You might also like

- Ciimem2 2nd Luciani enDocument15 pagesCiimem2 2nd Luciani enpahammed.farzeenNo ratings yet

- 11 - Michele Nardella. Market Concentration and Vertical IntegrationDocument27 pages11 - Michele Nardella. Market Concentration and Vertical IntegrationRicardo Vera TorresNo ratings yet

- 3Document1 page3Gissa SevieNo ratings yet

- Disbursing Cash To Shareholders: Frequently Asked Questions About Buybacks and DividendsDocument21 pagesDisbursing Cash To Shareholders: Frequently Asked Questions About Buybacks and DividendsDQNo ratings yet

- Uogb HPCL PDFDocument146 pagesUogb HPCL PDFSwagato ChakrabortyNo ratings yet

- Global Progress Polio Eradication Program & IPVDocument47 pagesGlobal Progress Polio Eradication Program & IPVASEP PRIATNANo ratings yet

- Malaysia'S Cocoa Industry: Progress and DevelopmentDocument29 pagesMalaysia'S Cocoa Industry: Progress and DevelopmentaseancocoaclubNo ratings yet

- Figure 1. Energy Production Figure 2. Total Primary Energy SupplyDocument3 pagesFigure 1. Energy Production Figure 2. Total Primary Energy Supplyalexey91400No ratings yet

- INM-CSA PracticeDocument40 pagesINM-CSA PracticeCharradi FatihaNo ratings yet

- Strip Plan For Utility Shifting and Tree Cutting (Km.139/Nh-15)Document1 pageStrip Plan For Utility Shifting and Tree Cutting (Km.139/Nh-15)Bilal A BarbhuiyaNo ratings yet

- T C M E R U S: HE Olombian Onetary AND Xchange Egime Nder TressDocument13 pagesT C M E R U S: HE Olombian Onetary AND Xchange Egime Nder Tressapi-26091012No ratings yet

- Cable Tray Catalogue 2021Document6 pagesCable Tray Catalogue 2021Project1 Tech7No ratings yet

- 16 Mines in 2010Document53 pages16 Mines in 2010api-16218084No ratings yet

- GRAPHDocument1 pageGRAPHShanelle MacajilosNo ratings yet

- GRAPHDocument1 pageGRAPHShanelle MacajilosNo ratings yet

- Imamia Book Bank: A Project of Imamia Education Board (IEB) Jaffar-E-Tayyar UnitDocument9 pagesImamia Book Bank: A Project of Imamia Education Board (IEB) Jaffar-E-Tayyar Unitale hassanNo ratings yet

- Book 1Document2 pagesBook 1pacoyabi4454No ratings yet

- Worldwide ICT Spending by Technology FactorDocument1 pageWorldwide ICT Spending by Technology FactorRodr-No ratings yet

- Pump Hm250 FHC-S C5 Performance Curve: 600mm 600mm Full Closed 73mm High Chrome High ChromeDocument1 pagePump Hm250 FHC-S C5 Performance Curve: 600mm 600mm Full Closed 73mm High Chrome High ChromeJoão Paulo Augusto MacedoNo ratings yet

- No. Students Registered No. of Students Recruited: Yearwise Placement StatisticsDocument9 pagesNo. Students Registered No. of Students Recruited: Yearwise Placement StatisticsrtrNo ratings yet

- Waterfall Chart TemplateDocument3 pagesWaterfall Chart TemplateMichael GarciaNo ratings yet

- Latihan ComputerDocument2 pagesLatihan ComputerdewiNo ratings yet

- Iron Pump QVDocument2 pagesIron Pump QVAmit ChourasiaNo ratings yet

- Trabajo 6 Geologia CorteDocument1 pageTrabajo 6 Geologia Cortejtrinacokhotmail.comNo ratings yet

- Excel Ex4Document6 pagesExcel Ex4Moza AlmaamariNo ratings yet

- Crude Palm Oil Hedging and StorageDocument5 pagesCrude Palm Oil Hedging and StorageRaymond Thurston DavidNo ratings yet

- Typ. Roof Beam DetailDocument1 pageTyp. Roof Beam DetailJuliah Ekisha MeiNo ratings yet

- PrinEconArabWorld 4e Ch02 PowerPointDocument20 pagesPrinEconArabWorld 4e Ch02 PowerPointmaha13aljasmiNo ratings yet

- 0680 - w07 - 2 Question Paper WT Answer2007Document20 pages0680 - w07 - 2 Question Paper WT Answer2007same faazNo ratings yet

- BS 6779 - Highways Parapets For Bridges... Part 4Document56 pagesBS 6779 - Highways Parapets For Bridges... Part 4Vicky Munien100% (3)

- Issued For Information Issued For Approval: NotesDocument1 pageIssued For Information Issued For Approval: NotesAnkurAgarwalNo ratings yet

- Treinamento - Evolução - 2022 - GabrielDocument98 pagesTreinamento - Evolução - 2022 - GabrielGabriel MartinsNo ratings yet

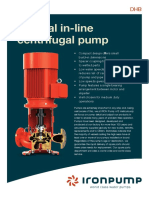

- IP Pump DataSheet DHBDocument2 pagesIP Pump DataSheet DHBAmit ChourasiaNo ratings yet

- Year 5 Mass AssessmentDocument7 pagesYear 5 Mass AssessmentSomala KarthigeshNo ratings yet

- Sustainability 12 08142 v2Document12 pagesSustainability 12 08142 v2Bahiru BelachewNo ratings yet

- Bonding Jumper-Cable Tray)Document2 pagesBonding Jumper-Cable Tray)nadeem UddinNo ratings yet

- Bull & Bear Market CorrectionsDocument10 pagesBull & Bear Market Correctionsk bierNo ratings yet

- Pareto ChartDocument2 pagesPareto ChartshikhaNo ratings yet

- IP Pump DataSheet CNLDocument2 pagesIP Pump DataSheet CNLAmit ChourasiaNo ratings yet

- Seminar Teknik Untirta 2010Document23 pagesSeminar Teknik Untirta 2010Wawan GunawanNo ratings yet

- Belt and Bucket Elevator - LBEB - Data Sheet - ENDocument2 pagesBelt and Bucket Elevator - LBEB - Data Sheet - ENsalih khattabNo ratings yet

- Upendra Singh: Technology Advances in Agricultural Production, Water and Nutrient ManagementDocument55 pagesUpendra Singh: Technology Advances in Agricultural Production, Water and Nutrient ManagementCharradi FatihaNo ratings yet

- Macro-Economic Case of The PhilippinesDocument21 pagesMacro-Economic Case of The PhilippinesMichaelAngeloBattungNo ratings yet

- Recent Advances in Sorghum Improvement Research at ICRISAT: Review ArticleDocument8 pagesRecent Advances in Sorghum Improvement Research at ICRISAT: Review ArticleKateNo ratings yet

- Aviation Industry in India: Submitted To: Dr. Jagdish Shettigar Dr. Pooja MishraDocument33 pagesAviation Industry in India: Submitted To: Dr. Jagdish Shettigar Dr. Pooja Mishrasy dayNo ratings yet

- Admission Open For Session 2021-2022: 10% Discount On All The BooksDocument2 pagesAdmission Open For Session 2021-2022: 10% Discount On All The BooksJaanvhi BhatraiNo ratings yet

- Viability of Coffee Farming As A Business: Lucy MuriithiDocument11 pagesViability of Coffee Farming As A Business: Lucy MuriithiTrey NgugiNo ratings yet

- Significant Organizational Achievements and Commitments 1992-2022Document8 pagesSignificant Organizational Achievements and Commitments 1992-2022FIRST CHILDREN'S EMBASSY IN THE WORLD MEGJASHI MACEDONIANo ratings yet

- MB 17 Redmond 0419Document4 pagesMB 17 Redmond 0419TBP_Think_TankNo ratings yet

- Revised Low Cost 11 New District - Structural Semi Detached FNDDocument1 pageRevised Low Cost 11 New District - Structural Semi Detached FNDElirehema MunuoNo ratings yet

- Introduction of SCP To The Curriculum - FoM - UoCDocument77 pagesIntroduction of SCP To The Curriculum - FoM - UoCThusitha SugathapalaNo ratings yet

- Global Markets MinesweeperDocument4 pagesGlobal Markets MinesweeperanisdangasNo ratings yet

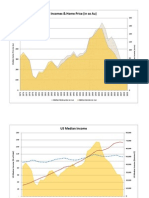

- Incomes & Home Price (In Oz Au)Document2 pagesIncomes & Home Price (In Oz Au)kettle1No ratings yet

- Indoneisa 2013Document36 pagesIndoneisa 2013Iam IbadNo ratings yet

- IS1948Document2 pagesIS1948fabian pachecoNo ratings yet

- Final Portfolio For Print 2 FULLDocument29 pagesFinal Portfolio For Print 2 FULLJim NohNo ratings yet

- Hugh Donovan, Eight-Year Review of The Full Depth Reclamation Process in The City of EdmontonDocument40 pagesHugh Donovan, Eight-Year Review of The Full Depth Reclamation Process in The City of Edmontoneye2iNo ratings yet

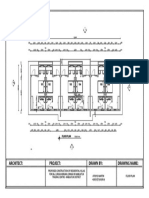

- Architect: Project: Drawn By: Drawing Name:: Floor PlanDocument1 pageArchitect: Project: Drawn By: Drawing Name:: Floor PlanAthiyo MartinNo ratings yet

- Type 1279, 1377, 1379 & 2462 Receiver GaugesDocument4 pagesType 1279, 1377, 1379 & 2462 Receiver GaugesHectorNo ratings yet

- Session 4.2: ASEAN in The Global Value Chains by Aladdin RilloDocument16 pagesSession 4.2: ASEAN in The Global Value Chains by Aladdin RilloADBI EventsNo ratings yet

- Session 4.1: Leveraging On The New Economy For Inclusive Growth: Factory Asia, Shopper Asia by Lam San LingDocument43 pagesSession 4.1: Leveraging On The New Economy For Inclusive Growth: Factory Asia, Shopper Asia by Lam San LingADBI EventsNo ratings yet

- Session 1.3: The Housing Unaffordability Crisis in Asia & Pacific by Matthias HelbleDocument24 pagesSession 1.3: The Housing Unaffordability Crisis in Asia & Pacific by Matthias HelbleADBI EventsNo ratings yet

- Session 2.1: Thailand and Malaysia's Incentive and Regulatory Design For SOE Performance by Pornchai WisuttisakDocument52 pagesSession 2.1: Thailand and Malaysia's Incentive and Regulatory Design For SOE Performance by Pornchai WisuttisakADBI EventsNo ratings yet

- Session 2.2: Establishing Social Protection System For Inclusive Rural Development by Arup ChatterjeeDocument45 pagesSession 2.2: Establishing Social Protection System For Inclusive Rural Development by Arup ChatterjeeADBI EventsNo ratings yet

- Heat TreatmentDocument14 pagesHeat TreatmentAkhilesh KumarNo ratings yet

- AAR Safety Fact SheetDocument2 pagesAAR Safety Fact Sheetrogelio mezaNo ratings yet

- The Impact of Teaching PracticeDocument14 pagesThe Impact of Teaching PracticemubarakNo ratings yet

- Plastics Library 2016 enDocument32 pagesPlastics Library 2016 enjoantanamal tanamaNo ratings yet

- UX-driven Heuristics For Every Designer: OutlineDocument7 pagesUX-driven Heuristics For Every Designer: OutlinemuhammadsabirinhadisNo ratings yet

- 1778 3557 1 SM PDFDocument4 pages1778 3557 1 SM PDFjulio simanjuntakNo ratings yet

- Science 10 FINAL Review 2014Document49 pagesScience 10 FINAL Review 2014Zara Zalaal [Student]No ratings yet

- Etm API 600 Trim MaterialDocument1 pageEtm API 600 Trim Materialmayukhguhanita2010No ratings yet

- ToobaKhawar 6733 VPL Lab Sat 12 3 All TasksDocument38 pagesToobaKhawar 6733 VPL Lab Sat 12 3 All TasksTooba KhawarNo ratings yet

- Writing Capstone Research Project For Senior High School A Modified Guide ManualDocument9 pagesWriting Capstone Research Project For Senior High School A Modified Guide ManualIOER International Multidisciplinary Research Journal ( IIMRJ)No ratings yet

- Orchid Group of Companies Company ProfileDocument3 pagesOrchid Group of Companies Company ProfileAngelica Nicole TamayoNo ratings yet

- Standard CellDocument53 pagesStandard CellShwethNo ratings yet

- Sow and Learning ObjectivesDocument14 pagesSow and Learning ObjectivesEhsan AzmanNo ratings yet

- Unit-4.Vector CalculusDocument32 pagesUnit-4.Vector Calculuskhatua.deb87No ratings yet

- Creating Enterprise LeadersDocument148 pagesCreating Enterprise LeadersValuAidNo ratings yet

- Autonomic Nervous SystemDocument21 pagesAutonomic Nervous SystemDung Nguyễn Thị MỹNo ratings yet

- Hitachi VSP Pricelist PeppmDocument57 pagesHitachi VSP Pricelist PeppmBahman MirNo ratings yet

- Mrr2 Why The Future Doesnt Need UsDocument3 pagesMrr2 Why The Future Doesnt Need UsSunshine Glory EgoniaNo ratings yet

- Terraform AWSDocument1,531 pagesTerraform AWSTilted Mowa100% (1)

- The History of The Photocopy MachineDocument2 pagesThe History of The Photocopy MachineAndy WijayaNo ratings yet

- Ssg-Ng01012401-Gen-Aa-5880-00012 - C01 - Ssags Nigerian Content PlanDocument24 pagesSsg-Ng01012401-Gen-Aa-5880-00012 - C01 - Ssags Nigerian Content PlanStroom Limited100% (2)

- 44Document2 pages44menakadevieceNo ratings yet

- Tawjihi 7Document55 pagesTawjihi 7api-3806314No ratings yet

- 3 - RA-Erecting and Dismantling of Scaffolds (WAH) (Recovered)Document6 pages3 - RA-Erecting and Dismantling of Scaffolds (WAH) (Recovered)hsem Al EimaraNo ratings yet

- Banana Stem Patty Pre Finale 1Document16 pagesBanana Stem Patty Pre Finale 1Armel Barayuga86% (7)

- Authority To TravelDocument39 pagesAuthority To TraveljoraldNo ratings yet

- Microtech Testing & Research Laboratory: Condition of Sample, When Received: SatisfactoryDocument1 pageMicrotech Testing & Research Laboratory: Condition of Sample, When Received: SatisfactoryKumar AbhishekNo ratings yet

- Buncefield Volume 2Document208 pagesBuncefield Volume 2Hammy223No ratings yet

- Tle7 Ict TD M2 V3Document28 pagesTle7 Ict TD M2 V3Rowemar Corpuz100% (1)

- Building A Vacuum Forming TableDocument9 pagesBuilding A Vacuum Forming TableWil NelsonNo ratings yet