You might also like

- "Common Documents": Document No 7,8 and 11 Are OptionalDocument2 pages"Common Documents": Document No 7,8 and 11 Are OptionalMayurRawoolNo ratings yet

- Template: (See Master Slides)Document13 pagesTemplate: (See Master Slides)MayurRawoolNo ratings yet

- IPR Project OriginalDocument22 pagesIPR Project OriginalMayurRawoolNo ratings yet

- Form No. 9: Record of Mortgage by Deposit of Title - DeedsDocument1 pageForm No. 9: Record of Mortgage by Deposit of Title - DeedsMayurRawoolNo ratings yet

- Maharashtra Act No. XXIV of 1961Document154 pagesMaharashtra Act No. XXIV of 1961MayurRawoolNo ratings yet

- Template: (See Master Slides)Document13 pagesTemplate: (See Master Slides)MayurRawoolNo ratings yet

- Mobile A Boon or CURSEDocument6 pagesMobile A Boon or CURSEMayurRawoolNo ratings yet

- Call CenterDocument13 pagesCall CenterMayurRawoolNo ratings yet

- Moot Court 1Document21 pagesMoot Court 1MayurRawoolNo ratings yet

- Lecture 17 - Game TheoryDocument28 pagesLecture 17 - Game TheoryMayurRawoolNo ratings yet

- ProductionDocument35 pagesProductionMayurRawoolNo ratings yet

- Working Capital ManagementDocument50 pagesWorking Capital ManagementUpendra SinghNo ratings yet

- Fire InsuranceDocument18 pagesFire InsuranceMayurRawoolNo ratings yet

- GK Compilation of Important Topics For SnapDocument4 pagesGK Compilation of Important Topics For SnapMayurRawoolNo ratings yet

- Accounting Treatment of Goodwill at The Time of AdmissionDocument25 pagesAccounting Treatment of Goodwill at The Time of AdmissionMayurRawool100% (2)

- Name: Shraddha C Surve Te CMPN B Batch No:4 Roll No:59 Expt No:1 AIM: To Study OPEN-ENDEN SystemDocument4 pagesName: Shraddha C Surve Te CMPN B Batch No:4 Roll No:59 Expt No:1 AIM: To Study OPEN-ENDEN SystemMayurRawoolNo ratings yet

- Earn Profits: "Goodwill Is Nothing More Than The Probability That The Old Customer Will Resort To The Old Place."Document4 pagesEarn Profits: "Goodwill Is Nothing More Than The Probability That The Old Customer Will Resort To The Old Place."MayurRawoolNo ratings yet

- Horror, Love and Break Up StoriesDocument1 pageHorror, Love and Break Up StoriesMayurRawoolNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (347)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

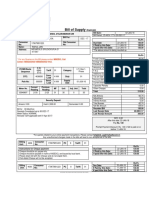

- Bill of Supply: For Any Queries On This Bill Please Contact MSEDCL CallDocument1 pageBill of Supply: For Any Queries On This Bill Please Contact MSEDCL CallrahulNo ratings yet

- Cost Curves: QuantityDocument1 pageCost Curves: QuantityAmmar Akhter Uz ZamanNo ratings yet

- Ghana Culture Global CitizenshipDocument17 pagesGhana Culture Global Citizenshipapi-687506772No ratings yet

- RENAULT Lodgy BrochureDocument8 pagesRENAULT Lodgy Brochureman_ishkumarNo ratings yet

- Power IndustryDocument11 pagesPower IndustryMinesh Chand MeenaNo ratings yet

- Toyota Remote InstructionsDocument64 pagesToyota Remote InstructionsRonit LambaNo ratings yet

- MIM CSR Final Paper (Riquet and Jarck)Document20 pagesMIM CSR Final Paper (Riquet and Jarck)lriquetNo ratings yet

- Ho3 BLT 2019Document13 pagesHo3 BLT 2019Angeline VergaraNo ratings yet

- Trade Union Congress in The PhilippinesDocument15 pagesTrade Union Congress in The PhilippinesHerbie SolonNo ratings yet

- Chapter-1 Imperatives For Market Driven StrategyDocument11 pagesChapter-1 Imperatives For Market Driven Strategysajid bhattiNo ratings yet

- Decent Work in Global Supply Chains: A Baseline ReportDocument22 pagesDecent Work in Global Supply Chains: A Baseline ReportDaniela FrumusachiNo ratings yet

- Your Boarding Pass To Mumbai - VISTARADocument1 pageYour Boarding Pass To Mumbai - VISTARAJinkal patwariNo ratings yet

- The Fārs Hoard: A Buyid Hoard From Fārs Province, Iran / Donald S. WhitcombDocument97 pagesThe Fārs Hoard: A Buyid Hoard From Fārs Province, Iran / Donald S. WhitcombDigital Library Numis (DLN)No ratings yet

- 05 Bbma3203 T1Document23 pages05 Bbma3203 T1Harianti HattaNo ratings yet

- Audited Financial StatementDocument17 pagesAudited Financial StatementVictor BiacoloNo ratings yet

- Ramadan Rate Offer Far-East 2023Document1 pageRamadan Rate Offer Far-East 2023Ryan DarmawanNo ratings yet

- Account Statement 24th March 2016Document3 pagesAccount Statement 24th March 2016Niket GuptaNo ratings yet

- The Role of Supply Chain Management in EconomyDocument24 pagesThe Role of Supply Chain Management in EconomySHIVANSHUNo ratings yet

- Mission Statement Says:: Harley Davidson, IncDocument13 pagesMission Statement Says:: Harley Davidson, IncKaran ChaudharyNo ratings yet

- Let S Fall in LoveDocument6 pagesLet S Fall in LoveDantiNo ratings yet

- Sorp 4Document13 pagesSorp 4flippermiloNo ratings yet

- Case Study On Amazon Supply Chain MetricDocument34 pagesCase Study On Amazon Supply Chain MetricAyush goyal100% (1)

- Geochemical Methods in Mineral ExplorationDocument22 pagesGeochemical Methods in Mineral ExplorationSandeep GawandeNo ratings yet

- Term Report-Analysis of Sugar Industry of Pakistan PDFDocument13 pagesTerm Report-Analysis of Sugar Industry of Pakistan PDFAryanMemonNo ratings yet

- CONTRACT To Sell Ponciano BatugalDocument3 pagesCONTRACT To Sell Ponciano BatugalEppie SeverinoNo ratings yet

- FinTech in IndiaDocument6 pagesFinTech in IndiaMARPU RAVITEJANo ratings yet

- Jammu and Kashmir Bank Clerk Prelims Model Paper 2: English LanguageDocument26 pagesJammu and Kashmir Bank Clerk Prelims Model Paper 2: English LanguageShubham VermaNo ratings yet

- Asis Mo 6: Supply Chain ManagementDocument8 pagesAsis Mo 6: Supply Chain ManagementTalitha GranitaNo ratings yet

- QuestionnaireDocument2 pagesQuestionnaireRM FerrancolNo ratings yet

- The Civilization of China and IndiaDocument3 pagesThe Civilization of China and IndiaTomNo ratings yet