yet

- Chiripal Poly R 08092017Document7 pagesChiripal Poly R 08092017Saurabh JainNo ratings yet

- Happy ForgingsDocument7 pagesHappy ForgingsArshChandraNo ratings yet

- Dhanuka Laboratories LimitedDocument8 pagesDhanuka Laboratories LimitedDarshanNo ratings yet

- Drools Pet Food Private LimitedDocument6 pagesDrools Pet Food Private Limitedkasimmalnas.ipsNo ratings yet

- Companiees DataDocument51 pagesCompaniees Datasales100% (1)

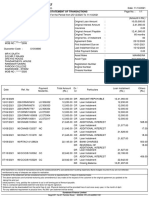

- Statement of Transactions: Sundaram Finance LimitedDocument1 pageStatement of Transactions: Sundaram Finance LimitedBhavin SagarNo ratings yet

- Toaz - Info Data 1xlsx PRDocument1,033 pagesToaz - Info Data 1xlsx PRBhavin SagarNo ratings yet

- Qtrly - Reportq1 FY 2008 2009Document2 pagesQtrly - Reportq1 FY 2008 2009Bhavin SagarNo ratings yet

- Bse Sme Ipo IndexDocument4 pagesBse Sme Ipo IndexBhavin SagarNo ratings yet

- Yap 31 1 19Document345 pagesYap 31 1 19Bhavin SagarNo ratings yet

- CPhI China'09Document1 pageCPhI China'09Bhavin SagarNo ratings yet

- Revised Underwriting Agreement 31.03Document14 pagesRevised Underwriting Agreement 31.03Bhavin SagarNo ratings yet

- Amalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDDocument10 pagesAmalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDBhavin SagarNo ratings yet

- Revised Market Making Agreement 31.03Document13 pagesRevised Market Making Agreement 31.03Bhavin SagarNo ratings yet

- Amalgamation - Share India Securities - Turnaround Corporate AdvisorsDocument5 pagesAmalgamation - Share India Securities - Turnaround Corporate AdvisorsBhavin SagarNo ratings yet

- August 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsDocument10 pagesAugust 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsBhavin SagarNo ratings yet

- Enigma IndiabuilsDocument36 pagesEnigma IndiabuilsKaran Mehta50% (2)

- Nebbia Mutual NDADocument3 pagesNebbia Mutual NDABhavin SagarNo ratings yet

- Revised RV - Draft Valuation Report - Hakuna MatataDocument11 pagesRevised RV - Draft Valuation Report - Hakuna MatataBhavin SagarNo ratings yet

- Capital Reduction - Escorts LTD - GalacticoDocument10 pagesCapital Reduction - Escorts LTD - GalacticoBhavin SagarNo ratings yet

- Underwriters AgreementDocument15 pagesUnderwriters AgreementBhavin SagarNo ratings yet

- List of Valuation ReportsDocument18 pagesList of Valuation ReportsBhavin SagarNo ratings yet

- piVentures-Term Sheet - TemplateDocument6 pagespiVentures-Term Sheet - TemplateBhavin SagarNo ratings yet

- Demerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiDocument4 pagesDemerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiBhavin SagarNo ratings yet

- Removed HEM SECURITIES - MAGAZINE - DEC (8) - 5Document1 pageRemoved HEM SECURITIES - MAGAZINE - DEC (8) - 5Bhavin SagarNo ratings yet

- NDADocument7 pagesNDABhavin SagarNo ratings yet

- piVentures-Term Sheet - TemplateDocument6 pagespiVentures-Term Sheet - TemplateBhavin SagarNo ratings yet

- Overall Strategies For All VerticalsDocument2 pagesOverall Strategies For All VerticalsBhavin SagarNo ratings yet

- 7868 01 Spaceship Roadmap Concept For Powerpoint 16x9Document5 pages7868 01 Spaceship Roadmap Concept For Powerpoint 16x9Bhavin SagarNo ratings yet

- Performance of Sectoral Indices - 2021Document80 pagesPerformance of Sectoral Indices - 2021Bhavin SagarNo ratings yet

- Revised SME IPO Data Performers 2021Document13 pagesRevised SME IPO Data Performers 2021Bhavin SagarNo ratings yet

- 02 Corporate Orange Powerpoint Presentations 16x9 1Document13 pages02 Corporate Orange Powerpoint Presentations 16x9 1Bhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- ICRA Limited Final Placements 2010Document17 pagesICRA Limited Final Placements 2010Sandeep ReddyNo ratings yet

- HRM ImpDocument18 pagesHRM ImpPriyanka RajputNo ratings yet

- WACC - Calculation - DELOITE Macedonija Telecom 2009Document18 pagesWACC - Calculation - DELOITE Macedonija Telecom 2009nanamilecaNo ratings yet

- C3 Credit RatingDocument1 pageC3 Credit RatingGAME OVERNo ratings yet

- Country RiskDocument13 pagesCountry RiskruchiwadhawancaNo ratings yet

- Guidelines For Culminating ActivityDocument3 pagesGuidelines For Culminating Activitychris areola100% (1)

- LEEA-053 Guidance On Hand Chain BlocksDocument3 pagesLEEA-053 Guidance On Hand Chain Blockssuhailpm0% (1)

- Project Report On Credit RatingDocument15 pagesProject Report On Credit RatingShambhu Kumar100% (4)

- Case Study 1Document4 pagesCase Study 1Aqil Ur Rehman54% (13)

- Suguna Electroplaters EvaluationDocument3 pagesSuguna Electroplaters EvaluationSaravanan PNo ratings yet

- APRM Guidebook March2018Document15 pagesAPRM Guidebook March20188612959No ratings yet

- 41163TAD5 ProspectusDocument182 pages41163TAD5 ProspectusBrittany LewisNo ratings yet

- Dahej Standby Jetty 2264Document9 pagesDahej Standby Jetty 2264Anonymous i3lI9MNo ratings yet

- Feasibility StudyDocument1 pageFeasibility Studykalu420No ratings yet

- Direct Labor Variance ExampleDocument1 pageDirect Labor Variance ExampleImperoCo LLCNo ratings yet

- Tata Steel Balance Sheet 2005-06Document172 pagesTata Steel Balance Sheet 2005-06karthikrmNo ratings yet

- ReportDocument1 pageReportumaganNo ratings yet

- Grey Market For Ipos in India: Its Trading Mechanism and Implications For Ipo UnderpricingDocument20 pagesGrey Market For Ipos in India: Its Trading Mechanism and Implications For Ipo UnderpricingNitin BasoyaNo ratings yet

- Graphical Rating ScalesDocument11 pagesGraphical Rating ScalespapanavishekNo ratings yet

- AkshDocument20 pagesAkshNitin KamcoNo ratings yet

- Annual Audit Plan Prepared by Alvarez, LealynDocument30 pagesAnnual Audit Plan Prepared by Alvarez, LealynGerlyn Garcia100% (2)

- Liverage Brigham Case SolutionDocument8 pagesLiverage Brigham Case SolutionShahid Mehmood100% (1)

- Hotel BaliDocument2 pagesHotel BaliJimmyNo ratings yet

- BISE Multan: Fee Structure: Conduct BranchDocument3 pagesBISE Multan: Fee Structure: Conduct BranchQandeelKhanNo ratings yet

- Fresh Fruit ReceptionDocument2 pagesFresh Fruit ReceptionhaysnamripNo ratings yet

- Credit Rating Agencies in IndiaDocument23 pagesCredit Rating Agencies in Indiaanon_315460204No ratings yet

- Manual XiiDocument868 pagesManual XiiyogeshdagaurNo ratings yet

- Article - How Do CFOs Make Capital Budgeting and Capital Structure DecisionsDocument16 pagesArticle - How Do CFOs Make Capital Budgeting and Capital Structure DecisionsmssanNo ratings yet

- Credit RatingDocument46 pagesCredit RatingMahak KhemkaNo ratings yet