You might also like

- CIR v. Isabela Cultural Corp.Document4 pagesCIR v. Isabela Cultural Corp.kathrynmaydevezaNo ratings yet

- Transaction Journal Posting Flow of Purchase CycleDocument8 pagesTransaction Journal Posting Flow of Purchase Cyclemukiiraeve100% (1)

- BIR Vs CA and Sps. ManlyDocument1 pageBIR Vs CA and Sps. ManlyJayNo ratings yet

- Calculation of Return and WACC: Wacc E D+ E × + D D+E × RDDocument3 pagesCalculation of Return and WACC: Wacc E D+ E × + D D+E × RDTamim ChowdhuryNo ratings yet

- FORM 16 CERTIFICATEDocument8 pagesFORM 16 CERTIFICATENidhish AgrawalNo ratings yet

- BIR Ruling (DA-145-07) March 8, 2007Document3 pagesBIR Ruling (DA-145-07) March 8, 2007Raiya AngelaNo ratings yet

- CIR V Toledo (2015)Document2 pagesCIR V Toledo (2015)Anonymous bOncqbp8yiNo ratings yet

- 07 - Visayan Cebu Terminal V CIRDocument2 pages07 - Visayan Cebu Terminal V CIRKristine De LeonNo ratings yet

- CIR v. CTA, GCLDocument2 pagesCIR v. CTA, GCLIan GanasNo ratings yet

- SC declares sections of RR 10-2008 null and void for adding qualifications not found in R.A. 9504Document5 pagesSC declares sections of RR 10-2008 null and void for adding qualifications not found in R.A. 9504Chelle BelenzoNo ratings yet

- Cir V. Philippine Airlines, Inc. (2009) : PartiesDocument3 pagesCir V. Philippine Airlines, Inc. (2009) : PartiesAila AmpNo ratings yet

- 2018 - PAL vs. CIRDocument2 pages2018 - PAL vs. CIRJimcris HermosadoNo ratings yet

- CIR v. Juliane Baier-Nickel - SUBADocument2 pagesCIR v. Juliane Baier-Nickel - SUBAPaul Joshua Torda SubaNo ratings yet

- C. Bloomberry Resorts and Hotels Inc. vs. Bureau of Internal RevenueDocument2 pagesC. Bloomberry Resorts and Hotels Inc. vs. Bureau of Internal RevenueJoieNo ratings yet

- Corre Vs Tan CorreDocument2 pagesCorre Vs Tan CorreLean Manuel ParagasNo ratings yet

- CIR Vs Stanley PHDocument2 pagesCIR Vs Stanley PHAnneNo ratings yet

- 143.CIR Vs Stanley (Phils.)Document8 pages143.CIR Vs Stanley (Phils.)Clyde KitongNo ratings yet

- 65 Commissioner of Internal Revenue v. Puregold Duty Free, IncDocument2 pages65 Commissioner of Internal Revenue v. Puregold Duty Free, IncjNo ratings yet

- CIR v. Pascor RealtyDocument1 pageCIR v. Pascor RealtyDaLe AparejadoNo ratings yet

- CIR Vs ST Luke S Medical CenterDocument6 pagesCIR Vs ST Luke S Medical CenterOlan Dave LachicaNo ratings yet

- Gutierrez V Collector 101 Phil 743Document1 pageGutierrez V Collector 101 Phil 743Khian JamerNo ratings yet

- TRANSLINERDocument2 pagesTRANSLINERMARRYROSE LASHERASNo ratings yet

- COMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Document1 pageCOMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Charles Roger Raya100% (1)

- Citizen's Alliance V Energy Regulatory CommissionDocument1 pageCitizen's Alliance V Energy Regulatory CommissionJason KingNo ratings yet

- 13.d CIR vs. CA and BPI (G.R. No. 117254 January 21, 1999) - H DigestDocument1 page13.d CIR vs. CA and BPI (G.R. No. 117254 January 21, 1999) - H DigestHarleneNo ratings yet

- SSS Case DigestDocument8 pagesSSS Case DigestJaycebelNo ratings yet

- Bloomberry Resorts vs. Cir 2016Document2 pagesBloomberry Resorts vs. Cir 2016Anny YanongNo ratings yet

- 49 CIR V Glenshaw GlassDocument2 pages49 CIR V Glenshaw GlassMiguel AlonzoNo ratings yet

- Silkair v. CIR: Proper party to claim excise tax refund is statutory taxpayerDocument3 pagesSilkair v. CIR: Proper party to claim excise tax refund is statutory taxpayerRob100% (1)

- CIR v. Asalus CorpDocument9 pagesCIR v. Asalus CorpMeg ReyesNo ratings yet

- Duty Free v. COADocument1 pageDuty Free v. COALizzy Way100% (1)

- Collector Vs HendersonDocument11 pagesCollector Vs HendersonBenedick LedesmaNo ratings yet

- Valentino Tio Vs Videogram, Regulatory Board GR No. L-75697 June 18, 1987Document1 pageValentino Tio Vs Videogram, Regulatory Board GR No. L-75697 June 18, 1987anjo020025No ratings yet

- RCBC Vs CIRDocument2 pagesRCBC Vs CIRAnneNo ratings yet

- 4 - Capili Vs Cardana Digest PDFDocument2 pages4 - Capili Vs Cardana Digest PDFNeapolle FleurNo ratings yet

- CIR v. Benguet Corp Ruling on Retroactive Application of VAT RulingDocument1 pageCIR v. Benguet Corp Ruling on Retroactive Application of VAT RulingAgnes GamboaNo ratings yet

- CIR Vs ICCDocument2 pagesCIR Vs ICCNa AbdurahimNo ratings yet

- Kabalikat VS CirDocument1 pageKabalikat VS CirKenette Diane CantubaNo ratings yet

- Sec of Finance v. LazatinDocument10 pagesSec of Finance v. Lazatinana abayaNo ratings yet

- Philippine Bank of Communications tax refund caseDocument1 pagePhilippine Bank of Communications tax refund caseKkee DdooNo ratings yet

- Swedish Match Phil vs. Treasurer of City of Manila.Document2 pagesSwedish Match Phil vs. Treasurer of City of Manila.michelle m. templadoNo ratings yet

- BPI vs. CIR Prescriptive Period for Deficiency Tax AssessmentDocument2 pagesBPI vs. CIR Prescriptive Period for Deficiency Tax AssessmentJP Murao IIINo ratings yet

- Table of LegitimesDocument1 pageTable of LegitimestopatbNo ratings yet

- Chevron Vs CIRDocument2 pagesChevron Vs CIRKim Lorenzo CalatravaNo ratings yet

- Henderson v. Collector DigestDocument2 pagesHenderson v. Collector DigestOne TwoNo ratings yet

- 14d G.R. No. L-18330 July 31, 1963 de Borja Vs GellaDocument2 pages14d G.R. No. L-18330 July 31, 1963 de Borja Vs GellarodolfoverdidajrNo ratings yet

- Philippine Airlines V CIRDocument5 pagesPhilippine Airlines V CIRBettina Rayos del SolNo ratings yet

- CIR vs. Filinvest Dev't Corp.Document2 pagesCIR vs. Filinvest Dev't Corp.Direct LukeNo ratings yet

- CIR vs. Burroghs, G.R. No. 66653, June 19, 1986Document1 pageCIR vs. Burroghs, G.R. No. 66653, June 19, 1986Oro ChamberNo ratings yet

- Corporate Income Tax GuideDocument46 pagesCorporate Income Tax GuideCanapi AmerahNo ratings yet

- Pepsi Cola vs. City of ButuanDocument1 pagePepsi Cola vs. City of ButuanArdy Falejo FajutagNo ratings yet

- Caltex Vs CoaDocument1 pageCaltex Vs CoaAnonymous 5MiN6I78I0No ratings yet

- PNOC vs. Court of Appeals upholds CTA review of tax compromiseDocument2 pagesPNOC vs. Court of Appeals upholds CTA review of tax compromisejohn vidadNo ratings yet

- CIR Vs General FoodsDocument4 pagesCIR Vs General FoodsMonaVargasNo ratings yet

- Sabena Airlines liable for damages from lost luggage in Brussels and BarcelonaDocument5 pagesSabena Airlines liable for damages from lost luggage in Brussels and BarcelonaWonder WomanNo ratings yet

- Bir V. Ca: GR. No. 197590, Nov. 24, 2014Document2 pagesBir V. Ca: GR. No. 197590, Nov. 24, 2014Jezreel Y. ChanNo ratings yet

- DIAZ v. SECRETARY OF FINANCEDocument1 pageDIAZ v. SECRETARY OF FINANCEKristine VillanuevaNo ratings yet

- 76 CIR v. Fortune Tobacco CorporationDocument3 pages76 CIR v. Fortune Tobacco CorporationMac Duguiang Jr.No ratings yet

- Income Tax DigestsDocument6 pagesIncome Tax Digestsada mae santoniaNo ratings yet

- LG-Electronics-vs.-CIR-digestDocument21 pagesLG-Electronics-vs.-CIR-digestDarrel John SombilonNo ratings yet

- CIR Vs Aluminum WheelsDocument3 pagesCIR Vs Aluminum WheelsJenifferRimandoNo ratings yet

- Tax deductions require proper substantiationDocument35 pagesTax deductions require proper substantiationDebbie De Sesto AcbangNo ratings yet

- Ing V Cir FinalDocument6 pagesIng V Cir FinalTrem GallenteNo ratings yet

- Overlord Light Novels, Manga, Drama CDs and Blu-ray Special StoriesDocument1 pageOverlord Light Novels, Manga, Drama CDs and Blu-ray Special StoriesJulian GuevarraNo ratings yet

- The Hugo Grotius of His Time: Intro Tobias AsserDocument6 pagesThe Hugo Grotius of His Time: Intro Tobias AsserJulian GuevarraNo ratings yet

- Affidavit of ComplaintDocument1 pageAffidavit of ComplaintHilron DioknoNo ratings yet

- Imasen V AlconDocument6 pagesImasen V AlconJulian GuevarraNo ratings yet

- Brief Introduction To Who Is Tobias AsserDocument8 pagesBrief Introduction To Who Is Tobias AsserJulian GuevarraNo ratings yet

- BankardDocument5 pagesBankardJulian GuevarraNo ratings yet

- Sources Topbias AsserDocument1 pageSources Topbias AsserJulian GuevarraNo ratings yet

- Coownership 2Document21 pagesCoownership 2Julian GuevarraNo ratings yet

- ANNULMENT CASE A PREJUDICIAL QUESTION IN BIGAMY PROSECUTIONDocument5 pagesANNULMENT CASE A PREJUDICIAL QUESTION IN BIGAMY PROSECUTIONJulian GuevarraNo ratings yet

- ReferencesDocument6 pagesReferencesJulian GuevarraNo ratings yet

- Case 1 Lutz V AranetaDocument1 pageCase 1 Lutz V AranetaJulian GuevarraNo ratings yet

- DAVAO GULF LUMBER CORPORATION V CIR July 23Document1 pageDAVAO GULF LUMBER CORPORATION V CIR July 23Julian GuevarraNo ratings yet

- BankardDocument5 pagesBankardJulian GuevarraNo ratings yet

- EasementsDocument36 pagesEasementsJulian GuevarraNo ratings yet

- Rule 116Document5 pagesRule 116Julian GuevarraNo ratings yet

- SourcesDocument3 pagesSourcesJulian GuevarraNo ratings yet

- Trademarks CasesDocument10 pagesTrademarks CasesJulian GuevarraNo ratings yet

- Rule 116Document5 pagesRule 116Julian GuevarraNo ratings yet

- 10 Lecture 10Document2 pages10 Lecture 10Ahmad HasnainNo ratings yet

- Tutorial Question - Sales - Service Tax 1Document5 pagesTutorial Question - Sales - Service Tax 1Braham Rahul Ram JamnadasNo ratings yet

- PayslipSalary Slips - 9-2020 PDFDocument1 pagePayslipSalary Slips - 9-2020 PDFSukant ChampatiNo ratings yet

- LSP SMK NEGERI 51 JAKARTA Entry Journal WorksheetDocument7 pagesLSP SMK NEGERI 51 JAKARTA Entry Journal WorksheetSams YogxNo ratings yet

- Financial Accounting Exam for Diploma in Accountancy StudentsDocument223 pagesFinancial Accounting Exam for Diploma in Accountancy StudentsethelNo ratings yet

- WC157 158Document5 pagesWC157 158JayBalaNo ratings yet

- Taxation I Course SyllabusDocument4 pagesTaxation I Course Syllabuszeigfred badanaNo ratings yet

- Policy Schedule Personal Accident Insurance Policy: (Plan 5)Document2 pagesPolicy Schedule Personal Accident Insurance Policy: (Plan 5)Rana BiswasNo ratings yet

- 8% Income Tax OptionDocument14 pages8% Income Tax OptionZaaavnn VannnnnNo ratings yet

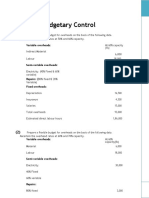

- Budgetary Control: Variable OverheadsDocument11 pagesBudgetary Control: Variable OverheadsAmmy GuptaNo ratings yet

- Computation and ProcedureDocument1 pageComputation and ProcedureJorge ParkerNo ratings yet

- Acc 496 Chapter 9Document2 pagesAcc 496 Chapter 9Abdul HassonNo ratings yet

- South Western Federal Taxation 2019 Corporations Partnerships Estates and Trusts 42nd Edition Raabe Solutions ManualDocument48 pagesSouth Western Federal Taxation 2019 Corporations Partnerships Estates and Trusts 42nd Edition Raabe Solutions Manualalicebellamyq3yj100% (19)

- Over Not Over Tax: Basic Income Table (Tax Code, Section 24 A)Document2 pagesOver Not Over Tax: Basic Income Table (Tax Code, Section 24 A)Juliana ChengNo ratings yet

- (123doc) - Tai-Lieu-Accounting-Principles-Mid-Semester-Test PDFDocument4 pages(123doc) - Tai-Lieu-Accounting-Principles-Mid-Semester-Test PDFTrung HậuNo ratings yet

- Job Order Costing Work Sheet - Answered REALDocument16 pagesJob Order Costing Work Sheet - Answered REALEllah MaeNo ratings yet

- T AccountDocument2 pagesT AccountSophia RamirezNo ratings yet

- Tax ProjectDocument8 pagesTax ProjectKunalNo ratings yet

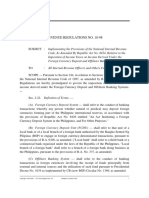

- RR 10-98 - FcduDocument6 pagesRR 10-98 - FcduCkey ArNo ratings yet

- Lecture 3 Concept of Income Accounting Period and Methods of AccountingDocument21 pagesLecture 3 Concept of Income Accounting Period and Methods of AccountingCassie ParkNo ratings yet

- Mine Investment AnalysisDocument1 pageMine Investment AnalysisAndi Ichwanul MuslimNo ratings yet

- Sol. Man. - Chapter 9 Income TaxesDocument15 pagesSol. Man. - Chapter 9 Income TaxesMiguel Amihan100% (1)

- Wells Fargo VS CirDocument2 pagesWells Fargo VS CirViolet BlueNo ratings yet

- Tax Comp ExampleDocument115 pagesTax Comp ExampleJayjay FarconNo ratings yet

- ACC 102 - Week 5 - Worksheet and Adjustments - LectureDocument2 pagesACC 102 - Week 5 - Worksheet and Adjustments - LectureJorecan Enad DacupNo ratings yet

- BIR Form 2303 Registration GuideDocument2 pagesBIR Form 2303 Registration Guidejennifer alianzaNo ratings yet

- Budgeting Assessment - 2Document3 pagesBudgeting Assessment - 2Ariel KedemNo ratings yet