You might also like

- Amended Articles of Incorporation ofDocument17 pagesAmended Articles of Incorporation ofxenoyewNo ratings yet

- BIR Accreditation For CPAsDocument1 pageBIR Accreditation For CPAsECMH ACCOUNTING AND CONSULTANCY SERVICESNo ratings yet

- Integrity Pledge For Certified Public AccountantsDocument1 pageIntegrity Pledge For Certified Public AccountantsromabooNo ratings yet

- BOARD RESOLUTION Appropriation of REDocument2 pagesBOARD RESOLUTION Appropriation of REFamily FriendsNo ratings yet

- Death Note RulesDocument10 pagesDeath Note RulesShiraMeikoNo ratings yet

- Transferring Deposits for Future Stock Subscriptions Tax ImplicationsDocument2 pagesTransferring Deposits for Future Stock Subscriptions Tax ImplicationsCkey ArNo ratings yet

- RR 2-98Document85 pagesRR 2-98Elaine LatonioNo ratings yet

- Management Representation Letter AuditDocument5 pagesManagement Representation Letter AuditKiran NanduNo ratings yet

- RR No. 11-2018Document47 pagesRR No. 11-2018Micah Adduru - RoblesNo ratings yet

- Estate Tax Amnesty: An Overview of the Proposed Program and Features of Tax Amnesty Programs in Other CountriesDocument41 pagesEstate Tax Amnesty: An Overview of the Proposed Program and Features of Tax Amnesty Programs in Other CountriesCourt Nanquil100% (1)

- RR 8-98Document3 pagesRR 8-98matinikkiNo ratings yet

- Board Resolution Approving Sale of AssetsDocument0 pagesBoard Resolution Approving Sale of AssetsshekhawatrNo ratings yet

- Remedies of Landowners Whose Property Is Occupied by Informal SettlersDocument5 pagesRemedies of Landowners Whose Property Is Occupied by Informal Settlersracs_arcrNo ratings yet

- About The Canon - Encyclopaedia Judaica (Vol. III)Document17 pagesAbout The Canon - Encyclopaedia Judaica (Vol. III)Arllington R. F. da CostaNo ratings yet

- Estate Settlement GuidelinesDocument4 pagesEstate Settlement GuidelinesOfel TactacNo ratings yet

- Authority To Print 2013 - SynerquestDocument3 pagesAuthority To Print 2013 - SynerquestrobinrubinaNo ratings yet

- Ra 4200Document34 pagesRa 4200sajdy100% (1)

- Guidelines On Land AcquisitionDocument3 pagesGuidelines On Land Acquisitionirwinariel mielNo ratings yet

- Overview of Handling BIR Tax Audit in The PhilippinesDocument3 pagesOverview of Handling BIR Tax Audit in The PhilippinesMarietta Fragata Ramiterre100% (2)

- PPC Audit Finds P54M in Government Assets UninsuredDocument4 pagesPPC Audit Finds P54M in Government Assets UninsuredmocsNo ratings yet

- SEC Opinion Re Change of Principal AddressDocument5 pagesSEC Opinion Re Change of Principal AddressLRMNo ratings yet

- Affidavit of Non Operation (BIR)Document2 pagesAffidavit of Non Operation (BIR)Kaiser Delos Cientos Narciso100% (8)

- Execom Res No 001 s2017Document14 pagesExecom Res No 001 s2017Teff Quibod71% (7)

- Articles of Incorporation SampleDocument8 pagesArticles of Incorporation SampleLeevan Roy YapNo ratings yet

- Engagement LetterDocument3 pagesEngagement LetterRathan Mat100% (1)

- GST Basics and AccountingDocument30 pagesGST Basics and AccountingHarnitNo ratings yet

- Additonal Disclosure RR 15 2010Document5 pagesAdditonal Disclosure RR 15 2010Emil A. MolinaNo ratings yet

- OM No. 2018-04-03Document2 pagesOM No. 2018-04-03Christian Albert HerreraNo ratings yet

- Ramo 1-2019Document74 pagesRamo 1-2019Donato Vergara IIINo ratings yet

- A.M. 04-3-15-scDocument17 pagesA.M. 04-3-15-scErly Ecal100% (1)

- Petition To Revisit Denial of AIPO Renewal PDFDocument87 pagesPetition To Revisit Denial of AIPO Renewal PDFEM Gesmundo SevillaNo ratings yet

- PROPOSED NOTES ON TAXESDocument9 pagesPROPOSED NOTES ON TAXESMary Grace Caguioa AgasNo ratings yet

- Givvy Mobile App Terms of Service SummaryDocument14 pagesGivvy Mobile App Terms of Service Summaryali esquerNo ratings yet

- SEC Memo 11-08Document9 pagesSEC Memo 11-08Matthew TiuNo ratings yet

- This Study Resource Was: Revenue Regulations No. 9-98Document6 pagesThis Study Resource Was: Revenue Regulations No. 9-98Cyruss Xavier Maronilla NepomucenoNo ratings yet

- List of Mandatory Documentary Requirements and Procedure (RD Extrajudicial Settlement)Document4 pagesList of Mandatory Documentary Requirements and Procedure (RD Extrajudicial Settlement)punditninjaNo ratings yet

- Citigroup, Inc., v. Citistate Savings Bank, Inc.Document1 pageCitigroup, Inc., v. Citistate Savings Bank, Inc.Samantha MakayanNo ratings yet

- SPECIAL POWER OF ATTORNEY - SampleDocument3 pagesSPECIAL POWER OF ATTORNEY - SampleJustine CastanedaNo ratings yet

- Procedure in Extra-Judicial Foreclosure of Mortgage - 99-10-05-0 - August 7, 2001 - en BancDocument2 pagesProcedure in Extra-Judicial Foreclosure of Mortgage - 99-10-05-0 - August 7, 2001 - en BancKristina LayugNo ratings yet

- Republic Act No. 7279Document25 pagesRepublic Act No. 7279Sharmen Dizon GalleneroNo ratings yet

- RA 7641 retirement guidelinesDocument11 pagesRA 7641 retirement guidelinesAllan Bacaron100% (1)

- RA 7641 retirement guidelinesDocument11 pagesRA 7641 retirement guidelinesAllan Bacaron100% (1)

- RA 7641 retirement guidelinesDocument11 pagesRA 7641 retirement guidelinesAllan Bacaron100% (1)

- Boa Sworn Statement For AccreditationDocument1 pageBoa Sworn Statement For AccreditationBillcounterNo ratings yet

- Statement of MGT Responsibility ITRDocument1 pageStatement of MGT Responsibility ITRJasper Andrew AdjaraniNo ratings yet

- Contract of Sale of VesselDocument6 pagesContract of Sale of VesselNicole SantoallaNo ratings yet

- CONTRACT of LEASE Blank TemplateDocument2 pagesCONTRACT of LEASE Blank Templateronald ramosNo ratings yet

- Taxation of Non-Bank Financial Intermediaries PhilippinesDocument12 pagesTaxation of Non-Bank Financial Intermediaries Philippinesjosiah9_5No ratings yet

- Philippine Detective A) Id Protectiye Acency Inc,: Association Operators (Padpao) ' No. City IDocument1 pagePhilippine Detective A) Id Protectiye Acency Inc,: Association Operators (Padpao) ' No. City Ijoseph iii goNo ratings yet

- Financial Rehabilitation and Insolvency Act (FRIA) of 2010: Signed On July 18, 2010Document15 pagesFinancial Rehabilitation and Insolvency Act (FRIA) of 2010: Signed On July 18, 2010Maika NarcisoNo ratings yet

- Shareholders Agreement DraftDocument8 pagesShareholders Agreement DraftEnrryson SebastianNo ratings yet

- Circular Entitled RN Lax And: LocalDocument6 pagesCircular Entitled RN Lax And: Localjoseph iii goNo ratings yet

- Ra 7279Document19 pagesRa 7279Babang100% (1)

- Urban Development and Housing Act (Udha) : Notes OnDocument5 pagesUrban Development and Housing Act (Udha) : Notes OnTDNo ratings yet

- Consolidated Scale of Fines for CorporationsDocument124 pagesConsolidated Scale of Fines for CorporationsDoctorGreyNo ratings yet

- RR No. 13-98Document16 pagesRR No. 13-98Ana DocallosNo ratings yet

- Sec Reportorial RequirementsDocument2 pagesSec Reportorial RequirementsAnonymous qDb8S3koENo ratings yet

- Authority To NegotiateDocument1 pageAuthority To NegotiateJomel Arzadon BarrozoNo ratings yet

- International Corporate Bank vs. Gueco (SCRA 516)Document156 pagesInternational Corporate Bank vs. Gueco (SCRA 516)DARLENENo ratings yet

- Articles of IncorporationDocument5 pagesArticles of Incorporationpoloy6200No ratings yet

- 10 most important things about the RESA LawDocument3 pages10 most important things about the RESA LawRichard AbellaNo ratings yet

- Matching Cost Against RevenueDocument1 pageMatching Cost Against Revenuejuliet_emelinotmaestroNo ratings yet

- Application Form: Professional Regulation CommissionDocument3 pagesApplication Form: Professional Regulation Commissionmerlie_navaltaNo ratings yet

- 7925-2005-Bir Ruling No. 009-05Document4 pages7925-2005-Bir Ruling No. 009-05Alexander Julio Valera100% (1)

- Chavez Vs Gonzales 32 Scra 547Document14 pagesChavez Vs Gonzales 32 Scra 547Elyn Bautista100% (1)

- Expanded Withholding Taxes On Government Income PaymentsDocument172 pagesExpanded Withholding Taxes On Government Income PaymentsBien Bowie A. CortezNo ratings yet

- BIR Ease of Doing BusinessDocument25 pagesBIR Ease of Doing BusinessCess MelendezNo ratings yet

- Urban Planning Related LawsDocument23 pagesUrban Planning Related LawsNathalie ReyesNo ratings yet

- Group 2 Ra 7279Document48 pagesGroup 2 Ra 7279Johnny Castillo SerapionNo ratings yet

- RA 7279 9194 10884 Irr Udha Balance HousingDocument25 pagesRA 7279 9194 10884 Irr Udha Balance HousingKathleen Andrea C. RodriguezNo ratings yet

- Documents/ 563/week13.doc/ 9/29/2008/ 8:40:05 AM 1 of 13Document13 pagesDocuments/ 563/week13.doc/ 9/29/2008/ 8:40:05 AM 1 of 13VictoriaNo ratings yet

- Lecture - RA NO. 7279Document49 pagesLecture - RA NO. 7279sebkolieNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument44 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledMawmagNo ratings yet

- Cotabato City - MINISTRY OF SOCIAL SERVICES, BARMM (5.27.2020)Document2 pagesCotabato City - MINISTRY OF SOCIAL SERVICES, BARMM (5.27.2020)joseph iii goNo ratings yet

- Davao City - DEPARTMENT OF SOCIAL WELFARE AND DEVELOPMENT - REGION XI (5.27.2020)Document5 pagesDavao City - DEPARTMENT OF SOCIAL WELFARE AND DEVELOPMENT - REGION XI (5.27.2020)joseph iii goNo ratings yet

- GPPB Circular No. 02-2018 PDFDocument4 pagesGPPB Circular No. 02-2018 PDFKaren Balisacan Segundo RuizNo ratings yet

- GenSan - DEPARTMENT OF PUBLIC WORKS AND HIGHWAYS - SOUTH COTABATO 1S (5.27.2020)Document5 pagesGenSan - DEPARTMENT OF PUBLIC WORKS AND HIGHWAYS - SOUTH COTABATO 1S (5.27.2020)joseph iii goNo ratings yet

- Davao City - PRESIDENTIAL COMMISSION FOR THE URBAN POOR - REGION XI (5.27.2020)Document3 pagesDavao City - PRESIDENTIAL COMMISSION FOR THE URBAN POOR - REGION XI (5.27.2020)joseph iii goNo ratings yet

- Security Bidding Doc 2021Document56 pagesSecurity Bidding Doc 2021joseph iii goNo ratings yet

- Tagum - TAGUM WATER DISTRICT (5.27.2020)Document4 pagesTagum - TAGUM WATER DISTRICT (5.27.2020)joseph iii goNo ratings yet

- Small ClaimsDocument66 pagesSmall ClaimsarloNo ratings yet

- Omnibus Sworn StatementDocument1 pageOmnibus Sworn StatementjovanNo ratings yet

- Affidavit of Undertaking: Annex "A"Document1 pageAffidavit of Undertaking: Annex "A"joseph iii goNo ratings yet

- Book 1Document10 pagesBook 1Bianca Camille Bodoy SalvadorNo ratings yet

- FULL TEXT: EO No. 28, Extending The Enhanced Community Quarantine in Davao CityDocument2 pagesFULL TEXT: EO No. 28, Extending The Enhanced Community Quarantine in Davao Cityjoseph iii goNo ratings yet

- DTI-DOLE Joint Memorandum Circular No. 20-04-ADocument22 pagesDTI-DOLE Joint Memorandum Circular No. 20-04-AdonhillourdesNo ratings yet

- EO292 - Admin Code Book IIDocument9 pagesEO292 - Admin Code Book IIjoseph iii goNo ratings yet

- Executive Order No. 292 Administrative Code of 1987Document8 pagesExecutive Order No. 292 Administrative Code of 1987joseph iii goNo ratings yet

- Post-Employment Termination and Retirement RulesDocument4 pagesPost-Employment Termination and Retirement RulesWilfredo MolinaNo ratings yet

- Manual On The Disposition of SL CaseDocument47 pagesManual On The Disposition of SL CaseAnonymous zJ0X97No ratings yet

- Codal - BP 881 Omnibus Election CodeDocument95 pagesCodal - BP 881 Omnibus Election CodeCamille Hernandez0% (1)

- RA 8295 Proclamation of Lone CandidateDocument2 pagesRA 8295 Proclamation of Lone Candidatejoseph iii goNo ratings yet

- Dole Do 18-02 2002Document7 pagesDole Do 18-02 2002thecityforeverNo ratings yet

- Comelec Rules of ProcedureDocument45 pagesComelec Rules of ProceduremakicanibanNo ratings yet

- Revised Rules Proceedings Regional ArbitersDocument18 pagesRevised Rules Proceedings Regional ArbitersDianne MedianeroNo ratings yet

- Hadhrat Moulana Maseehullah - RADocument319 pagesHadhrat Moulana Maseehullah - RAtakwania100% (1)

- Certificate of EarningsDocument1 pageCertificate of EarningsRiasat AliNo ratings yet

- Assignment 2 Answer KeyDocument2 pagesAssignment 2 Answer KeyAbdulakbar Ganzon BrigoleNo ratings yet

- Soal Siklus AkuntansiDocument6 pagesSoal Siklus Akuntansidery dulitaNo ratings yet

- 74HC00D 74HC00D 74HC00D 74HC00D: CMOS Digital Integrated Circuits Silicon MonolithicDocument8 pages74HC00D 74HC00D 74HC00D 74HC00D: CMOS Digital Integrated Circuits Silicon MonolithicAssistec TecNo ratings yet

- Wong Keng Liang The Lizard King CaseDocument11 pagesWong Keng Liang The Lizard King CaseaishahNo ratings yet

- (LLM. Crim.L) Comperative LawDocument11 pages(LLM. Crim.L) Comperative LawAishwarya SudhirNo ratings yet

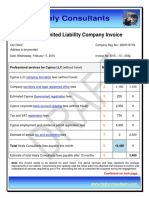

- Draft Invoice Cyprus LLC MigrationDocument7 pagesDraft Invoice Cyprus LLC MigrationShehryar KhanNo ratings yet

- MCB Bank Internship ReportDocument9 pagesMCB Bank Internship ReportZahid ButtNo ratings yet

- SB 737 53 1125 03Document39 pagesSB 737 53 1125 03Fernando CarmonaNo ratings yet

- Roxanna Mayo LawsuitDocument20 pagesRoxanna Mayo LawsuitNaomi MartinNo ratings yet

- Case Analysis of X V Principal SecretaryDocument6 pagesCase Analysis of X V Principal SecretaryVimdhayak JiNo ratings yet

- D. The Learning Child v. Ayala Alabang Village Association (Non-Impairment Clause)Document18 pagesD. The Learning Child v. Ayala Alabang Village Association (Non-Impairment Clause)Kaloi GarciaNo ratings yet

- Correctional Administration: (Institutional Correction)Document15 pagesCorrectional Administration: (Institutional Correction)RamirezNo ratings yet

- Ethnicity and Crime A3 Knowledge Organiser FinalDocument3 pagesEthnicity and Crime A3 Knowledge Organiser FinalCharlotte BrennanNo ratings yet

- GARVICH, Javier. El Caracter Chicha en La Cultura Peruana ContemporaneaDocument10 pagesGARVICH, Javier. El Caracter Chicha en La Cultura Peruana ContemporaneaDarloxNo ratings yet

- 4 - Is Democracy A FailureDocument8 pages4 - Is Democracy A FailureSaqib Shuhab SNo ratings yet

- Telkom 4 at 108.0°E - LyngSatDocument5 pagesTelkom 4 at 108.0°E - LyngSatEchoz NhackalsNo ratings yet

- Quiz Securities LawDocument7 pagesQuiz Securities LawSevastian jedd EdicNo ratings yet

- Central Board of Direct Taxes, E-Filing Project: ITR 1 - Validation Rules For AY 2021-22Document15 pagesCentral Board of Direct Taxes, E-Filing Project: ITR 1 - Validation Rules For AY 2021-22MOHAMMED LayeeqNo ratings yet

- Fauquier Supervisors May 14, 2020, AgendaDocument3 pagesFauquier Supervisors May 14, 2020, AgendaFauquier NowNo ratings yet

- RRiF br. 1/13 fiscalization elements and leasing accountingDocument1 pageRRiF br. 1/13 fiscalization elements and leasing accountingivmar61No ratings yet

- 404 Damodhar Narayan Sawale V Shri Tejrao Bajirao Mhaske 4 May 2023 472234Document13 pages404 Damodhar Narayan Sawale V Shri Tejrao Bajirao Mhaske 4 May 2023 472234Avinash SrivastavaNo ratings yet

- Canoreco v. Torres GR 127249 2-27-1998Document10 pagesCanoreco v. Torres GR 127249 2-27-1998HjktdmhmNo ratings yet

- Ventureshield™ Paint Protection Film 7510Cc/Cs-Ld: Technical Data Sheet April 2011Document2 pagesVentureshield™ Paint Protection Film 7510Cc/Cs-Ld: Technical Data Sheet April 2011Димитър ПетровNo ratings yet