You might also like

- Double Entry Bookkeeping Joan MartinDocument13 pagesDouble Entry Bookkeeping Joan MartinTyra RobinsonNo ratings yet

- International Trade and Business LawDocument530 pagesInternational Trade and Business LawMercy NamboNo ratings yet

- Ryan Deiss - 80 Point Business Marketing ChecklistDocument4 pagesRyan Deiss - 80 Point Business Marketing Checklistchiguybg100% (7)

- 0106XXXXXX8428-01-04-21 - 31-03-2022Document27 pages0106XXXXXX8428-01-04-21 - 31-03-2022SabyasachiBanerjeeNo ratings yet

- ConfessionsDocument10 pagesConfessionsMercy Nambo100% (1)

- Chapter 19 Changes in PartnershipDocument30 pagesChapter 19 Changes in PartnershipHarrison MataraNo ratings yet

- CHAPTER 5 (Accounting For Service)Document26 pagesCHAPTER 5 (Accounting For Service)lc100% (1)

- CB Insights - Fintech Report Q2 2020Document89 pagesCB Insights - Fintech Report Q2 2020Hector Andrade100% (2)

- Syllabus On Banking and Financial InstitutionsDocument2 pagesSyllabus On Banking and Financial InstitutionsFatima Bagay94% (18)

- Journalizing: Jessah Mae G. FernandezDocument38 pagesJournalizing: Jessah Mae G. FernandezmNo ratings yet

- Ledger Account ExamplesDocument8 pagesLedger Account Examplestanmay agrawalNo ratings yet

- Ac11 Answer Sheet Ex1 Fall 06 - KeyDocument5 pagesAc11 Answer Sheet Ex1 Fall 06 - KeySteven SandersonNo ratings yet

- Journal Entries in The Books of Medi StoreDocument8 pagesJournal Entries in The Books of Medi StoreAkshay Pratap SinghNo ratings yet

- VAKEV s6 Updated Note 2023-2024 XVDocument83 pagesVAKEV s6 Updated Note 2023-2024 XVvigiraneza0No ratings yet

- Cash BookDocument5 pagesCash BookZaara AshfaqNo ratings yet

- Untitled FgapqDocument5 pagesUntitled FgapqSusovan SirNo ratings yet

- Reading of Ledger AccountDocument18 pagesReading of Ledger Accountneeru79200050% (2)

- Date Particulars J/F Amount Date Particulars J/F: in The Books of Orbit EnterprisesDocument12 pagesDate Particulars J/F Amount Date Particulars J/F: in The Books of Orbit EnterprisesShera BhaiNo ratings yet

- 1 Foundation FT 1 (Solved)Document18 pages1 Foundation FT 1 (Solved)shrinivassunilkatkar2002No ratings yet

- Business Pp2 MsDocument6 pagesBusiness Pp2 MsmartinNo ratings yet

- Tutorial Letter 202/1/2020: Financial Accounting Principles For Law PractitionersDocument9 pagesTutorial Letter 202/1/2020: Financial Accounting Principles For Law Practitionersall green associatesNo ratings yet

- Sheet 3 2020 PDFDocument11 pagesSheet 3 2020 PDFmagdy kamelNo ratings yet

- Accounting INDIVIDUAL ASSIGNMENTDocument17 pagesAccounting INDIVIDUAL ASSIGNMENTHajara SaleethNo ratings yet

- AP PPE QuizDocument3 pagesAP PPE QuizjomsNo ratings yet

- Q.1 Record This Transactions in Cash Book and Other LedgersDocument7 pagesQ.1 Record This Transactions in Cash Book and Other LedgersAnuj GohainNo ratings yet

- Week3-Lecture 6 NotesDocument28 pagesWeek3-Lecture 6 Noteskk23212No ratings yet

- Accounts Question Paper With SolutionsDocument17 pagesAccounts Question Paper With SolutionsAMIN BUHARI ABDUL KHADER67% (9)

- Accounts Question Paper With AnswersDocument17 pagesAccounts Question Paper With AnswersAMIN BUHARI ABDUL KHADERNo ratings yet

- Depreciation Solution PDFDocument10 pagesDepreciation Solution PDFDivya PunjabiNo ratings yet

- Assignment No 1 FinalDocument13 pagesAssignment No 1 FinalMuhammad AwaisNo ratings yet

- Unit 2 - Accountingformanager - AnanduDocument52 pagesUnit 2 - Accountingformanager - Ananducraziestidiot31No ratings yet

- Preparation of The General: JournalDocument3 pagesPreparation of The General: JournalWamema joshuaNo ratings yet

- Bcoc-131: Financial Accounting Tutor Marked AssignmentDocument17 pagesBcoc-131: Financial Accounting Tutor Marked AssignmentRajni KumariNo ratings yet

- HA2032Document12 pagesHA2032Aayam SubediNo ratings yet

- POA - mt.01 SolutionDocument7 pagesPOA - mt.01 SolutionHường Đoàn ThịNo ratings yet

- 11.recording Business TransactionDocument17 pages11.recording Business TransactionAfrin rahman miliNo ratings yet

- ACC407 - Chapter 4b - Trial BalanceDocument18 pagesACC407 - Chapter 4b - Trial BalanceA24 Izzah100% (1)

- Accountancy-Books of Prime EntryDocument8 pagesAccountancy-Books of Prime EntryGedie Rocamora100% (1)

- 11 Acc Task 5.5 5.8 5.9 5.12 5.16 Memos 2023 GoodDocument10 pages11 Acc Task 5.5 5.8 5.9 5.12 5.16 Memos 2023 Goodora mashaNo ratings yet

- Project Report in Accountancy: - Submitted by - Nishan Pant - Grade - 11 - Section DDocument13 pagesProject Report in Accountancy: - Submitted by - Nishan Pant - Grade - 11 - Section Dnishan pantNo ratings yet

- FA Cia 1Document10 pagesFA Cia 1K M NANDAKISHORE 2210824No ratings yet

- Internal Reconstruction Part-IIDocument13 pagesInternal Reconstruction Part-IIINTER SMARTIANSNo ratings yet

- Unit 3: Trial Balance: Learning OutcomesDocument13 pagesUnit 3: Trial Balance: Learning OutcomesSjNo ratings yet

- The Role of The Cash BookDocument67 pagesThe Role of The Cash BookMercy NamboNo ratings yet

- Sem-1 14 BCOM GENERAL CC-1.1CG FINANCIAL-ACCOUNTING-I-1348 PDFDocument11 pagesSem-1 14 BCOM GENERAL CC-1.1CG FINANCIAL-ACCOUNTING-I-1348 PDFJude VascoNo ratings yet

- Model Test Paper 15Document15 pagesModel Test Paper 15ganeshNo ratings yet

- Journal Date Description Post REF. DebitDocument20 pagesJournal Date Description Post REF. DebitKanika SharmaNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Mehta AutoCare Pvt. Ltd.Document30 pagesMehta AutoCare Pvt. Ltd.Shashank PatelNo ratings yet

- Principles of Accounts 11Document47 pagesPrinciples of Accounts 11Godfrey LwandoNo ratings yet

- Presentation ON General Ledger & Trail BalanceDocument14 pagesPresentation ON General Ledger & Trail BalanceNumanNo ratings yet

- P18Document23 pagesP18aleeshaNo ratings yet

- Banking Insurance Sem. I Choice Base R 2016 81301 Financial Accounting I Q.P.CODE 59346Document7 pagesBanking Insurance Sem. I Choice Base R 2016 81301 Financial Accounting I Q.P.CODE 59346Ali HassanNo ratings yet

- Financial Accounting - B, Com Sem I NEP 2022 PDFDocument6 pagesFinancial Accounting - B, Com Sem I NEP 2022 PDF『SHREYAS NAIDU』No ratings yet

- Summer ExamDocument17 pagesSummer Examoliverchukwudi97No ratings yet

- Cash Books To StudentsDocument8 pagesCash Books To StudentsIRUNGU BRENDA MURUGINo ratings yet

- 03 Books of Original Entry and Ledgers (I)Document16 pages03 Books of Original Entry and Ledgers (I)YU TaktakNo ratings yet

- 2019 Review Quiz Without Answer SheetDocument4 pages2019 Review Quiz Without Answer SheetSittie HafsahNo ratings yet

- 72222bos58192 P1aDocument11 pages72222bos58192 P1aSufiyan MominNo ratings yet

- Answer Sheet Workbookquestions DeprciationDocument10 pagesAnswer Sheet Workbookquestions DeprciationgunasekarasugeethaNo ratings yet

- JournalDocument5 pagesJournalGanapathi VNo ratings yet

- 1st Unit Test B.K 12th 2020Document2 pages1st Unit Test B.K 12th 2020Soham SahareNo ratings yet

- Acctg Books - Subsidiary Ledgers IllustrationDocument9 pagesAcctg Books - Subsidiary Ledgers IllustrationCorn SaladNo ratings yet

- CA Foundation Accounts A MTP 2 Dec 2022Document11 pagesCA Foundation Accounts A MTP 2 Dec 2022shagana212005No ratings yet

- Generally Accepted Accounting Principles (GAAP) andDocument58 pagesGenerally Accepted Accounting Principles (GAAP) andamithkiran100% (1)

- The Role of The Cash BookDocument67 pagesThe Role of The Cash BookMercy NamboNo ratings yet

- Introduction PovertyDocument3 pagesIntroduction PovertyMercy NamboNo ratings yet

- InsuranceDocument52 pagesInsuranceMercy NamboNo ratings yet

- Law of CooperativesDocument28 pagesLaw of CooperativesMercy NamboNo ratings yet

- TaxesDocument3 pagesTaxesMercy NamboNo ratings yet

- Notes ICTDocument68 pagesNotes ICTMercy NamboNo ratings yet

- Partnerships in KenyaDocument13 pagesPartnerships in KenyaMercy NamboNo ratings yet

- Delay Defeats EquityDocument5 pagesDelay Defeats EquityMercy NamboNo ratings yet

- Extent of Poverty in KenyaDocument3 pagesExtent of Poverty in KenyaMercy NamboNo ratings yet

- Misconduct and Integrity IssuesDocument3 pagesMisconduct and Integrity IssuesMercy NamboNo ratings yet

- Date Received For Registration Presentation Book Registration FeesDocument2 pagesDate Received For Registration Presentation Book Registration FeesMercy NamboNo ratings yet

- Theories of ADMINDocument10 pagesTheories of ADMINMercy NamboNo ratings yet

- Mount Kenya University School of LawDocument6 pagesMount Kenya University School of LawMercy NamboNo ratings yet

- Administrative Law: Class Notes by Dr. Dwasi Jane © 2004 University of NairobiDocument24 pagesAdministrative Law: Class Notes by Dr. Dwasi Jane © 2004 University of NairobiMercy NamboNo ratings yet

- BankingDocument6 pagesBankingMercy NamboNo ratings yet

- Do Judges Make Law?: This Paper Will Proceed To Answer Two QuestionsDocument8 pagesDo Judges Make Law?: This Paper Will Proceed To Answer Two QuestionsMercy Nambo100% (1)

- Kabillah - The Office of The Ombudsman As An Advocate of Access To Administrative Justice Lessons For KenyaDocument147 pagesKabillah - The Office of The Ombudsman As An Advocate of Access To Administrative Justice Lessons For KenyaMercy NamboNo ratings yet

- Community Land Definition: Salient Features OwnershipDocument3 pagesCommunity Land Definition: Salient Features OwnershipMercy NamboNo ratings yet

- ATM Crunch: Economic Betterment or Cost Reduction MoveDocument4 pagesATM Crunch: Economic Betterment or Cost Reduction MoveChristine VergheseNo ratings yet

- Kelvin Njenga Bank Statement - 12 - 02 - 2024Document1 pageKelvin Njenga Bank Statement - 12 - 02 - 2024kendallbolton534No ratings yet

- Pre-Eliminary ImplementationDocument10 pagesPre-Eliminary Implementationyosdi harmenNo ratings yet

- Cashier Audit 09-AugDocument3 pagesCashier Audit 09-AugRoberto LamasNo ratings yet

- HSBC BackgroundDocument2 pagesHSBC BackgroundNazim UddinNo ratings yet

- SOA Acct 2738103 32023Document2 pagesSOA Acct 2738103 32023L&L TransportNo ratings yet

- MFMRI. Commerce Faculty BHU, Placement ReportDocument3 pagesMFMRI. Commerce Faculty BHU, Placement ReportALOK KUMAR100% (1)

- Accounting UC3M Midterm Mock ExamDocument5 pagesAccounting UC3M Midterm Mock ExamInterecoNo ratings yet

- 2019 2020 Star Rated HotelsDocument2 pages2019 2020 Star Rated HotelsJohn Paulo VelasquezNo ratings yet

- Sample Assignment TESCO UKDocument18 pagesSample Assignment TESCO UKLwk KheanNo ratings yet

- Periodic MethodDocument14 pagesPeriodic MethodRACHEL DAMALERIONo ratings yet

- SBI ATMDebit Card Application FormDocument4 pagesSBI ATMDebit Card Application Formrajeev11juneNo ratings yet

- 2 Ipecs Ucm Wms Manual Issue 1.1 1517389492943Document440 pages2 Ipecs Ucm Wms Manual Issue 1.1 1517389492943MasterNo ratings yet

- Finacle - Some Important Function KeysDocument10 pagesFinacle - Some Important Function KeysSudershan ThaibaNo ratings yet

- Paras ItrDocument61 pagesParas ItrArun BhardwajNo ratings yet

- Wireless and Mobile All-IP Networks: Yi-Bing Lin and Ai-Chun Pang Liny@csie - Nctu.edu - TWDocument80 pagesWireless and Mobile All-IP Networks: Yi-Bing Lin and Ai-Chun Pang Liny@csie - Nctu.edu - TWSabareesan SankaranNo ratings yet

- Savings Accounts TNCDocument2 pagesSavings Accounts TNCrohan1234567No ratings yet

- Supplementary Terms & Condition LetterDocument2 pagesSupplementary Terms & Condition LetterSunil GoyalNo ratings yet

- ACH Block AuthorizationDocument1 pageACH Block AuthorizationZim UgochukwuNo ratings yet

- Meraki WaiverDocument4 pagesMeraki WaiverJayson RenoloNo ratings yet

- Mareting in Digital World PresentationDocument34 pagesMareting in Digital World PresentationFeroj AhmedNo ratings yet

- Modern Treasury - Accounting For Developers Parts I-IIIDocument32 pagesModern Treasury - Accounting For Developers Parts I-IIIfelipeap92No ratings yet

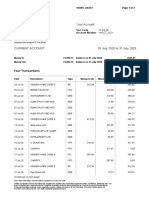

- Current Account 01 July 2020 To 31 July 2020: Your TransactionsDocument1 pageCurrent Account 01 July 2020 To 31 July 2020: Your TransactionsRamesh NatarajanNo ratings yet

- Data (5) HODocument35 pagesData (5) HOKarim AwaadNo ratings yet

- Bill Statement 05 2023 PDFDocument2 pagesBill Statement 05 2023 PDFJasmin RojiyaNo ratings yet

- Grade 9 Accounting p2Document5 pagesGrade 9 Accounting p2AliNo ratings yet