You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- DCB Bank: Statement of AccountDocument2 pagesDCB Bank: Statement of AccounthasnainNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Introduction To Finacial Markets Final With Refence To CDSLDocument40 pagesIntroduction To Finacial Markets Final With Refence To CDSLShoumi Mahapatra100% (1)

- Ubs Case StudyDocument9 pagesUbs Case StudyIlavarasan NeeraruNo ratings yet

- Registration FormDocument2 pagesRegistration FormBuddhi Bal ChidiNo ratings yet

- Design of Concrete Structures - : Eurocodes Versus British StandardsDocument2 pagesDesign of Concrete Structures - : Eurocodes Versus British StandardsnsureshbabuNo ratings yet

- Ramon Magsaysay Memorial Colleges-Marbel Inc Accounting Education Program Purok Waling-Waling, Arellano Street, Zone II, Koronadal CityDocument3 pagesRamon Magsaysay Memorial Colleges-Marbel Inc Accounting Education Program Purok Waling-Waling, Arellano Street, Zone II, Koronadal Cityalajar opticalNo ratings yet

- Analysis of Business Environment of Top 5 Banks - PPT 2.Ppt 1Document16 pagesAnalysis of Business Environment of Top 5 Banks - PPT 2.Ppt 1Shanky DargeNo ratings yet

- APB Live BanksDocument12 pagesAPB Live BanksSumit Kumar GuptaNo ratings yet

- Warno AhmadDocument2 pagesWarno AhmadPT. Sarana Akses IndoNo ratings yet

- 57-60 Partnership & Agency DoctrinesDocument1 page57-60 Partnership & Agency DoctrinesKrishianne LabianoNo ratings yet

- O o o o O: Option (Finance)Document12 pagesO o o o O: Option (Finance)waibhavNo ratings yet

- 54thintrasupplement 110831080225 Phpapp02 PDFDocument11 pages54thintrasupplement 110831080225 Phpapp02 PDFKhaela MercaderNo ratings yet

- Swot Analysis of MCBDocument4 pagesSwot Analysis of MCBAbdulMoeedMalik100% (1)

- 5farmer Producer Operational FPO GuidelinesDocument9 pages5farmer Producer Operational FPO GuidelinesArun KurtakotiNo ratings yet

- Comsavings Bank Vs Sps. Danilo and Estrella Capistrano, GR No. 170942Document14 pagesComsavings Bank Vs Sps. Danilo and Estrella Capistrano, GR No. 170942Aldin Lucena AparecioNo ratings yet

- Financial AccountingDocument4 pagesFinancial Accountingbub12345678No ratings yet

- AEON Financial Service - AR - 2015 PDFDocument68 pagesAEON Financial Service - AR - 2015 PDFAnonymous pywZSKdXNo ratings yet

- Foundations in Accountancy Re-Registration Application: Student PortalDocument4 pagesFoundations in Accountancy Re-Registration Application: Student PortalDavis KasitomuNo ratings yet

- For Others: National Institute of Technology Tiruchirappalli - 620 015Document2 pagesFor Others: National Institute of Technology Tiruchirappalli - 620 015hakeemniyasNo ratings yet

- Company Research Report: Shriram Transport Finance Company LimitedDocument30 pagesCompany Research Report: Shriram Transport Finance Company Limitedsandip_dNo ratings yet

- Week 11 - Tutorial QuestionsDocument7 pagesWeek 11 - Tutorial QuestionsVuong Bao KhanhNo ratings yet

- Responsive Document - CREW: FDLE: Request For Records in Investigation of Rep. David Rivera: 5/14/2012 - FDLE Report (Combined)Document172 pagesResponsive Document - CREW: FDLE: Request For Records in Investigation of Rep. David Rivera: 5/14/2012 - FDLE Report (Combined)CREWNo ratings yet

- Heirs of Franco vs. Sps. Gonzales, G.R. No. 159709Document17 pagesHeirs of Franco vs. Sps. Gonzales, G.R. No. 159709joluwcarNo ratings yet

- ECS ChargesDocument14 pagesECS ChargesgnanaNo ratings yet

- Presentation Of: Allied Bank LimitedDocument21 pagesPresentation Of: Allied Bank LimitedRiaz MirzaNo ratings yet

- Karnataka Public Moneys (Recovery of Dues) Act, 1979Document7 pagesKarnataka Public Moneys (Recovery of Dues) Act, 1979Latest Laws Team0% (1)

- En Banc Ruben Reyna and Lloyd Soria, PresentDocument31 pagesEn Banc Ruben Reyna and Lloyd Soria, Presentrian5852No ratings yet

- RebateDocument163 pagesRebateSourav KumarNo ratings yet

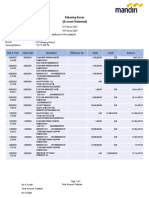

- Account - Statement - PDF - 1480016649116 - 16 February 2021Document2 pagesAccount - Statement - PDF - 1480016649116 - 16 February 2021Adipt MarajaNo ratings yet

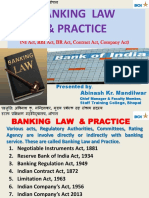

- Banking Law & PracticeDocument89 pagesBanking Law & Practicemail2piyushranjanNo ratings yet