You might also like

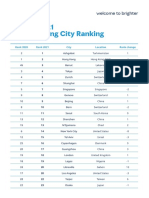

- GL 2021 Cost of Living City Ranking Mercer 0622Document9 pagesGL 2021 Cost of Living City Ranking Mercer 0622Stathis MetsovitisNo ratings yet

- The Lancet Advierte A Gobiernos y Asesores Porqué Ahora La Fase 4 Es Más Importante Que La Fase 3Document3 pagesThe Lancet Advierte A Gobiernos y Asesores Porqué Ahora La Fase 4 Es Más Importante Que La Fase 3Urgente24No ratings yet

- Astra Zeneca - D8110C00001 - CSP-v2Document111 pagesAstra Zeneca - D8110C00001 - CSP-v2Urgente24No ratings yet

- Canal 9: Falló A Favor de Remigio Ángel González González en Un Litigio Contra El Abogado Carlos Lorefice LynchDocument130 pagesCanal 9: Falló A Favor de Remigio Ángel González González en Un Litigio Contra El Abogado Carlos Lorefice LynchClaudio Andrés De LucaNo ratings yet

- FCA Enters Into 6.3 Billion Credit Facility With Intesa SanpaoloDocument3 pagesFCA Enters Into 6.3 Billion Credit Facility With Intesa SanpaoloUrgente24No ratings yet

- Informe Del Credit Suisse Sobre Oferta Argentina de DeudaDocument6 pagesInforme Del Credit Suisse Sobre Oferta Argentina de DeudaUrgente24No ratings yet

- Ganadores y Perdedores Según JP MorganDocument10 pagesGanadores y Perdedores Según JP MorganUrgente24No ratings yet

- Reigniting Growth in Low-Income en Emerging Market - FMIDocument28 pagesReigniting Growth in Low-Income en Emerging Market - FMIUrgente24No ratings yet

- El Embargo A Robert BoschDocument3 pagesEl Embargo A Robert BoschUrgente24No ratings yet

- Informe Jul19 NacionalDocument30 pagesInforme Jul19 NacionalUrgente24No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Chapter-2 Concept of DerivativesDocument50 pagesChapter-2 Concept of Derivativesamrin banuNo ratings yet

- The Work of The Alien Property CustodianDocument16 pagesThe Work of The Alien Property CustodianMika'il BeyNo ratings yet

- Interim Order in The Matter of Infocare Infra LimitedDocument14 pagesInterim Order in The Matter of Infocare Infra LimitedShyam SunderNo ratings yet

- Contemporary Financial Management 14th Edition Moyer Solutions ManualDocument7 pagesContemporary Financial Management 14th Edition Moyer Solutions Manualbenjaminnelsonijmekzfdos100% (13)

- Nguyen Dang Bao Tran - s3801633 - Assignment 1 Business Report - BAFI3184 Business FinanceDocument14 pagesNguyen Dang Bao Tran - s3801633 - Assignment 1 Business Report - BAFI3184 Business FinanceNgọc MaiNo ratings yet

- 1.1.26.11.2012 Financial ServicesDocument329 pages1.1.26.11.2012 Financial ServicesfunshareNo ratings yet

- Court Update For Reading 2017Document132 pagesCourt Update For Reading 2017chris cardinoNo ratings yet

- TATA AIA Fund-Performance-Aug20Document55 pagesTATA AIA Fund-Performance-Aug20Abhijit ChakiNo ratings yet

- Guide To Investing in Emerging and Frontier MarketsDocument40 pagesGuide To Investing in Emerging and Frontier MarketsAndrew CrabbeNo ratings yet

- Motilal Oswal Financial Services LTDDocument4 pagesMotilal Oswal Financial Services LTDAkriti SharmaNo ratings yet

- Australia and New Zealand Banking Group Limited 6.736 Dated 17 Mar 23Document12 pagesAustralia and New Zealand Banking Group Limited 6.736 Dated 17 Mar 23Mister MisterNo ratings yet

- 20189616154angel Broking DRHPDocument349 pages20189616154angel Broking DRHPravi.youNo ratings yet

- Raport 2010 LuxairDocument28 pagesRaport 2010 Luxaircatalin_ionut005804No ratings yet

- Sfig Blockchain Report PDFDocument40 pagesSfig Blockchain Report PDFbablu boroNo ratings yet

- Kasapreko PLC Prospectus November 2023Document189 pagesKasapreko PLC Prospectus November 2023kofiatisu0000No ratings yet

- Recovery2017020 Wilful DefaultDocument9 pagesRecovery2017020 Wilful DefaultBrijeshNo ratings yet

- Let's Know: Learning Activity SheetDocument8 pagesLet's Know: Learning Activity SheetWahidah BaraocorNo ratings yet

- Buczek 20101012 Judicial Notice Title 18 Not Law, Etc 54 & 121 & 141Document45 pagesBuczek 20101012 Judicial Notice Title 18 Not Law, Etc 54 & 121 & 141Bob HurtNo ratings yet

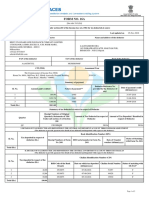

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToAkriti JhaNo ratings yet

- Regulation of para Banking Activities of Commercial BanksDocument18 pagesRegulation of para Banking Activities of Commercial BanksEswar StarkNo ratings yet

- Comprehensive Exercises On Equity InvestmentquestionaireDocument4 pagesComprehensive Exercises On Equity InvestmentquestionaireLilian LagrimasNo ratings yet

- Assignment - Financial Institutions and MarketsDocument6 pagesAssignment - Financial Institutions and MarketsShivam GoelNo ratings yet

- MCQ S Question Bank - Law: Company Basic ConceptsDocument33 pagesMCQ S Question Bank - Law: Company Basic Conceptssayan biswas100% (1)

- Nflpa 2019 LM-2Document440 pagesNflpa 2019 LM-2Robert LeeNo ratings yet

- Investments:: True or FalseDocument9 pagesInvestments:: True or FalseXienaNo ratings yet

- Isbn6582-0 Ross ch24Document21 pagesIsbn6582-0 Ross ch24NurArianaNo ratings yet

- 30 Bank of The Philippine Islands v. Intermediate Appellate CourtDocument13 pages30 Bank of The Philippine Islands v. Intermediate Appellate CourtKaiiSophieNo ratings yet

- What Is The Difference Between Commercial Banking and Merchant BankingDocument8 pagesWhat Is The Difference Between Commercial Banking and Merchant BankingScarlett Lewis100% (2)

- Aberdeen First Israel Fund, Inc. (ISL)Document28 pagesAberdeen First Israel Fund, Inc. (ISL)ArvinLedesmaChiongNo ratings yet

- DCB Bank Annual Report 2019 20Document163 pagesDCB Bank Annual Report 2019 20Anitha PeyyalaNo ratings yet