You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Auditing and Assurance Concepts and Applications 2Document6 pagesAuditing and Assurance Concepts and Applications 2mhadzmp100% (1)

- Summary Notes - Review Far - Part 3: 1 A B C D 2Document10 pagesSummary Notes - Review Far - Part 3: 1 A B C D 2Fery AnnNo ratings yet

- Case Study Nike, Inc. - Cost of CapitalDocument6 pagesCase Study Nike, Inc. - Cost of Capitalabrown5_csustan100% (2)

- Group Activity: University of People BUS 5110 Group Activity Case StudyDocument11 pagesGroup Activity: University of People BUS 5110 Group Activity Case Studychristian allos100% (15)

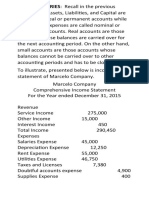

- CLOSING ENTRIES: Recall in The PreviousDocument4 pagesCLOSING ENTRIES: Recall in The PreviousPark ChimmyNo ratings yet

- Chapter 2Document2 pagesChapter 2Park ChimmyNo ratings yet

- 3 RDDocument2 pages3 RDPark ChimmyNo ratings yet

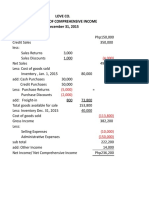

- Sample Income StatementDocument1 pageSample Income StatementPark ChimmyNo ratings yet

- Chapter 11 Capital Budgeting Cash FlowsDocument33 pagesChapter 11 Capital Budgeting Cash FlowsShahadNo ratings yet

- Accounting Group AssignmentDocument12 pagesAccounting Group Assignmentapi-288004594No ratings yet

- A8ZUYZ9tReL58evU5E2S EXCEL Stock Analysis Spreadsheet 10YR 2021 Vers 3.1Document13 pagesA8ZUYZ9tReL58evU5E2S EXCEL Stock Analysis Spreadsheet 10YR 2021 Vers 3.1Santhosh KumarNo ratings yet

- Chapter 32 - AnswerDocument11 pagesChapter 32 - AnswerKathleen LeynesNo ratings yet

- Afar 2 Module CH 5Document15 pagesAfar 2 Module CH 5Razmen Ramirez PintoNo ratings yet

- Cash Budget Definition - InvestopediaDocument2 pagesCash Budget Definition - InvestopediaBob KaneNo ratings yet

- DeVry University Walmart ProjectDocument12 pagesDeVry University Walmart ProjectKristin ParkerNo ratings yet

- Switches Can Be Purchased For $8 Per Switch ($200,000) : Baron Co. Incurs The Following Costs To Make 25,000 SwitchesDocument16 pagesSwitches Can Be Purchased For $8 Per Switch ($200,000) : Baron Co. Incurs The Following Costs To Make 25,000 SwitchesALI HAMEEDNo ratings yet

- q3 1Document26 pagesq3 1api-321469925No ratings yet

- Entrep12 q2 m10 Bookkeeping-2Document48 pagesEntrep12 q2 m10 Bookkeeping-2Gerald PatolotNo ratings yet

- Capital Budgeting FMDocument25 pagesCapital Budgeting FMAysha RiyaNo ratings yet

- Internship Report: Performance (A Case Study From Pubali Bank Limited) ."Document51 pagesInternship Report: Performance (A Case Study From Pubali Bank Limited) ."Mominul MominNo ratings yet

- 4a. Question - Chapter 4Document4 pages4a. Question - Chapter 4plinhcoco02No ratings yet

- Chapter 3 Cost Valume Profit AnalysisDocument5 pagesChapter 3 Cost Valume Profit AnalysisAbdirazak MohamedNo ratings yet

- Titman - PPT - CH04 - Financial Analysis v4Document68 pagesTitman - PPT - CH04 - Financial Analysis v4Hein HNo ratings yet

- Statement of Cash FlowsDocument30 pagesStatement of Cash FlowsG Murtaza DarsNo ratings yet

- Gwari P. AccsDocument59 pagesGwari P. AccsOwen Bawlor ManozNo ratings yet

- BAlance Sheet NikeDocument2 pagesBAlance Sheet NikeهانيNo ratings yet

- Asset Depreciation Calulation Change With Retrospective EffectDocument17 pagesAsset Depreciation Calulation Change With Retrospective EffectManas Kumar SahooNo ratings yet

- Financial Ratios CFP On ExcelDocument20 pagesFinancial Ratios CFP On ExcelAkash JadhavNo ratings yet

- Accounting Short Question and AnswersDocument4 pagesAccounting Short Question and AnswersMalik Naseer AwanNo ratings yet

- Financial & Managerial Accounting For Mbas, 5Th Edition by Easton, Halsey, Mcanally, Hartgraves & Morse Practice QuizDocument4 pagesFinancial & Managerial Accounting For Mbas, 5Th Edition by Easton, Halsey, Mcanally, Hartgraves & Morse Practice QuizLevi AlvesNo ratings yet

- Final AccountsDocument23 pagesFinal AccountsRajat srivastavaNo ratings yet

- FR Expected Questions Nov 2023Document345 pagesFR Expected Questions Nov 2023Uppara Gangadhar SagarNo ratings yet

- Pas 16-Property, Plant, & Equipment 1. Objective, Scope, and Definition MeasurementDocument4 pagesPas 16-Property, Plant, & Equipment 1. Objective, Scope, and Definition Measurementmarilyn wallaceNo ratings yet