You might also like

- Project MNGGDocument48 pagesProject MNGGJaspreet SalujaNo ratings yet

- General Management - DIGITAL PAYMENT REVOLUTION PDFDocument40 pagesGeneral Management - DIGITAL PAYMENT REVOLUTION PDFasitbhatiaNo ratings yet

- Data Analysis of CBDocument8 pagesData Analysis of CBasitbhatiaNo ratings yet

- 07 PDFDocument1 page07 PDFasitbhatiaNo ratings yet

- Subject: Closure of Savings/ Current Bank Account (Whichever Is Applicable)Document1 pageSubject: Closure of Savings/ Current Bank Account (Whichever Is Applicable)asitbhatiaNo ratings yet

- Siddhesh Moitra - MMS 2018-2020 - Roll No.44Document1 pageSiddhesh Moitra - MMS 2018-2020 - Roll No.44asitbhatiaNo ratings yet

- Questionnaire Investors Perception Towards RiskDocument2 pagesQuestionnaire Investors Perception Towards RiskasitbhatiaNo ratings yet

- Competitionact2012 PDFDocument65 pagesCompetitionact2012 PDFpriyankasunjayNo ratings yet

- Real Estate Consumer Behavior ReportDocument74 pagesReal Estate Consumer Behavior ReportasitbhatiaNo ratings yet

- The Impact of Social Entrepreneurship On Wealth Creation in Nigeria A Case Study of Selected Non-For-Profit Organizations (NPOS)Document24 pagesThe Impact of Social Entrepreneurship On Wealth Creation in Nigeria A Case Study of Selected Non-For-Profit Organizations (NPOS)asitbhatiaNo ratings yet

- 17 - Infosys Limited - Hetvi DoshiDocument14 pages17 - Infosys Limited - Hetvi DoshiasitbhatiaNo ratings yet

- LinkedIn Training Program - MMSA2018-20Document11 pagesLinkedIn Training Program - MMSA2018-20asitbhatiaNo ratings yet

- Historic Returns - Ultra Short Duration Fund Performance Tracker Mutual Funds With Highest ReturnsDocument3 pagesHistoric Returns - Ultra Short Duration Fund Performance Tracker Mutual Funds With Highest ReturnsasitbhatiaNo ratings yet

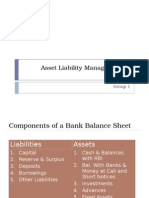

- Asset Liability Management in Banks: Group 1Document29 pagesAsset Liability Management in Banks: Group 1AjDonNo ratings yet

- ROLEOFLEADERSHIPINORGANIZATIONALDEVELOPMENTDocument27 pagesROLEOFLEADERSHIPINORGANIZATIONALDEVELOPMENTRee-Jane Bautista MacaraegNo ratings yet

- Questionnaire Investors Perception Towards RiskDocument2 pagesQuestionnaire Investors Perception Towards RiskasitbhatiaNo ratings yet

- Bain-Report India Venture Capital ReportDocument32 pagesBain-Report India Venture Capital ReportasitbhatiaNo ratings yet

- 007 - Asit Bhatia - Claris Distribution PVT LTDDocument17 pages007 - Asit Bhatia - Claris Distribution PVT LTDasitbhatiaNo ratings yet

- 07 - Asit Bhatia - INFYDocument15 pages07 - Asit Bhatia - INFYasitbhatiaNo ratings yet

- Sampling Asit BhatiaDocument5 pagesSampling Asit BhatiaasitbhatiaNo ratings yet

- Untitled DocumentDocument1 pageUntitled DocumentasitbhatiaNo ratings yet

- Siddhesh Moitra SAPMDocument9 pagesSiddhesh Moitra SAPMasitbhatiaNo ratings yet

- PAYoffDocument8 pagesPAYoffasitbhatiaNo ratings yet

- PAYoffDocument8 pagesPAYoffasitbhatiaNo ratings yet

- Pre-Interview FormDocument3 pagesPre-Interview FormasitbhatiaNo ratings yet

- GuddiDocument1 pageGuddiasitbhatiaNo ratings yet

- Capstone Project - FinanceDocument1 pageCapstone Project - FinanceasitbhatiaNo ratings yet

- Indiabulls Hitesh ChaurasiaDocument5 pagesIndiabulls Hitesh ChaurasiaasitbhatiaNo ratings yet

- Working Capital Management Finance Project MbaDocument67 pagesWorking Capital Management Finance Project Mbaimran shaikh67% (3)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)