You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Admin Rough DraftDocument3 pagesAdmin Rough DraftMonica ChandrashekharNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Corporate Law II Final DraftDocument15 pagesCorporate Law II Final DraftMonica ChandrashekharNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Taxation Law Final DraftDocument16 pagesTaxation Law Final DraftMonica ChandrashekharNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Banking Law Final DraftDocument20 pagesBanking Law Final DraftMonica ChandrashekharNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Taxation Law Rough DraftDocument3 pagesTaxation Law Rough DraftMonica ChandrashekharNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- DPC Final DraftDocument28 pagesDPC Final DraftMonica ChandrashekharNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Admin Rough DraftDocument3 pagesAdmin Rough DraftMonica ChandrashekharNo ratings yet

- Taxation Law II Final DraftDocument12 pagesTaxation Law II Final DraftMonica ChandrashekharNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- IPR Final DraftDocument17 pagesIPR Final DraftMonica ChandrashekharNo ratings yet

- IC Report - DraftDocument31 pagesIC Report - DraftMonica ChandrashekharNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Compendium of Case LawsDocument6 pagesCompendium of Case LawsMonica ChandrashekharNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Godrej Agrovet LTD Vs Ramdev Singh & Ors On 14 December, 2013Document2 pagesGodrej Agrovet LTD Vs Ramdev Singh & Ors On 14 December, 2013Monica ChandrashekharNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Farokh SDocument1 pageFarokh SMonica ChandrashekharNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Sri Jayanta Goswami Vs The Senior Post Master, Serampore ... On 8 May, 2019Document6 pagesSri Jayanta Goswami Vs The Senior Post Master, Serampore ... On 8 May, 2019Monica ChandrashekharNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Tarun Kumar Ghai Vs Malibu Estate Pvt. Ltd. and Ors. On 20 December, 2007Document8 pagesTarun Kumar Ghai Vs Malibu Estate Pvt. Ltd. and Ors. On 20 December, 2007Monica ChandrashekharNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Mr. Narinder Arora Vs Altus Space Builders Private ... On 25 March, 2019Document18 pagesMr. Narinder Arora Vs Altus Space Builders Private ... On 25 March, 2019Monica ChandrashekharNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- CaseDocument5 pagesCaseMonica ChandrashekharNo ratings yet

- Hafizuddin Adult Son of Sri ... Vs Additional District Judge (Court ... On 15 December, 2005Document15 pagesHafizuddin Adult Son of Sri ... Vs Additional District Judge (Court ... On 15 December, 2005Monica ChandrashekharNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Atma Krishna Vs Orris Infrastructure Ltd. & Anr. On 21 December, 2018Document9 pagesAtma Krishna Vs Orris Infrastructure Ltd. & Anr. On 21 December, 2018Monica ChandrashekharNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- M S. Fortune Infrastructure (Now ... Vs Trevor Dlima On 12 March, 2018Document8 pagesM S. Fortune Infrastructure (Now ... Vs Trevor Dlima On 12 March, 2018Monica ChandrashekharNo ratings yet

- M S. SHL Ventures Vs P. Venkata Satya Prasad Rao On 20 August, 2018Document3 pagesM S. SHL Ventures Vs P. Venkata Satya Prasad Rao On 20 August, 2018Monica ChandrashekharNo ratings yet

- Delhi Transport Corporation Vs D.T.C. Mazdoor Congress On 4 September, 1990Document133 pagesDelhi Transport Corporation Vs D.T.C. Mazdoor Congress On 4 September, 1990Monica ChandrashekharNo ratings yet

- Anwari Basawaraj Patil and Ors Vs Siddaramaiah and Ors On 27 January, 1993 PDFDocument7 pagesAnwari Basawaraj Patil and Ors Vs Siddaramaiah and Ors On 27 January, 1993 PDFMonica ChandrashekharNo ratings yet

- Alka Bose Vs Parmatma Devi & Ors On 17 December, 2008Document6 pagesAlka Bose Vs Parmatma Devi & Ors On 17 December, 2008Monica ChandrashekharNo ratings yet

- Managerial Economics Final DraftDocument25 pagesManagerial Economics Final DraftMonica ChandrashekharNo ratings yet

- Ambadi Enterprises Limited, Vs Tmt. Rajalakshmi Subramanian On 26 February, 2013Document6 pagesAmbadi Enterprises Limited, Vs Tmt. Rajalakshmi Subramanian On 26 February, 2013Monica ChandrashekharNo ratings yet

- A. J. Ramadoss Vs S. Padmavathy and On 9 April, 2013Document7 pagesA. J. Ramadoss Vs S. Padmavathy and On 9 April, 2013Monica ChandrashekharNo ratings yet

- Evidence Law Final DraftDocument36 pagesEvidence Law Final DraftMonica ChandrashekharNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Affidavit of Duress: Illegal Tax Enforcement by de Facto Officers, Form #02.005Document48 pagesAffidavit of Duress: Illegal Tax Enforcement by de Facto Officers, Form #02.005Sovereignty Education and Defense Ministry (SEDM)No ratings yet

- Checklist Issuance New License LBDocument3 pagesChecklist Issuance New License LBRodneyAceNo ratings yet

- CIR Vs Filinvest (Case Digest)Document3 pagesCIR Vs Filinvest (Case Digest)Togz Mape100% (1)

- CommissionBill 3Document1 pageCommissionBill 3sarbjeet kumarNo ratings yet

- KushalDocument1 pageKushalKushal SinghalNo ratings yet

- Accounting For Partnerships: ©Mcgraw-Hill Companies, Inc., 2005 Solutions Manual, Chapter 12 653Document42 pagesAccounting For Partnerships: ©Mcgraw-Hill Companies, Inc., 2005 Solutions Manual, Chapter 12 653Ch Radeel MurtazaNo ratings yet

- TAXATION. Good NotesDocument33 pagesTAXATION. Good NotesDavid100% (2)

- Hilton MA 12e Chap002Document53 pagesHilton MA 12e Chap002Vân HảiNo ratings yet

- 2012 Instructions For Schedule C: Profit or Loss From BusinessDocument13 pages2012 Instructions For Schedule C: Profit or Loss From BusinessDunk7No ratings yet

- The Business, Tax, and Financial EnvironmentsDocument38 pagesThe Business, Tax, and Financial EnvironmentsNaveed AhmadNo ratings yet

- 1-33504247894 G0057436708 PDFDocument3 pages1-33504247894 G0057436708 PDFAziz MalikNo ratings yet

- 200 SAP SD Interview Questions and AnswersDocument16 pages200 SAP SD Interview Questions and Answersestivali10No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Ty Baf Sem Vi All Sample Question PaperDocument35 pagesTy Baf Sem Vi All Sample Question Paperjainam shahNo ratings yet

- A. General Concepts and Principles of TaxationDocument4 pagesA. General Concepts and Principles of TaxationAngelica EsguireroNo ratings yet

- RR No. 26-2002 Staggered FilingDocument5 pagesRR No. 26-2002 Staggered FilingCkey ArNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Ch PrasadNo ratings yet

- HighNote5 Unit Skills Test Unit03 GroupADocument3 pagesHighNote5 Unit Skills Test Unit03 GroupAMaria Berenice PantinNo ratings yet

- Edu Ex .: Crack It in First Attempt!!!Document3 pagesEdu Ex .: Crack It in First Attempt!!!umang24No ratings yet

- MGT-111 Final Term V.impDocument59 pagesMGT-111 Final Term V.impshahbaz shahidNo ratings yet

- In Re ZialcitaDocument6 pagesIn Re ZialcitaJunnieson BonielNo ratings yet

- P.D 1612-Anti Fencing LawDocument12 pagesP.D 1612-Anti Fencing LawRoemelNo ratings yet

- FOP and Inventory ControlDocument29 pagesFOP and Inventory ControlNefvi Desqi AndrianiNo ratings yet

- Ebook Corporate Finance PDF Full Chapter PDFDocument67 pagesEbook Corporate Finance PDF Full Chapter PDFmyrtle.sampson431100% (25)

- GL Owners - JTDocument50 pagesGL Owners - JTSuneet GaggarNo ratings yet

- HLB Personal Loan TNC en BMDocument25 pagesHLB Personal Loan TNC en BMMbatu TchalaNo ratings yet

- The Country Notebook-A Guide For Developing A Marketing PlanDocument40 pagesThe Country Notebook-A Guide For Developing A Marketing PlanMohammad BasahiNo ratings yet

- 08 Activity 1Document2 pages08 Activity 1Cj MoontonNo ratings yet

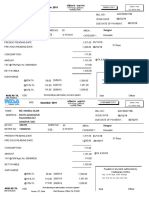

- Payroll Summary For The Month of AugustDocument46 pagesPayroll Summary For The Month of AugustAida MohammedNo ratings yet

- Rakib Wasa BillDocument1 pageRakib Wasa BillShahrial AhmedNo ratings yet

- Time: 3 Hrs Economics Marks: 80: Group A' Group B'Document13 pagesTime: 3 Hrs Economics Marks: 80: Group A' Group B'psawant77No ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet