You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- SATIDocument10 pagesSATIJorge Gomez0% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- September AthenaDocument1 pageSeptember AthenaSathyavathi PyNo ratings yet

- HighTech Auto Repair Business PLanDocument34 pagesHighTech Auto Repair Business PLanKyambadde FranciscoNo ratings yet

- HR KpiDocument4 pagesHR KpiALEXXA82No ratings yet

- Accounting Try LangDocument5 pagesAccounting Try LangYannah Hidalgo100% (1)

- LJJA Meijs Global Air Cargo Flows Estimation Based On OD Trade Data MSc. Thesis Final VersionDocument108 pagesLJJA Meijs Global Air Cargo Flows Estimation Based On OD Trade Data MSc. Thesis Final VersionChong An OngNo ratings yet

- Mowry Morgan Herp ReviewpaperDocument4 pagesMowry Morgan Herp ReviewpaperChong An OngNo ratings yet

- Villamizar Gomezetal 2016Document6 pagesVillamizar Gomezetal 2016Chong An OngNo ratings yet

- Factiva 20160512 1908Document162 pagesFactiva 20160512 1908Chong An OngNo ratings yet

- Factiva 20160512 1910Document119 pagesFactiva 20160512 1910Chong An OngNo ratings yet

- Factiva 20160512 1907Document161 pagesFactiva 20160512 1907Chong An OngNo ratings yet

- Factiva 20160512 1902Document157 pagesFactiva 20160512 1902Chong An OngNo ratings yet

- Factiva 20160512 1904Document155 pagesFactiva 20160512 1904Chong An OngNo ratings yet

- Factiva 20160512 1905Document144 pagesFactiva 20160512 1905Chong An OngNo ratings yet

- Sarahruhl 2008 Notesforthedirector DeadmanscellphonetcgeDocument3 pagesSarahruhl 2008 Notesforthedirector DeadmanscellphonetcgeChong An OngNo ratings yet

- PS1 Solution PDFDocument8 pagesPS1 Solution PDFChong An OngNo ratings yet

- PS2 Solution PDFDocument6 pagesPS2 Solution PDFChong An OngNo ratings yet

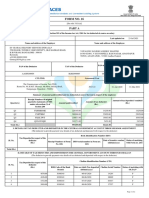

- Form No. 16: Part ADocument6 pagesForm No. 16: Part AVinuthna ChinnapaNo ratings yet

- ModEL Org MGNT 11Document30 pagesModEL Org MGNT 11Jonel LopezNo ratings yet

- Kams International Inc vs. NRC I GR No. 128806 Sept. 28 1999Document3 pagesKams International Inc vs. NRC I GR No. 128806 Sept. 28 1999TonGalabinIIINo ratings yet

- Chapter 7Document11 pagesChapter 7Syed Bilal HussainNo ratings yet

- Mod 7Document1 pageMod 7Renz Joshua Quizon MunozNo ratings yet

- Z83+Form Nqobile+Marisheni 4+Document2 pagesZ83+Form Nqobile+Marisheni 4+NqobileNo ratings yet

- Strategic Accounts Sales Executive in Atlanta GA Resume Mary ClementiDocument2 pagesStrategic Accounts Sales Executive in Atlanta GA Resume Mary ClementiMaryClementiNo ratings yet

- NurkseDocument14 pagesNurkseDeepika50% (2)

- Chapter One An Overview of Human Resource Management: Adriani DurahimDocument16 pagesChapter One An Overview of Human Resource Management: Adriani DurahimYus RimahNo ratings yet

- The Race To Develop Plastic-Eating Bacteria 4Document1 pageThe Race To Develop Plastic-Eating Bacteria 4Constance von ClaparedeNo ratings yet

- Kafka - PoseidonDocument1 pageKafka - PoseidonMarija BuljugicNo ratings yet

- NoemopinionSCTbrf Filed 12-15-23Document59 pagesNoemopinionSCTbrf Filed 12-15-23Pat PowersNo ratings yet

- Ekonomi Sumber Daya ManusiaDocument59 pagesEkonomi Sumber Daya ManusiaRasyid FikriNo ratings yet

- Hari Om Steel IndustriesDocument75 pagesHari Om Steel IndustriesViharNo ratings yet

- Annex III Personal History Statement FormDocument7 pagesAnnex III Personal History Statement FormEthan HuntNo ratings yet

- Magante V NLRC DigestDocument1 pageMagante V NLRC DigestJohnde MartinezNo ratings yet

- ElectricianDocument9 pagesElectricianapi-308761591No ratings yet

- Suraj Internship Report Final RecheckedDocument92 pagesSuraj Internship Report Final RecheckedÇrox Rmg PunkNo ratings yet

- Session 7 and 8Document33 pagesSession 7 and 8SURBHI MITTALNo ratings yet

- Day 3 Safety Inspections (Handout)Document5 pagesDay 3 Safety Inspections (Handout)mike cams100% (1)

- BHEL Unit Implements ERP PackageDocument9 pagesBHEL Unit Implements ERP PackageMuska MuskNo ratings yet

- Aws WJ 201409Document166 pagesAws WJ 201409German Favela100% (2)

- 5S Executive Summary Radi Rifki FaujiDocument4 pages5S Executive Summary Radi Rifki FaujiDyanaNo ratings yet

- WadingdingDocument43 pagesWadingdingJames Domini Lopez LabianoNo ratings yet

- WWW - Distanceeducationju.in BedgacDocument188 pagesWWW - Distanceeducationju.in BedgacSunita KumariNo ratings yet