You might also like

- Minsupala Trading Corporation (Workbook)Document14 pagesMinsupala Trading Corporation (Workbook)Luis Melquiades P. Garcia100% (3)

- Profit and Loss - Balance SheetDocument4 pagesProfit and Loss - Balance SheetAnklesh kumar Gupta100% (1)

- Format - SOPL N SOFPDocument2 pagesFormat - SOPL N SOFPA24 Izzah50% (2)

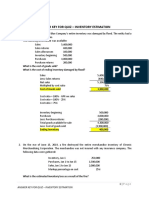

- Answer Key For Quiz - Inventory EstimationDocument6 pagesAnswer Key For Quiz - Inventory EstimationMelogen Labrador100% (3)

- Chapter 16Document17 pagesChapter 16Punit SharmaNo ratings yet

- Calculating Financial Metrics and Project ValuationDocument10 pagesCalculating Financial Metrics and Project Valuationpraveen gandiNo ratings yet

- Ifrs 9 Ecl Template General ApproachDocument2 pagesIfrs 9 Ecl Template General ApproachTousief NaqviNo ratings yet

- Steps in The Accounting Process: Ans:1 Definition of Accounting. 1: The System of Recording and SummarizingDocument9 pagesSteps in The Accounting Process: Ans:1 Definition of Accounting. 1: The System of Recording and SummarizingshamagondalNo ratings yet

- Financial Accounting Part 6Document26 pagesFinancial Accounting Part 6dannydoly100% (1)

- Quizzes Chapter 9 Acctg Cycle of A Service BusinessDocument26 pagesQuizzes Chapter 9 Acctg Cycle of A Service BusinessJames CastañedaNo ratings yet

- ACCT1200 (Fall 20) Lecture & Tutorial 5 Accounting Cycle 3Document9 pagesACCT1200 (Fall 20) Lecture & Tutorial 5 Accounting Cycle 3Lyaman TagizadeNo ratings yet

- Chapter 2 Review Sheet AnswersDocument7 pagesChapter 2 Review Sheet AnswersKenneth DayohNo ratings yet

- Co 2101Document3 pagesCo 2101PRIYA LAKSHMANNo ratings yet

- MGT101 12-15Document62 pagesMGT101 12-15Nasir BashirNo ratings yet

- Dbb1202 - Financial AccountingDocument5 pagesDbb1202 - Financial AccountingVansh JainNo ratings yet

- SET 1. Q.1 Explain Any Two Accounting Concepts With Example? AnsDocument9 pagesSET 1. Q.1 Explain Any Two Accounting Concepts With Example? AnsmuravbookNo ratings yet

- Unit 9Document29 pagesUnit 9Anilkumar KyNo ratings yet

- Accounting transactions journal entriesDocument8 pagesAccounting transactions journal entriesGedie Rocamora100% (1)

- Answers-Accounting CB 2nd Ed CambridgeDocument119 pagesAnswers-Accounting CB 2nd Ed Cambridgebk4t7j8g92No ratings yet

- Accounts Textbook AnswersDocument84 pagesAccounts Textbook AnswersVidhi Patel100% (4)

- Finanal Accounts - Solved ExamplesDocument11 pagesFinanal Accounts - Solved ExamplesDesmond Suting100% (2)

- MB0025 Financial and Management AccountingDocument7 pagesMB0025 Financial and Management Accountingvarsha100% (1)

- FYJC Book Keeping and Accuntancy Topic Final AccountDocument4 pagesFYJC Book Keeping and Accuntancy Topic Final AccountRavichandraNo ratings yet

- Sample worksheet K204050266 P3.5Document16 pagesSample worksheet K204050266 P3.5Trâm Mai Thị ThùyNo ratings yet

- Arab Final 90% Fall2021 (YS)Document8 pagesArab Final 90% Fall2021 (YS)ahmed abuzedNo ratings yet

- Set 1 MB0025 Financial and Management AccountingDocument7 pagesSet 1 MB0025 Financial and Management AccountingcaggandhiNo ratings yet

- Quizzes - Chapter 9 - Acctg Cycle of A Service BusinessDocument27 pagesQuizzes - Chapter 9 - Acctg Cycle of A Service BusinessArgene Bonghanoy AbellanosaNo ratings yet

- Partnership Accounts - IDocument23 pagesPartnership Accounts - IM JEEVARATHNAM NAIDU100% (1)

- Accounts Question Paper With AnswersDocument17 pagesAccounts Question Paper With AnswersAMIN BUHARI ABDUL KHADERNo ratings yet

- Advanced Accounting Week 4Document3 pagesAdvanced Accounting Week 4rahmaNo ratings yet

- Notes On Chapter 7: 7.1 Purposes of The Trading and Profit and Loss AccountDocument3 pagesNotes On Chapter 7: 7.1 Purposes of The Trading and Profit and Loss AccountAngel LawsonNo ratings yet

- Grade 11 AccoountsDocument10 pagesGrade 11 AccoountsJane MalhanganaNo ratings yet

- JournalDocument5 pagesJournalGanapathi VNo ratings yet

- "Final Accounts of Bishal Saree Centre" AccountancyDocument15 pages"Final Accounts of Bishal Saree Centre" AccountancyPravat Ranjan NagNo ratings yet

- Partnership Q1 To Q3 SolutionsDocument8 pagesPartnership Q1 To Q3 SolutionsJAYARAJALAKSHMI IlangoNo ratings yet

- ACCA Pilot Paper Int PPQDocument19 pagesACCA Pilot Paper Int PPQqaisar1982No ratings yet

- Assistant Professor Dept. of Commerce Shift - I ST - Thomas College of Arts and Science Koyambedu, Chennai-107Document87 pagesAssistant Professor Dept. of Commerce Shift - I ST - Thomas College of Arts and Science Koyambedu, Chennai-107123456No ratings yet

- Solution For Accounting Information Systems Basic Concepts and Current Issues 3rd Edition PDFDocument12 pagesSolution For Accounting Information Systems Basic Concepts and Current Issues 3rd Edition PDFCB OrdersNo ratings yet

- Session 5 - Ledger Format & Posting of TransactionsDocument33 pagesSession 5 - Ledger Format & Posting of Transactionsanandakumar100% (1)

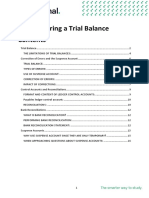

- Meaning and Types of Trail BalanceDocument4 pagesMeaning and Types of Trail Balancesujan BhandariNo ratings yet

- Financial and Management Accounting MB0025Document27 pagesFinancial and Management Accounting MB0025manuunamNo ratings yet

- Recording Financial Transactions Part 2Document4 pagesRecording Financial Transactions Part 2Debbie DebzNo ratings yet

- FA - Preparing A Trial BalanceDocument19 pagesFA - Preparing A Trial BalanceOwen GradyNo ratings yet

- Topic 4Document18 pagesTopic 4Sharmilah UthyasuriyanNo ratings yet

- Chapter: Common Size, Comparative and Trend AnalysisDocument6 pagesChapter: Common Size, Comparative and Trend Analysiseldridatech pvt ltdNo ratings yet

- Full Download Corporate Financial Accounting 14th Edition Warren Solutions ManualDocument35 pagesFull Download Corporate Financial Accounting 14th Edition Warren Solutions Manualmasonh7dswebb100% (39)

- Dwnload Full Corporate Financial Accounting 14th Edition Warren Solutions Manual PDFDocument35 pagesDwnload Full Corporate Financial Accounting 14th Edition Warren Solutions Manual PDFhofstadgypsyus100% (17)

- CSEC Principles of Accounts June 2015 Paper 1Document14 pagesCSEC Principles of Accounts June 2015 Paper 1Aria PersaudNo ratings yet

- FINANCIAL ACCOUNTING TESTDocument7 pagesFINANCIAL ACCOUNTING TESTSoumyadip DasNo ratings yet

- 6 Completion of Accounting Cycle UDDocument28 pages6 Completion of Accounting Cycle UDERICK MLINGWANo ratings yet

- Tugas Kelompok Ke-1 Week 3/ Sesi 4: EssayDocument5 pagesTugas Kelompok Ke-1 Week 3/ Sesi 4: Essayadelia zahraNo ratings yet

- 1500534100Document92 pages1500534100theabhishekdahalNo ratings yet

- 250 Question PaperDocument3 pages250 Question PaperSam NayakNo ratings yet

- Allama Iqbals accounting checklistDocument5 pagesAllama Iqbals accounting checklistAkhbar-ul- AkhyarNo ratings yet

- MID TERM EXAM REVIEW: FINANCIAL ACCOUNTING FUNDAMENTALSDocument3 pagesMID TERM EXAM REVIEW: FINANCIAL ACCOUNTING FUNDAMENTALSsahittiNo ratings yet

- Winning the Trading Game: Why 95% of Traders Lose and What You Must Do To WinFrom EverandWinning the Trading Game: Why 95% of Traders Lose and What You Must Do To WinNo ratings yet

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Question Chapter 7Document1 pageQuestion Chapter 7A24 IzzahNo ratings yet

- HRM - Izzah Izyana 1Document1 pageHRM - Izzah Izyana 1A24 IzzahNo ratings yet

- Test Law of AgencyDocument28 pagesTest Law of AgencyA24 IzzahNo ratings yet

- Individual Assignment 2. Reflective PaperDocument2 pagesIndividual Assignment 2. Reflective PaperA24 Izzah0% (1)

- BCH Fia f23Document215 pagesBCH Fia f23jprichardbcNo ratings yet

- Tax Rate Calculation and WACC for SignifyDocument9 pagesTax Rate Calculation and WACC for SignifyShivam GoelNo ratings yet

- Absorption and Variable CostingDocument3 pagesAbsorption and Variable CostingMohtasim Bin HabibNo ratings yet

- CA Inter Accounting Revision NotesDocument106 pagesCA Inter Accounting Revision NoteskalyanikamineniNo ratings yet

- SEBI Takeover Code Presentation by Niveeta Meshram, Aditya Bhujbal and Samir GopalDocument11 pagesSEBI Takeover Code Presentation by Niveeta Meshram, Aditya Bhujbal and Samir GopalSameer Gopal0% (1)

- Lembar JawabDocument9 pagesLembar JawabRita CahyaniNo ratings yet

- Capital BudgetingDocument22 pagesCapital BudgetingRajatNo ratings yet

- Vergina Natasha - CASE STUDY DIVIDEND POLICYDocument3 pagesVergina Natasha - CASE STUDY DIVIDEND POLICYVergina NatashaNo ratings yet

- Income Tax Act - UgandaDocument157 pagesIncome Tax Act - Ugandafnyeko100% (11)

- Intacc Chapter 1Document2 pagesIntacc Chapter 1Niño Albert EugenioNo ratings yet

- MR Badar Kazmi, CEO of Standard Chartered BankDocument1 pageMR Badar Kazmi, CEO of Standard Chartered BankasifsahuNo ratings yet

- Aud FeDocument11 pagesAud FeMark Domingo MendozaNo ratings yet

- TAX-402: Percentage TAX (P 2) : - T R S ADocument5 pagesTAX-402: Percentage TAX (P 2) : - T R S AEira ShaneNo ratings yet

- Title X. - Appraisal RightDocument2 pagesTitle X. - Appraisal RightAlyn SimNo ratings yet

- NismDocument17 pagesNismRohit Shet50% (2)

- Types of Financial Decisions: Investment Decision, Financing Decision, Dividend Decision and Working Capital Management DecisionDocument4 pagesTypes of Financial Decisions: Investment Decision, Financing Decision, Dividend Decision and Working Capital Management DecisionCjhay MarcosNo ratings yet

- Common Errors in DCF ModelsDocument12 pagesCommon Errors in DCF Modelsrslamba1100% (2)

- Audit ChecklistDocument2 pagesAudit ChecklistJahaziNo ratings yet

- Types of Companies Registered in SECPDocument4 pagesTypes of Companies Registered in SECPAXian TanveerNo ratings yet

- DocumentDocument5 pagesDocumentJannelle SalacNo ratings yet

- Resume FormatDocument1 pageResume FormatNishan ShettyNo ratings yet

- Dividends Calculations for Preference and Ordinary SharesDocument9 pagesDividends Calculations for Preference and Ordinary SharesPenelope PalconNo ratings yet

- Operating Segment StudentsDocument4 pagesOperating Segment StudentsAG VenturesNo ratings yet

- ENTREPRENEURSHIP: LEGAL FORMS OF BUSINESS ORGANIZATIONDocument68 pagesENTREPRENEURSHIP: LEGAL FORMS OF BUSINESS ORGANIZATIONHưng Đặng QuốcNo ratings yet

- Accounting cycle stepsDocument36 pagesAccounting cycle stepsRodolfo CorpuzNo ratings yet

- ISA 805 AUDITDocument19 pagesISA 805 AUDITLulu DwiNo ratings yet